Above Guideline Increase (AGI)

Learn about AGIs (above guideline increases) in Canadian rental law — what they are, when they apply, and tenant protections.

July 28, 2025

What is an Above Guideline Increase (AGI)?

An AGI, or above guideline increase, is a rent increase above the standard annual guideline that landlords can apply for in specific circumstances.

Why AGIs Matter in Real Estate

In Canadian rental law, AGIs allow landlords to recover costs from extraordinary expenses or investments while protecting tenants from arbitrary rent increases.

Common reasons for AGIs:

- Major capital improvements (e.g., new roofs, HVAC)

- Significant increases in taxes or utilities

- Enhanced security services

Understanding AGIs helps landlords and tenants know when such increases are valid and how they are regulated.

Example of an AGI in Action

The landlord applied for an AGI after completing extensive plumbing and electrical upgrades to the building.

Key Takeaways

- Rent increase above annual guideline

- Must be approved by landlord-tenant boards

- Only permitted for qualifying costs

- Tenants can dispute unsupported AGIs

- Ensures fair cost recovery for landlords

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

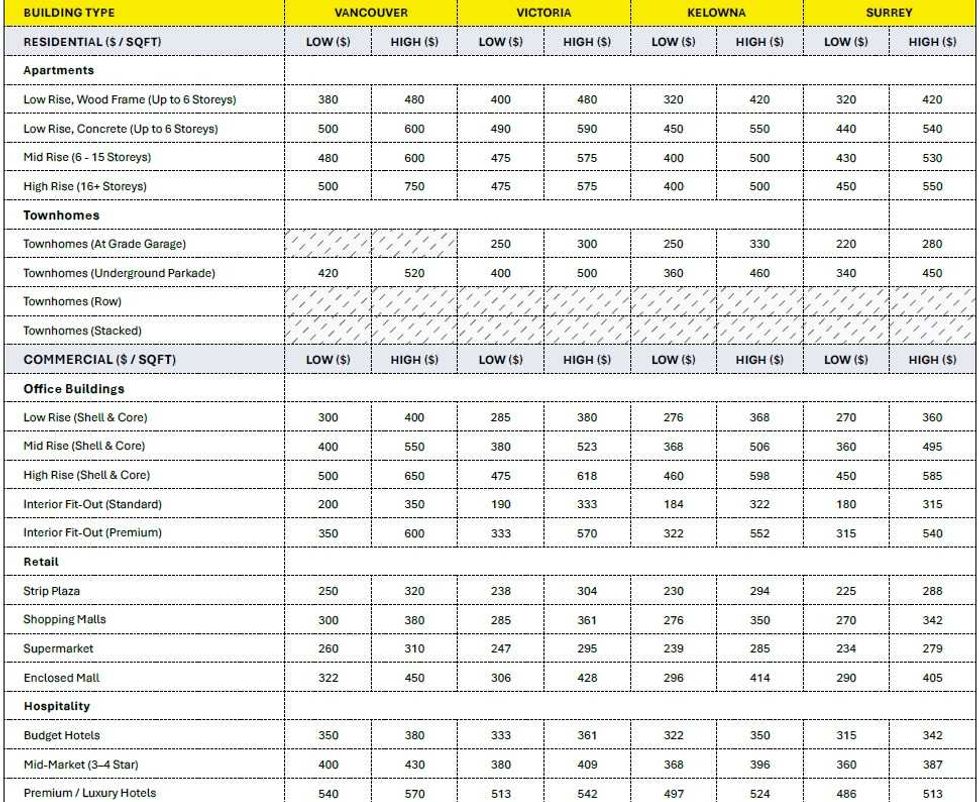

Construction cost ranges for British Columbia. (BTY Group)

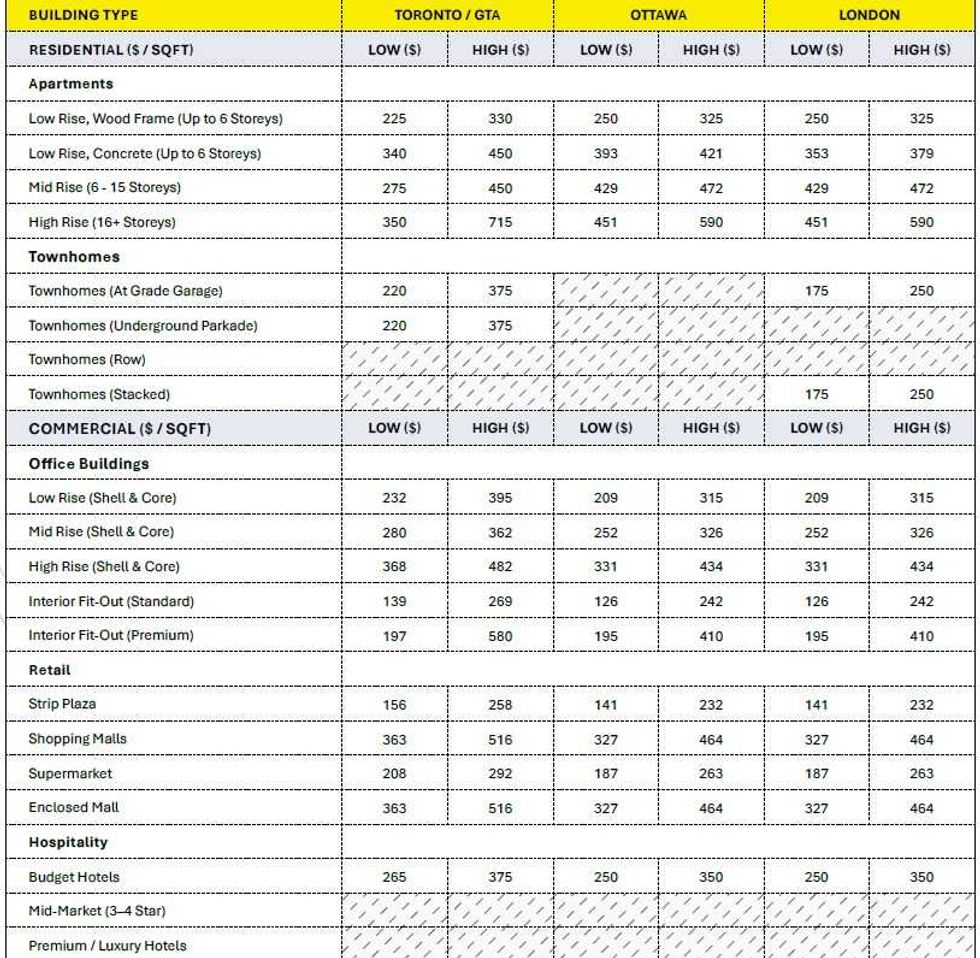

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

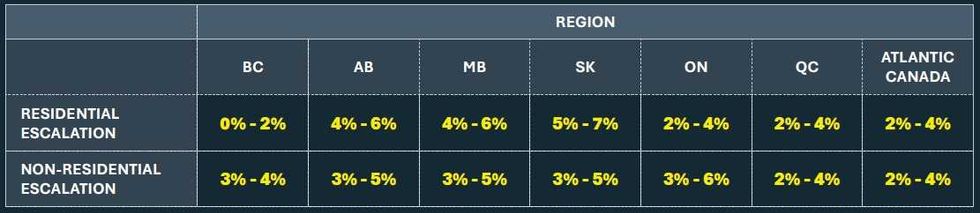

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)

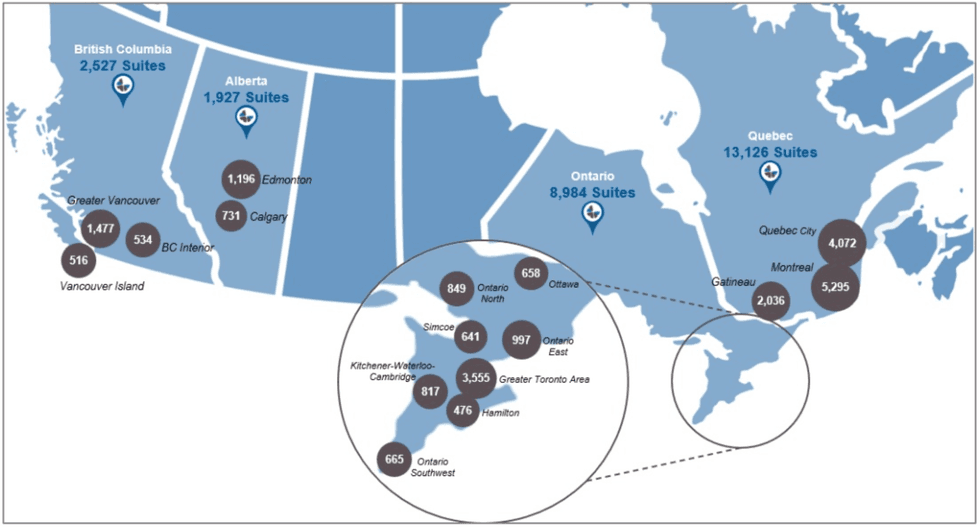

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)