Since the pandemic, investor appetite for office assets has dropped significantly as a result of the increased uncertainty around offices. Have downtowns been changed forever? When will workers return to the office? What are office buildings worth?

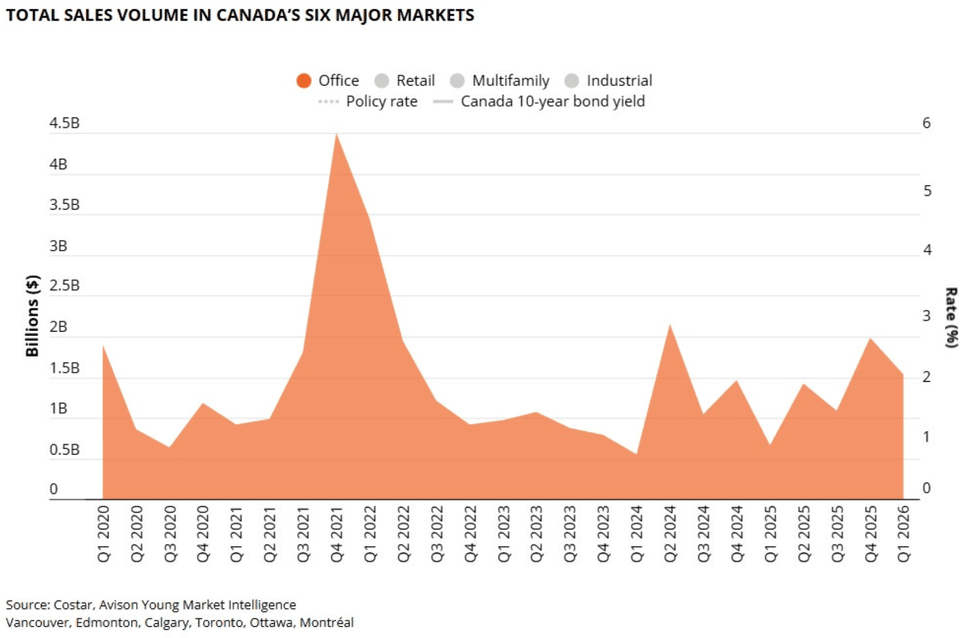

As a result of that uncertainty, office sales as a proportion of all commercial real estate transaction volume dropped to around 17% by 2025, while other sectors like industrial and multi-family saw increases to 38% and 27% — a combined two-thirds.

“Elevated vacancy, opaque pricing, and the lack of clarity around the future of office demand pushed many institutional participants to the sidelines,” said Avison Young in a recent office investment analysis. “But that dynamic is now beginning to shift.”

In Q1 2026, office transactions represented 19% of total sales volume, which is still below the 26% from the 2014-2019 cycle, but nonetheless an improvement.

There are also signs that this cycle is a bit different, as the flight-to-quality trend seen with leasing is also taking form when it comes to sales.

“Since 2025, Trophy office sales accounted for 25% of the total square footage and 39% of the total dollar volume of office sales in Canada,” says Avison Young President Mark Fieder. “This is up considerably from the period 2014 to 2019 and of course a major increase when compared to 2020 to 2024. This supports the narrative of institutional office investors narrowing their focus to core assets with a sustainable competitive advantage to enhance their offering to occupiers.”

According to Avison Young, the office market is now defined by “a pronounced and persistent bifurcation in asset quality” between the trophy segment — newer, Class AAA and A office buildings downtown — and the value-add segment — Class B and C — and this divergence is expected to persist, both in terms of leasing velocity, rent growth, and investor invest.

“After several years of hybrid work, the link between workplace quality, employee engagement, and productivity is now widely acknowledged by occupiers,” said Avison Young. “Office space is no longer treated as a commodity, but as a strategic tool to attract and retain talent.”

“As a result, demand has become increasingly concentrated in best-in-class buildings offering modern design, strong amenity packages, and compelling locations, while unrenovated or poorly positioned assets continue to underperform,” they added.

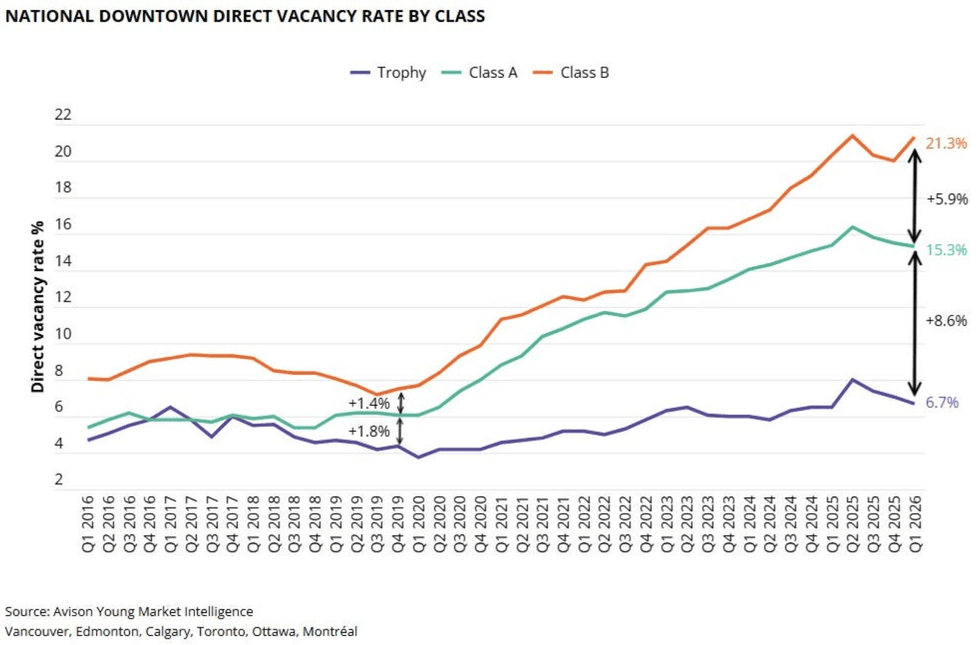

From a vacancy rate perspective, Avison Young notes that there are significant divergences across different classes. The national downtown vacancy rate is 21.3% for Class B buildings, 15.3% for Class A buildings, and just 6.7% for trophy Class AAA buildings. Thus, overall vacancy metrics are no longer useful and “[mask] how tight leasing conditions are for best-in-class space.”

Another reason behind the bifurcation is elevated construction costs, which become a significant factor when it comes to fitting out spaces for tenants.

“Elevated tenant expectations are translating into increasingly sophisticated and costly office fit outs, materially raising the capital intensity of ownership,” Avison Young observed. “Construction cost inflation and higher design standards have driven larger tenant improvement allowances, particularly among larger occupiers for whom high quality build outs are essential to support return to office initiatives.”

“While these allowances allow owners to preserve face rental rates, not all owners have the financial capacity to fund substantial capital programs over extended leasing cycles,” they explained. “This challenge is also prevalent among office investment sales. Increasingly expensive capital expenditures have posed headwinds to demand for vintage or generally undercapitalized assets.”

“Absorption flattened for the first time since 2020, while flight-to-quality trends strengthened. Trophy assets in major downtown cores are now seeing vacancy near 6%, supported by improving leasing momentum and limited competitive supply. Alongside moderating financing conditions, investor confidence has returned.”