CMHC Insurance

Learn what CMHC Insurance is, when it's required in Canadian real estate, how much it costs, and how it affects homebuyers with low down payments.

May 22, 2025

What is CMHC Insurance?

CMHC Insurance, also known as mortgage loan insurance, is a government-backed insurance policy provided by the Canada Mortgage and Housing Corporation (CMHC) that protects lenders in case a borrower defaults on a high-ratio mortgage.

Why CMHC Insurance Matters in Real Estate

In Canada, homebuyers who make a down payment of less than 20% are required by law to obtain mortgage loan insurance from CMHC or another approved provider. This insurance protects the lender — not the borrower — by covering losses in the event of mortgage default.

While it doesn’t benefit the buyer directly, CMHC Insurance enables them to purchase a home with as little as 5% down, which is crucial in high-priced housing markets. It helps stabilize the housing market and reduces risk for lenders, making mortgages more accessible to Canadians with lower savings.

The cost of CMHC Insurance is based on a sliding scale tied to the loan-to-value ratio and is typically added to the mortgage principal or paid as a lump sum. Premiums range from 2.8% to 4% of the mortgage amount, depending on the size of the down payment.

Understanding CMHC Insurance is key for budgeting, especially for first-time homebuyers, and for making informed decisions about down payment strategy and overall affordability.

Example of CMHC Insurance

A buyer in Ontario purchases a $500,000 home with a 10% down payment. Since this is less than 20%, they must pay a CMHC Insurance premium of $13,950, which is added to their mortgage.

Key Takeaways

- Required for down payments under 20%.

- Protects the lender in case of borrower default.

- Provided by CMHC and other approved insurers.

- Cost is based on mortgage size and down payment.

- Enables access to homeownership with smaller savings.

Related Terms

- High-Ratio Mortgage

- Loan-to-Value Ratio (LTV)

- Mortgage Default

- Down Payment

- Mortgage Pre-Approval

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

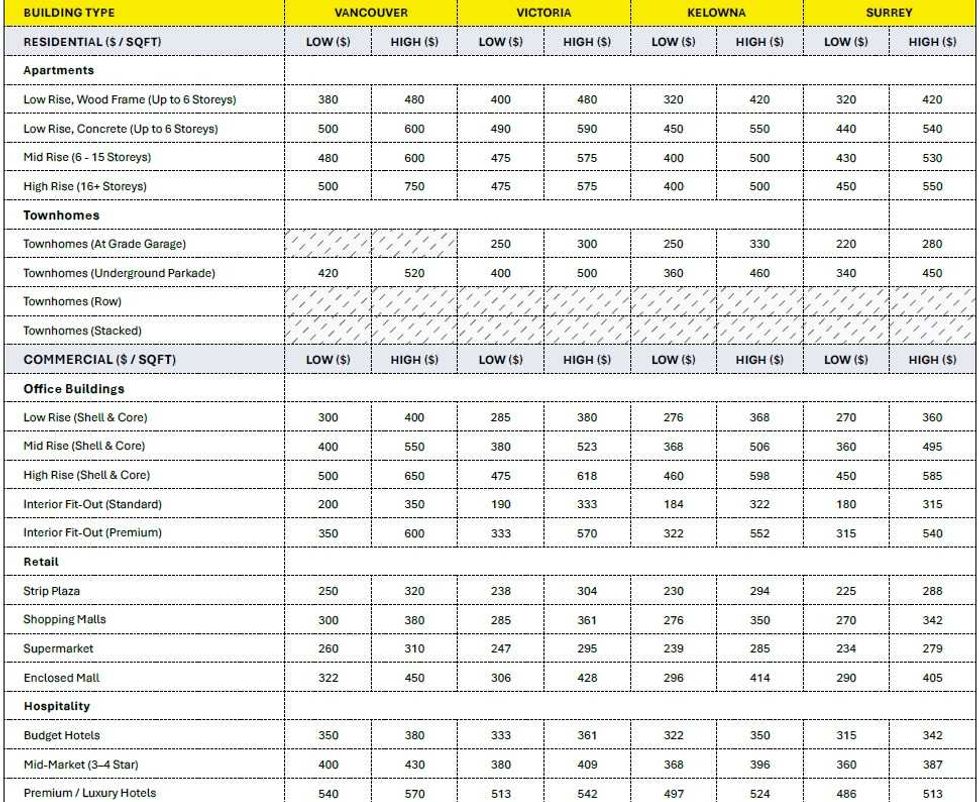

Construction cost ranges for British Columbia. (BTY Group)

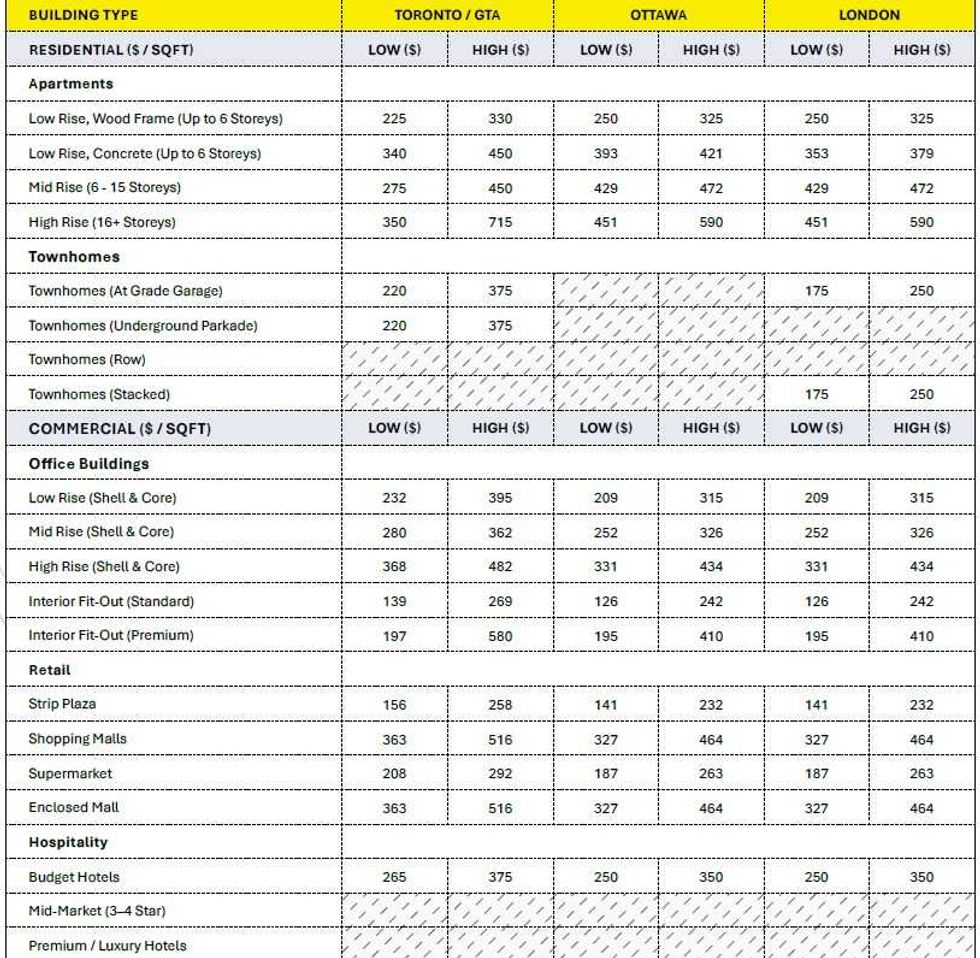

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

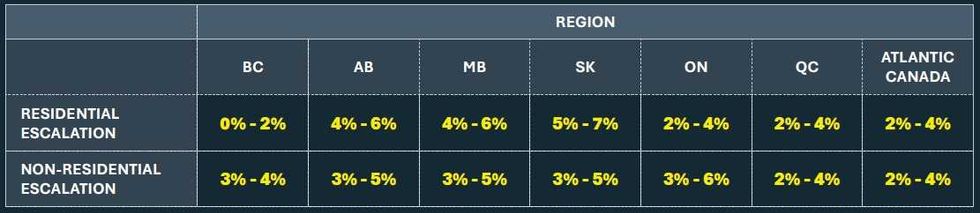

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)