Canadian home prices did something unremarkable in June: nothing.

The National Composite MLS Home Price Index was unchanged from May, according to the Canadian Real Estate Association's July 15 release. That flat reading ended a monthly decline that had run since January 2025.

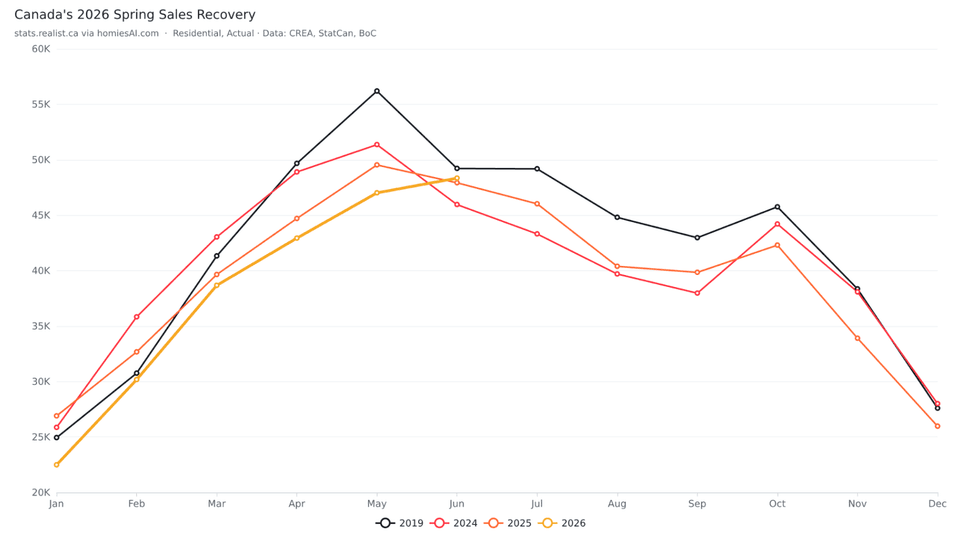

The pause arrived after buyers had already started moving. Seasonally adjusted sales rose 0.5% in June, following gains of 5.5% in May and 0.9% in April. National activity finished June roughly 7% above its March level. Actual sales were 0.9% higher than in June 2025.

Canada residential unit sales by month, actual, 2019 and 2024-2026. Data through June 2026. Source: stats.realist.ca via homiesai.com ai harness for realtors

Canada residential unit sales by month, actual, 2019 and 2024-2026. Data through June 2026. Source: stats.realist.ca via homiesai.com ai harness for realtors

This is an inflection in the transaction data, although it is too early to call a durable price recovery. The annual HPI remained 3.6% below last June. One flat month stops a streak. Several would establish a trend.

Buyers returned as sellers pulled back

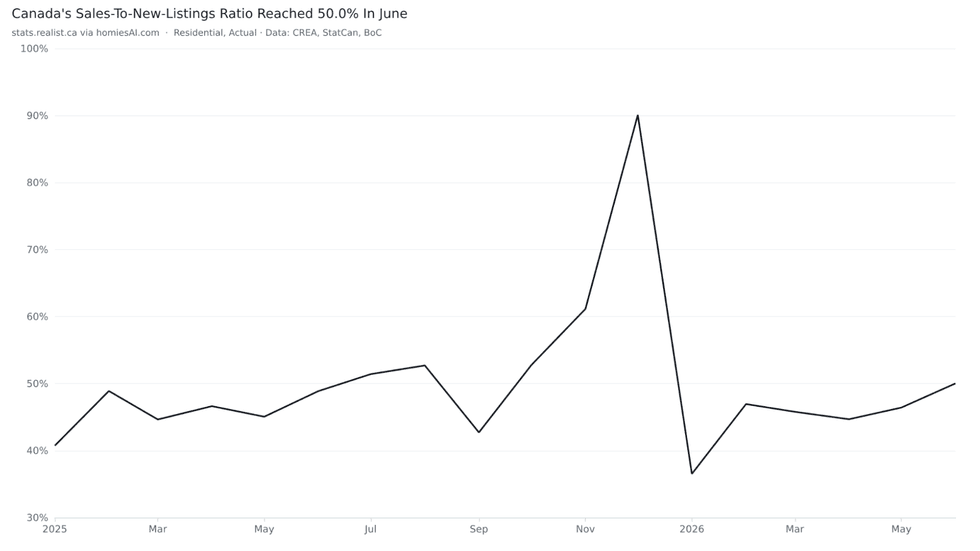

New listings declined 1.3% month over month in June, the second consecutive drop. The combination of slightly higher sales and fewer new listings pushed the sales-to-new-listings ratio to 50.2%, up from 49.3% in May.

CREA considers a ratio between 45% and 65% generally consistent with balanced conditions. At 50.2%, the country is still closer to the middle than either extreme. Buyers lost a little negotiating room in June, rather than losing it altogether.

Canada residential sales-to-new-listings ratio, actual, January 2025 to June 2026. Source: stats.realist.ca via homiesai.com ai harness for realtors

Canada residential sales-to-new-listings ratio, actual, January 2025 to June 2026. Source: stats.realist.ca via homiesai.com ai harness for realtors

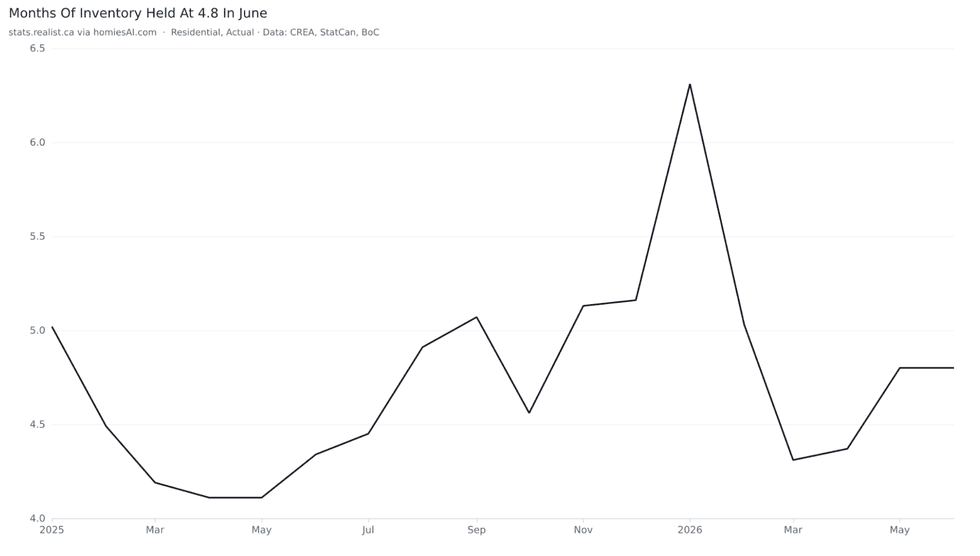

There were 208,578 homes listed for sale at the end of the month, only 0.6% more than a year earlier, and 0.8% above the long-run seasonal average. Months of inventory held at 4.8, its lowest point of 2026 and slightly below the five-month long-run average.

Canada residential months of inventory, actual, January 2025 to June 2026. Source: Source: stats.realist.ca via homiesai.com ai harness for realtors

Canada residential months of inventory, actual, January 2025 to June 2026. Source: Source: stats.realist.ca via homiesai.com ai harness for realtors

The national market has enough inventory to function. The useful inventory is another matter. A well-priced detached home in a tight school district can attract several buyers, while a nearby condo segment remains soft. National balance can contain fierce competition and stale listings at the same time.

Two price measures, two different stories

The average sale price was $696,078 in June, up 0.5% from a year earlier. That appears to conflict with an HPI that fell 3.6% over the same period.

But it does not.

Average price changes when the mix and geography of sales change. If more expensive homes or more homes in high-priced markets trade, the national average can rise. HPI attempts to track the price of a benchmark home by controlling for property attributes.

For national direction, the HPI is the better signal. For the value of a specific property, neither measure replaces current comparable sales.

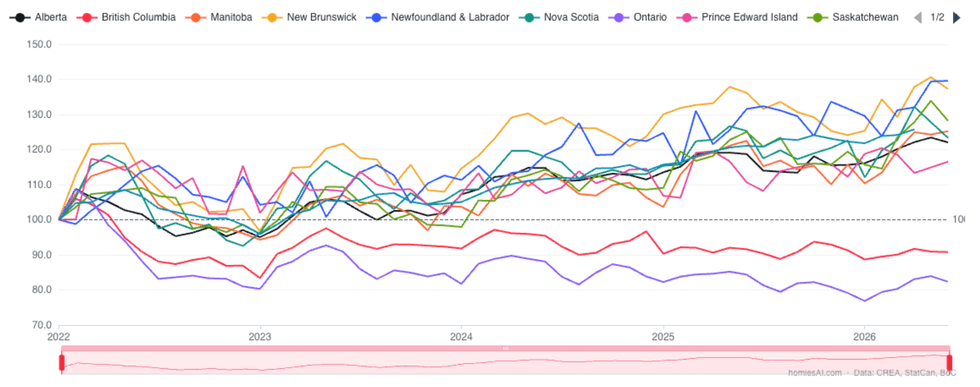

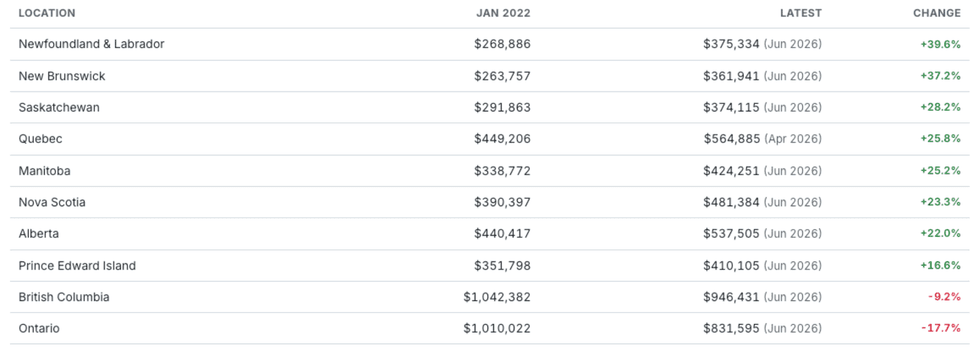

Regional HPI prices remained below last year's levels in British Columbia, Alberta, and Ontario, although CREA said the declines have narrowed as prices stabilize. Nova Scotia recorded its first annual decline in more than three years. Still, most markets outside of Ontario and BC are up significantly since the rate hiking cycle started:

Year-over-year change in residential average sale price for Canada, Ontario, British Columbia and Alberta, January 2022 to June 2026. Average price is shown here as a regional mix measure, not a substitute for HPI or local comparable sales. Source: stats.realist.ca via homiesai.com ai harness for realtors

Year-over-year change in residential average sale price for Canada, Ontario, British Columbia and Alberta, January 2022 to June 2026. Average price is shown here as a regional mix measure, not a substitute for HPI or local comparable sales. Source: stats.realist.ca via homiesai.com ai harness for realtors

That regional divergence complicates the recovery narrative. Ontario and B.C. are perceived to have have room to rebound on sales from weak transaction levels. Some markets that benefited from stronger population inflows and interprovincial migration are cooling from a higher base.

CREA cut its 2026 sales outlook

CREA's revised July 15 forecast calls for 463,336 residential sales in 2026, down 1.4% from 2025. The national average price is forecast at $686,710, up 1.1%.

Ontario is the only province where CREA expects sales to grow in 2026. At the same time, average prices in Ontario and British Columbia are forecast to decline by less than 1%. That combination is plausible: transactions can recover from weak levels without restoring broad pricing power.

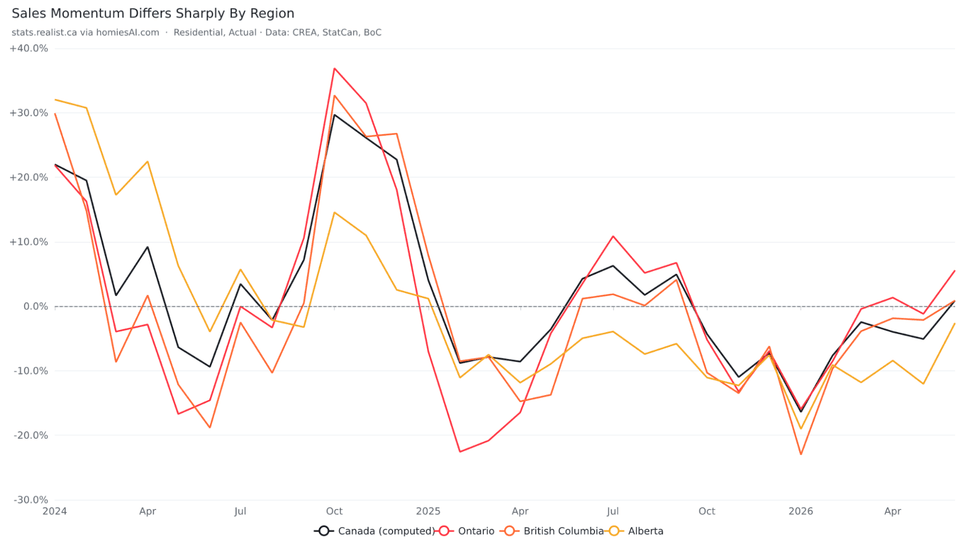

Year-over-year change in residential unit sales for Canada, Ontario, British Columbia and Alberta, January 2024 to June 2026. Source: stats.realist.ca.

Year-over-year change in residential unit sales for Canada, Ontario, British Columbia and Alberta, January 2024 to June 2026. Source: stats.realist.ca.

For 2027, CREA projects 480,567 sales, up 3.7%, and an average price of $694,164, up 1.1%. The stronger transaction recovery is therefore pushed into next year.

The forecast and the June actuals should be read separately. June sales momentum improved, and fixed rates eased from their April peak, but CREA still expects the weak start to 2026 to leave full-year sales below 2025. Inflation, bond yields and employment can still change the path. Pent-up demand only becomes a transaction when a household qualifies for the mortgage.

What the June turn changes

Buyers heading into fall should have financing and property criteria ready before Labour Day. A balanced market still permits conditions, inspections and negotiation in many segments. Scarce, well-priced homes will move faster than the national statistics suggest.

Sellers have a better setup than they had in early spring, but a flat national HPI does not create local pricing power. The relevant evidence is current competing inventory, recent firm sales, days on market, and the alternatives available to a buyer that weekend.

Investors can increase acquisition effort without increasing their price assumptions. Underwriting should begin with current rent, normalized expenses, debt service, necessary capital work and stabilized yield. Resale value belongs in a sensitivity analysis. Paying for a recovery before the property's income supports the basis is still a bad deal.

The next test comes after summer. Sales need to hold their gains. New listings need to remain absorbable when sellers return after Labour Day. The HPI needs more than one flat reading.

June improved the odds of a busier second half. The market has stopped sliding nationally. Local price discovery will decide how much of that momentum survives the fall.