Development Charges (DCs)

Learn about development charges in Canadian real estate — what they fund, who pays, and why they’re key in urban growth.

July 27, 2025

What are Development Charges?

Development charges (DCs) are fees imposed by municipalities on new developments to help fund infrastructure and services required due to growth.

Why Development Charges Matter in Real Estate

In Canadian real estate development, DCs ensure that growth-related costs are shared by new developments rather than existing taxpayers.

DCs fund:

- Roads and transit

- Water and sewer systems

- Parks and recreation facilities

- Libraries and emergency services

Understanding DCs helps developers budget accurately and assess project feasibility.

Example of Development Charges in Action

The developer factored in development charges when budgeting for the new 100-unit condo project.

Key Takeaways

- Fees levied on new development

- Fund infrastructure and community services

- Applied at municipal level

- Significant cost in project budgeting

- Supports growth management

Related Terms

- Building Permit

- Urban Planning

- Land Use Bylaws

- Official Plan

- Zoning

holborn.ca

holborn.ca

Hale Founders Eric Abugov and Robin Kerbel

Hale Founders Eric Abugov and Robin Kerbel This year's Board & Barrel: Charcuterie Experience will take place on July 25

This year's Board & Barrel: Charcuterie Experience will take place on July 25 The Board & Barrel: Charcuterie Experience

The Board & Barrel: Charcuterie Experience This year's Smash & Sear: Best in Burger Competition will be held on August 9

This year's Smash & Sear: Best in Burger Competition will be held on August 9 The Smash & Sear: Best in Burger Competition

The Smash & Sear: Best in Burger Competition Hale's new Cabin store opens this summer

Hale's new Cabin store opens this summer The Barn venue is slated for completion in spring 2027

The Barn venue is slated for completion in spring 2027

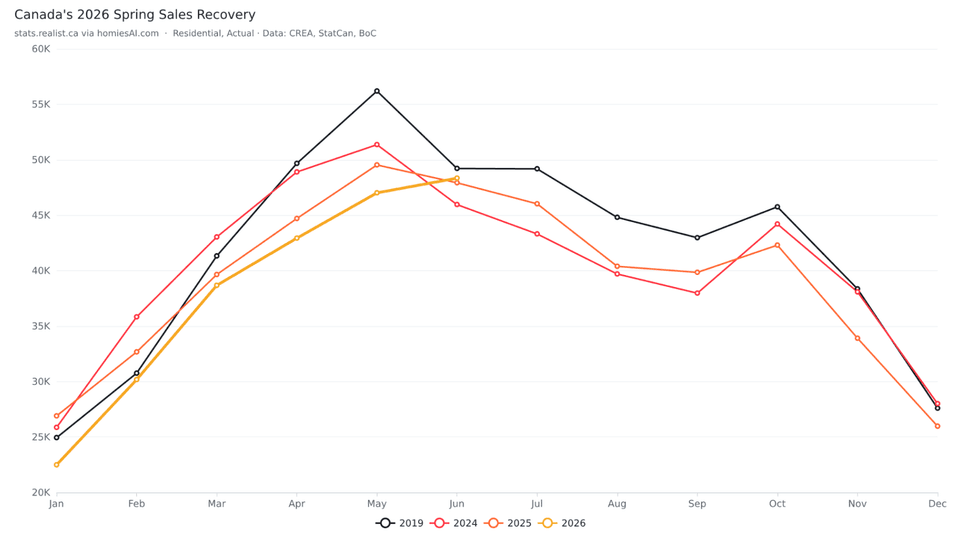

Canada residential unit sales by month, actual, 2019 and 2024-2026. Data through June 2026. Source:

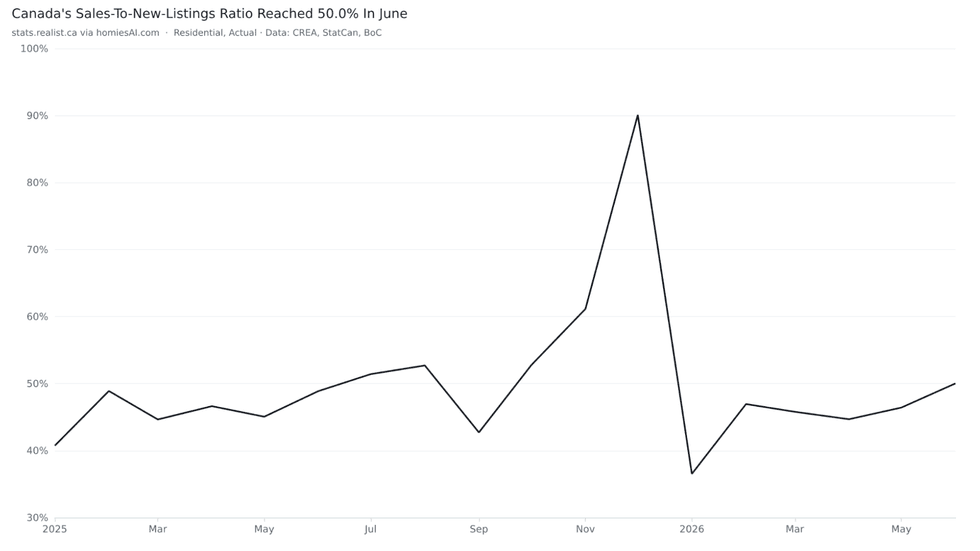

Canada residential unit sales by month, actual, 2019 and 2024-2026. Data through June 2026. Source:  Canada residential sales-to-new-listings ratio, actual, January 2025 to June 2026. Source:

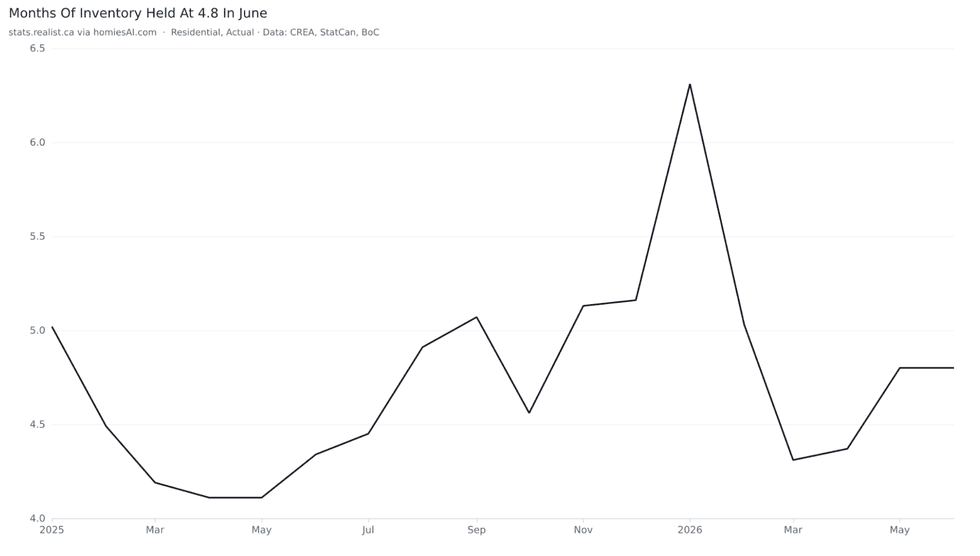

Canada residential sales-to-new-listings ratio, actual, January 2025 to June 2026. Source:  Canada residential months of inventory, actual, January 2025 to June 2026. Source: Source:

Canada residential months of inventory, actual, January 2025 to June 2026. Source: Source:

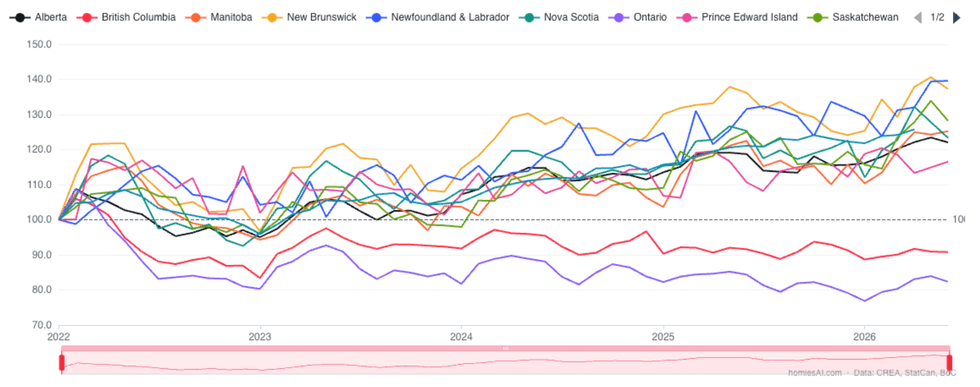

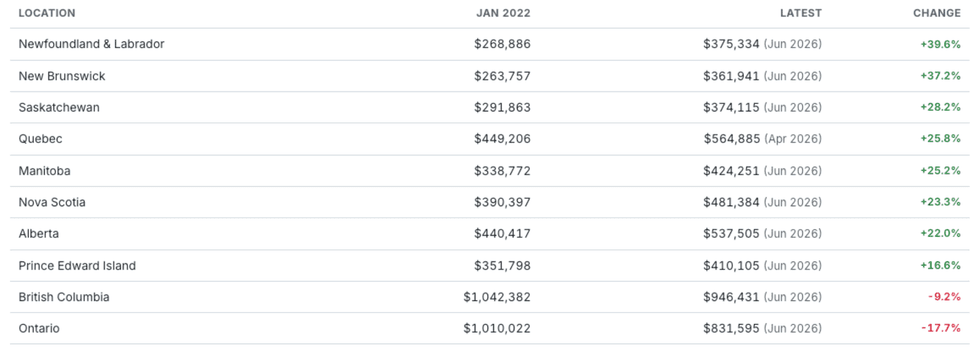

Year-over-year change in residential average sale price for Canada, Ontario, British Columbia and Alberta, January 2022 to June 2026. Average price is shown here as a regional mix measure, not a substitute for HPI or local comparable sales. Source:

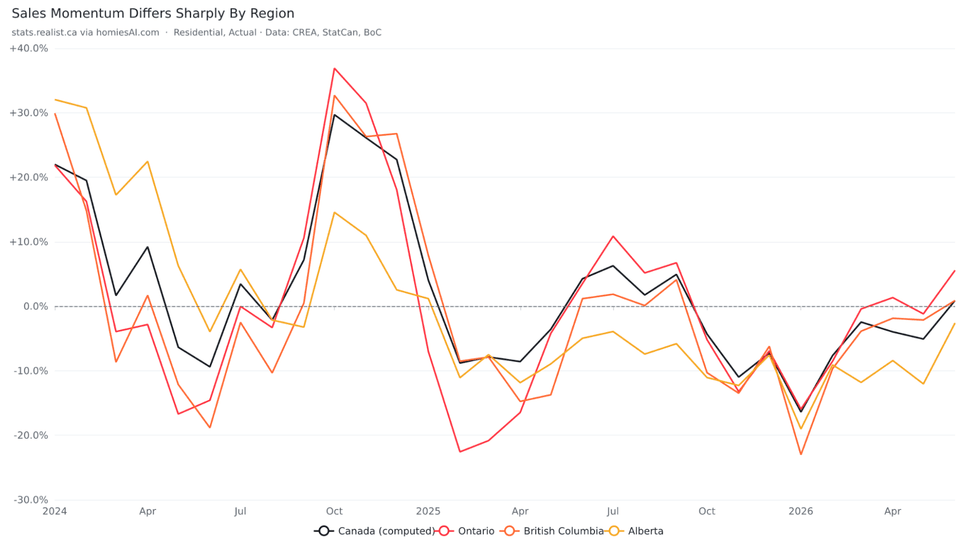

Year-over-year change in residential average sale price for Canada, Ontario, British Columbia and Alberta, January 2022 to June 2026. Average price is shown here as a regional mix measure, not a substitute for HPI or local comparable sales. Source:  Year-over-year change in residential unit sales for Canada, Ontario, British Columbia and Alberta, January 2024 to June 2026. Source:

Year-over-year change in residential unit sales for Canada, Ontario, British Columbia and Alberta, January 2024 to June 2026. Source:

Mattamy WideLot™ design

Mattamy WideLot™ design 'The Cline' at Cityscape

'The Cline' at Cityscape 'The Monarch' at Yorkville

'The Monarch' at Yorkville