Canada's largest city is on track to lose over 42,000 jobs as a result of the coronavirus pandemic, which has made Toronto's economy "drastically weaker" this year, according to a new report from the Conference Board of Canada.

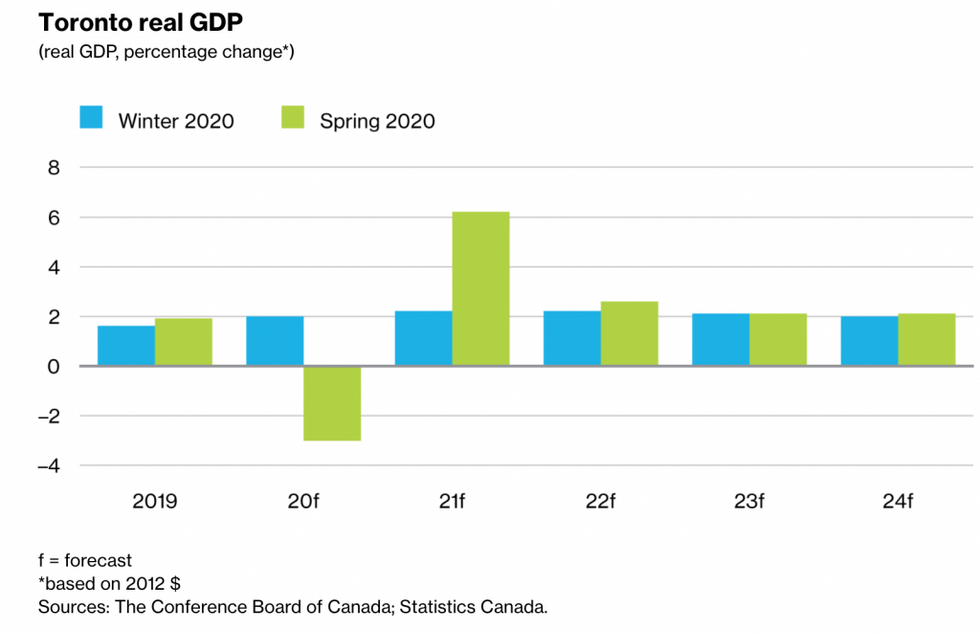

While the weight of the virus is being felt now — as physical distancing requirements and the closure of all non-essential businesses have brought a large portion of the economy to a standstill — the report predicts Toronto's economy is poised to rebound next year with GDP growth of 6.2%.

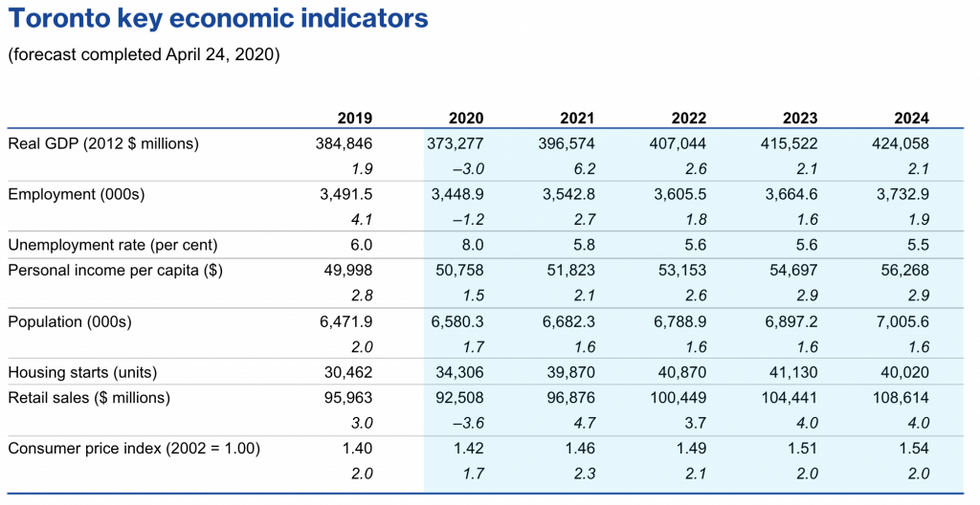

According to the report, Toronto's GDP is expected to fall by 3% this year, which includes a 1.0% contraction in this year’s first quarter and a 6% drop in the second.

In comparison, on a national level, Canada is in the midst of an "economic crisis" and the Conference Board of Canada says it's forecasting the country's real GDP to contract at an annualized pace of almost 5% in the first quarter of the year.

However, in the second quarter, the decline will hit 25%. To put that into perspective, the report says that until now the largest hit to GDP in the past 60 years was the 8.7% contraction in the first quarter of 2009.

READ: Home Prices in Toronto Could Drop More Than 14% By 2023: Report

Over 42,600 jobs will vanish in Toronto due to COVID, bringing the unemployment rate to 8%, according to the data. In the second quarter alone, employment is anticipated to fall by 5%, while the city's unemployment rate is expected to reach 13.9%. However, it's predicted that Toronto's labour market will recover some of the lost ground in 2021, with employment growth expected to rise 2.7%.

The report also revealed Toronto's residential construction sector struggled in 2019 because of a combination of "higher interest rates, high levels of consumer debt, and the tighter mortgage rules imposed by the federal governments in 2018," ultimately leading to slow demand for new homes.

Last year, total housing starts fell to 30,462 units — a 25.9% decline from 2018 — but despite the fallout from the pandemic, housing starts are expected to increase to 34,306 units this year, thanks to low-interest rates and supportive federal programs. What's more, the Conference Board of Canada believes these policies, in combination with the economic recovery, will lay the foundation for starts to rise to 39,870 units in 2021.

The data shows a strong recovery in 2021 following COVID-19 pandemic: Conference Board of Canada

The data shows a strong recovery in 2021 following COVID-19 pandemic: Conference Board of Canada

The data revealed Toronto's local retail trade sector will feel "the pinch" of the pandemic, with retail sales forecast to fall by 3.6% this year — the largest drop since 1991. However, while retail sales are expected to recover in the second half of this year, they will not return to pre-crisis peak until the end of 2021.

The report also notes that Toronto's "vibrant" labour market has also taken a hit as a result of COVID, as well. Over the past two years, Toronto welcomed 95,534 new arrivals per year, which allowed the population to grow by 2% in both 2018 and 2019. The pandemic will cut net in-migration to the region to 65,710 this year, ultimately slowing population growth by 1.7%.

Not surprisingly, the report says public administration, health care, and construction industries will emerge from the pandemic relatively unscathed, with all three posting growth this year. Additionally, the report says output in the finance, insurance, and real estate sector — Toronto’s largest industry — will remain essentially flat in 2020.

Also not a surprise, is that the pandemic is expected to create "recession-like conditions" in the accommodations and food industry, where output is forecast to contract by 40.2% and in arts, entertainment, and recreation industries, which will contract by 17.8%.

Conference Board of Canada

Conference Board of Canada

Looking ahead, while Toronto's GDP is set to decline by 3% this year, it will jump back up 6.2% in 2o21, suggesting the city's economy could have a strong resurgence.

Toronto has already established an economic recovery task force to deal with the aftermath of COVID-19. The team will “identify immediate and long-term economic strategies for residents and businesses, with a focus on supporting those segments of the economy that are most strongly impacted by COVID-19, such as tourism, hospitality, and entertainment.”

Plans for the economy to reopen are already underway.