Market Value

Learn what market value means in Canadian real estate, how it’s determined, and why it’s essential for pricing, financing, and smart investing.

May 22, 2025

What is Market Value?

Market value is the estimated price a property would sell for on the open market, assuming both buyer and seller are knowledgeable, willing, and acting without pressure.

Why Market Value Matter in Real Estate

In Canadian real estate, market value serves as the benchmark for pricing, financing, taxation, and investment decisions. It reflects the true worth of a property based on factors such as:- Location and neighbourhood trends

- Recent comparable sales (comps)

- Property condition and features

- Market supply and demand

- Economic conditions and interest rates

Market value is determined through appraisals, Comparative Market Analyses (CMAs) by REALTORS®, or buyer/seller negotiation. It's distinct from assessed value (used for property tax) and listing price (seller's asking amount).

Understanding market value helps sellers set realistic prices, prevents buyers from overpaying, and enables lenders to ensure that a mortgage doesn’t exceed the property’s worth. Investors also rely on accurate market valuations to assess return potential and risk exposure.

In competitive markets, emotional bidding can inflate sale prices above market value, increasing risk for buyers if a lender’s appraisal doesn’t align. Buyers should always seek professional valuation guidance before making a final offer.

Example of Market Value

A home is listed at $850,000, but a local REALTOR®’s CMA shows its market value to be closer to $825,000 based on similar recent sales.

Key Takeaways

- Reflects the price a property would fetch on the open market.

- Based on local comps, condition, and economic trends.

- Used by buyers, sellers, lenders, and appraisers.

- May differ from assessed or listing price.

- Vital for fair negotiation and financing decisions.

Related Terms

- Appraisal

- Listing Price

- Assessed Value

- Comparative Market Analysis (CMA)

- Fair Market Value

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

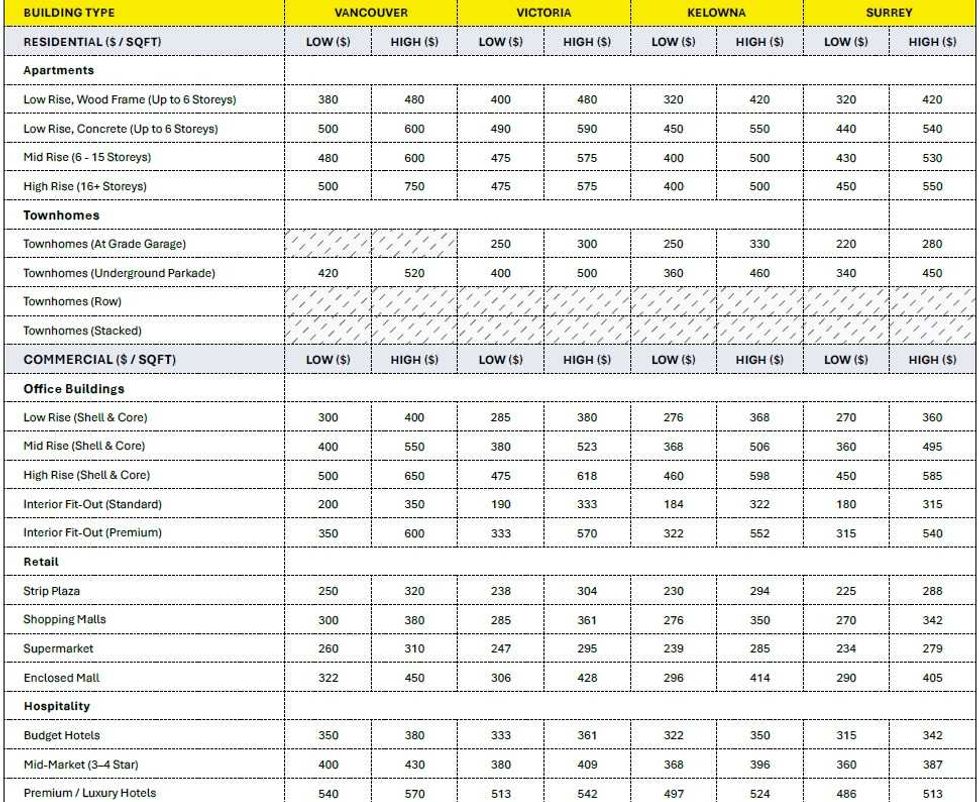

Construction cost ranges for British Columbia. (BTY Group)

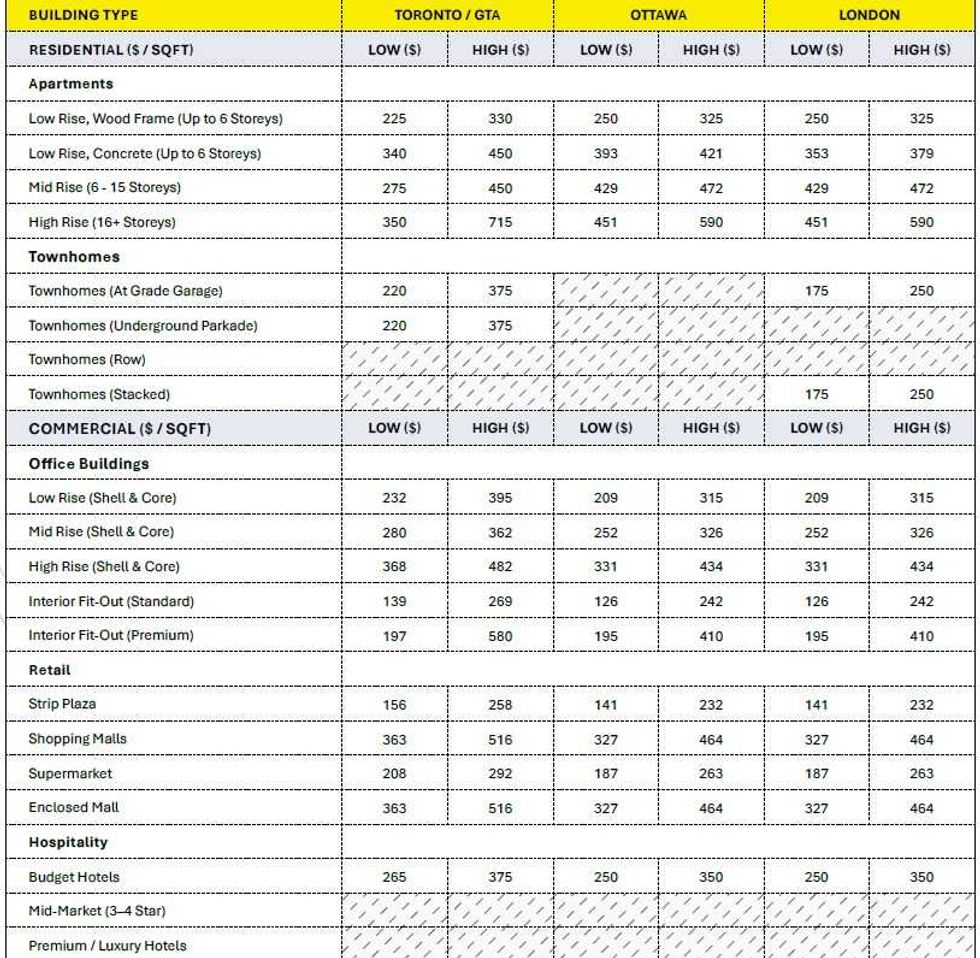

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

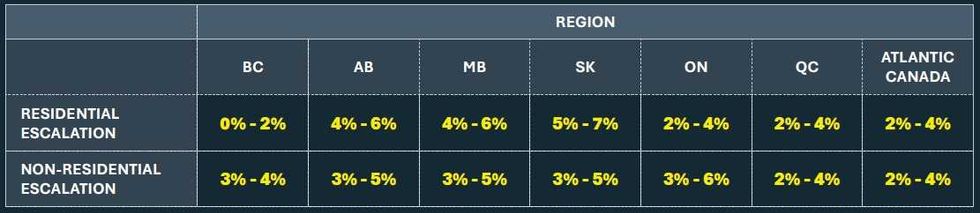

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)

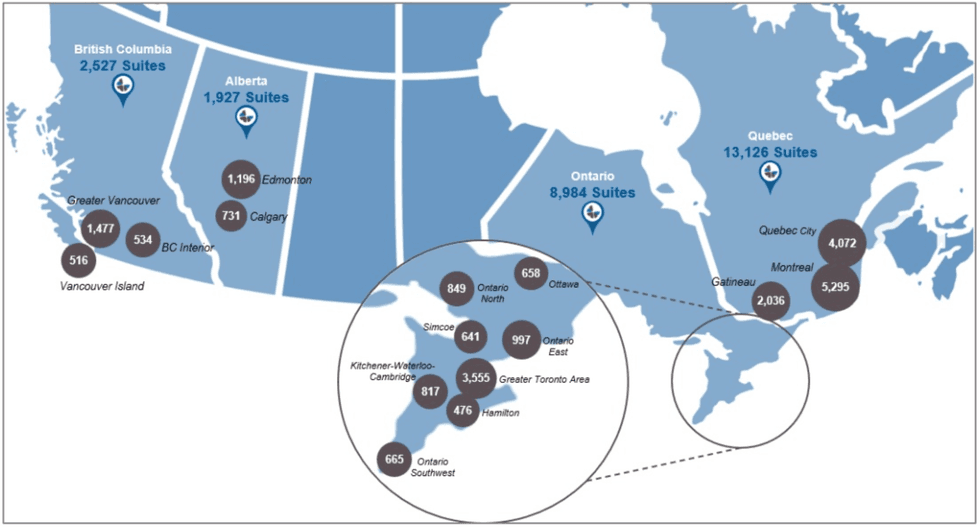

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)