Debt Service Ratios

Understand debt service ratios in Canadian real estate — how GDS and TDS work, their thresholds, and how lenders use them to approve mortgages.

May 22, 2025

What are Debt Service Ratios?

Debt service ratios are financial metrics used by lenders to assess a borrower’s ability to manage mortgage payments in relation to their income.

Why Do Debt Service Ratios Matter in Real Estate?

In Canadian real estate, two primary ratios are used:

1. Gross Debt Service (GDS) Ratio:- Measures housing costs vs. gross income

- Includes mortgage, property taxes, heating, and 50% of condo fees

- Generally must be under 39%

- Measures all debt obligations vs. gross income

- Includes GDS plus other debts like car loans and credit cards

- Generally must be under 44%

Lenders use these ratios to determine mortgage eligibility. Staying within these limits ensures that homeowners can afford their housing without becoming financially overextended.

Understanding debt service ratios helps buyers prepare for pre-approval, understand loan limits, and evaluate financial readiness.

Example of Debt Service Ratios in Action

A buyer with $6,000 monthly income and $2,100 in housing costs has a GDS of 35%. Including $500 in other debts, their TDS is 43%—within lender guidelines.

Key Takeaways

- Used to evaluate mortgage affordability.

- GDS focuses on housing costs; TDS includes all debts.

- Lenders require ratios within specific limits.

- Helps determine mortgage approval.

- Essential part of financial readiness.

Related Terms

- GDS

- TDS

- Mortgage Qualification

- Pre-Approval

- Lender Guidelines

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

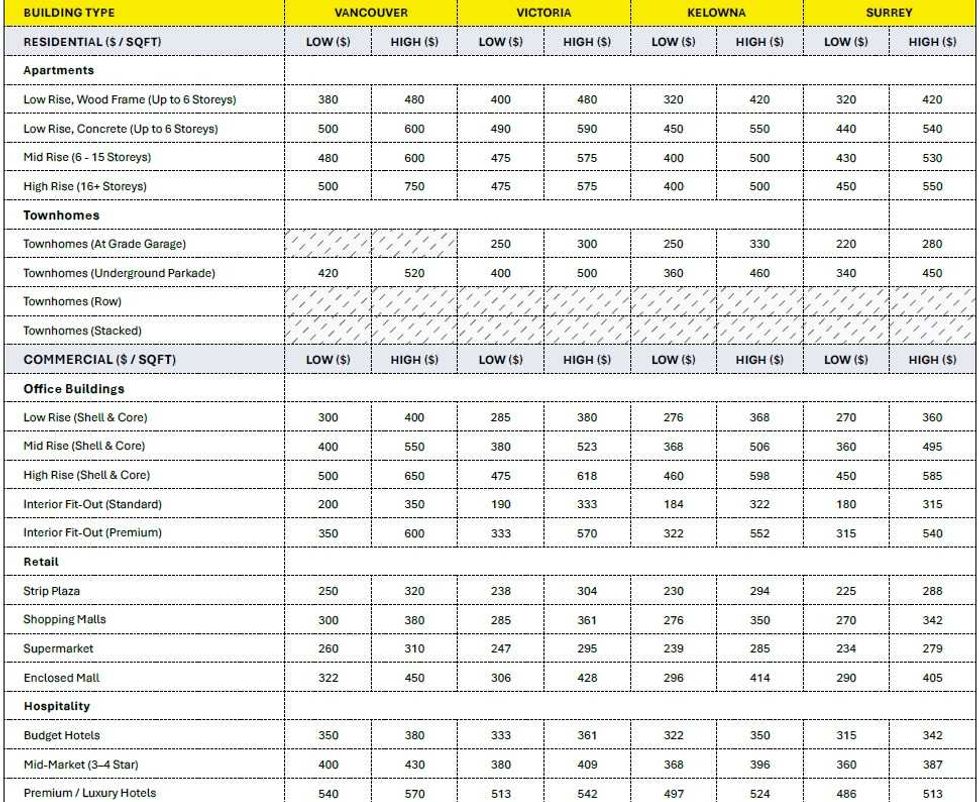

Construction cost ranges for British Columbia. (BTY Group)

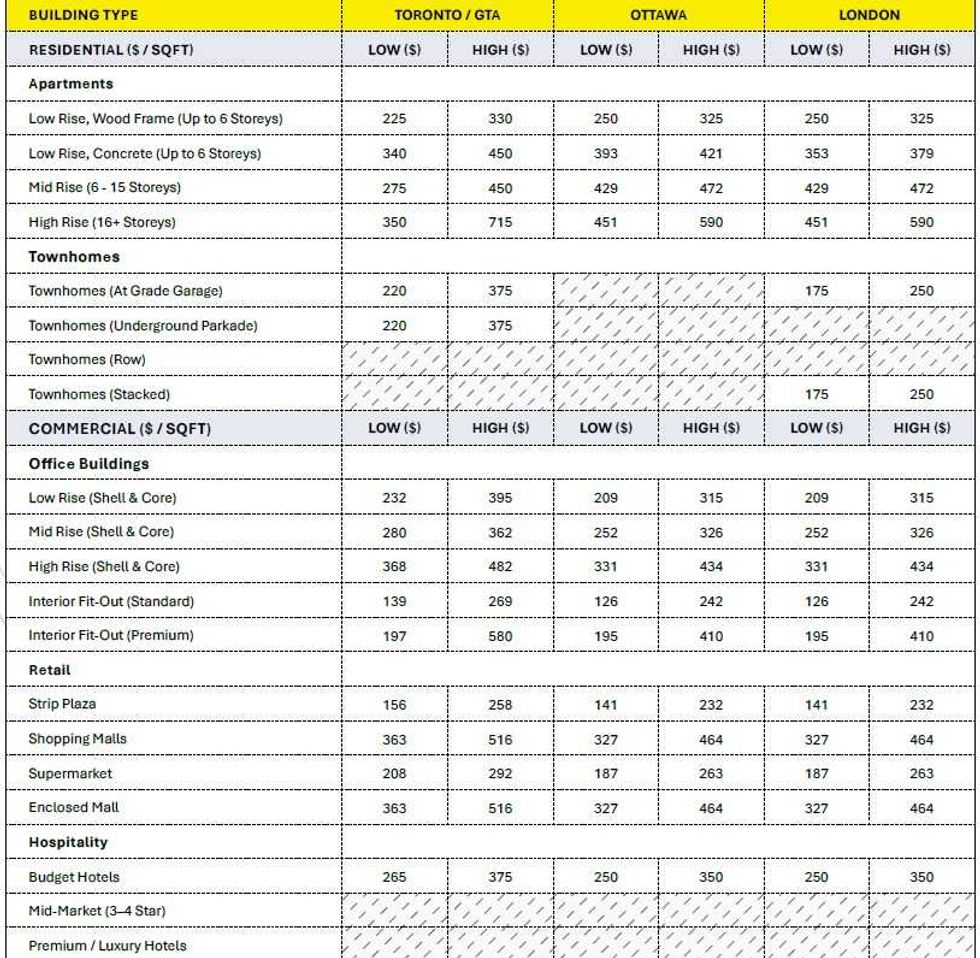

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

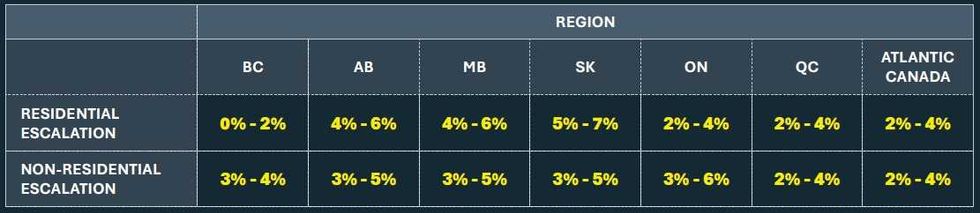

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)