Tenant Mix

Explore tenant mix in Canadian commercial real estate — how tenant selection influences traffic, synergy, and investment performance.

June 23, 2025

What is a Tenant Mix?

Tenant mix refers to the variety and composition of tenants within a commercial or mixed-use property, strategically curated to enhance customer traffic and overall profitability.

Why a Tenant Mix Matters in Real Estate

In Canadian commercial real estate, a balanced tenant mix supports stable rental income, reduces vacancy risk, and strengthens a property’s competitive advantage.

Tenant mix strategies include:

- Combining anchor tenants with small businesses

- Grouping complementary retailers (e.g., food + fitness)

- Avoiding tenant redundancy or direct competition

- Ensuring tenant types match target demographics

A successful tenant mix improves customer experience and increases foot traffic, particularly in retail plazas, malls, and mixed-use developments.

Understanding tenant mix is vital for property managers and investors optimizing asset performance.

Example of Tenant Mix in Action

The retail developer selects a grocery anchor, a pharmacy, and a café to create a well-balanced tenant mix that supports all-day customer visits.

Key Takeaways

- Refers to the mix of tenants in a property

- Affects customer traffic and sales synergy

- Strategic mix reduces vacancy and boosts retention

- Essential in commercial property planning

- Impacts leasing and marketing success

(OREA)

(OREA) (OREA)

(OREA)

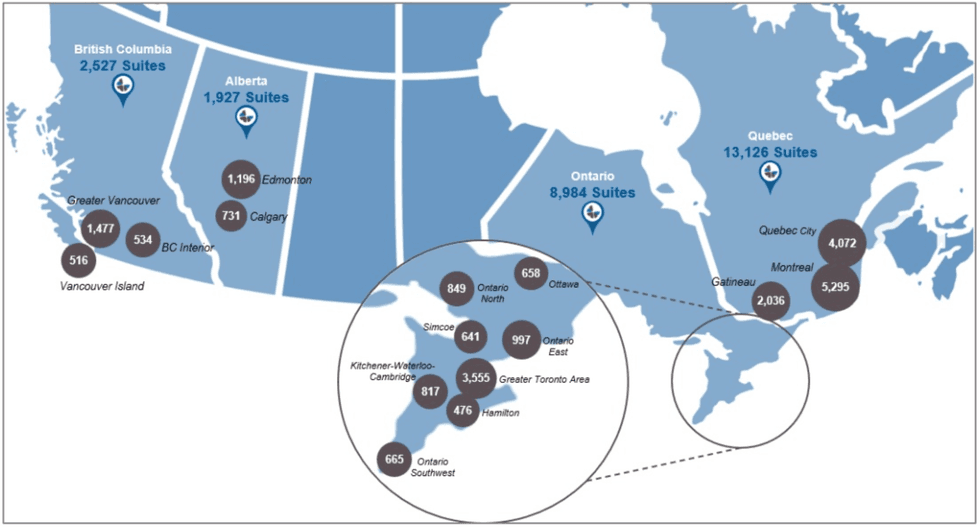

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

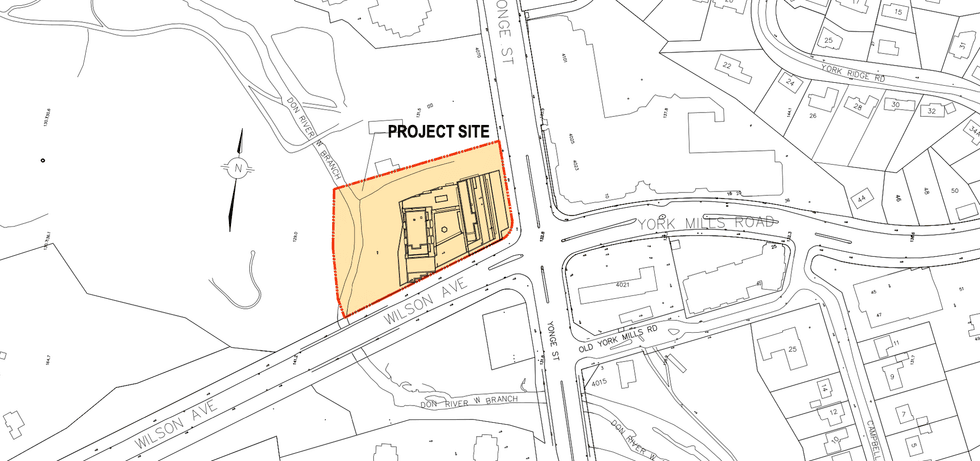

Context plan scale/Arcadis

Context plan scale/Arcadis Rendering of 4050 Yonge Street/Arcadis

Rendering of 4050 Yonge Street/Arcadis

150 Slater Street in Ottawa. (Regional Group)

150 Slater Street in Ottawa. (Regional Group) 150 Slater Street in Ottawa. (Regional Group)

150 Slater Street in Ottawa. (Regional Group)