Real Estate Lawyer

Learn how real estate lawyers support Canadian buyers and sellers during property transactions, including title searches, legal documents, and closing procedures.

May 22, 2025

What is a Real Estate Lawyer?

A real estate lawyer is a legal professional who specializes in property law, assisting with the legal aspects of buying, selling, or refinancing real estate.

Why Do Real Estate Lawyers Matter in Real Estate

In Canadian real estate, lawyers are often required to complete transactions. They ensure all legal documentation is properly prepared and reviewed, and that the title transfer process is completed without issues.

Roles of a real estate lawyer include:

- Reviewing the Agreement of Purchase and Sale

- Conducting title searches

- Arranging title insurance

- Handling mortgage registration

- Managing closing funds in trust accounts

A lawyer protects the buyer’s or seller’s legal interests and ensures the transaction complies with provincial real estate law. They are especially critical in complex cases such as:

- Estate sales

- Foreclosures or power of sale

- Disputes over easements or zoning

Understanding the role of a real estate lawyer helps ensure that your property transaction proceeds smoothly, lawfully, and with minimized legal risk.

Example of a Real Estate Lawyer in Action

A homebuyer in Alberta hires a real estate lawyer to review their purchase agreement, ensure the title is clear, and handle the legal closing process.

Key Takeaways

- Manages legal aspects of real estate deals.

- Required for closings in most provinces.

- Ensures title and funds are properly transferred.

- Reviews legal documents and resolves disputes.

- Protects client interests in property transactions.

Related Terms

- Notary Public

- Title Search

- Agreement of Purchase and Sale

- Closing Process

- Trust Account

Targets under the new 10-year plan. (Metro Vancouver)

Targets under the new 10-year plan. (Metro Vancouver)

(OREA)

(OREA) (OREA)

(OREA)

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

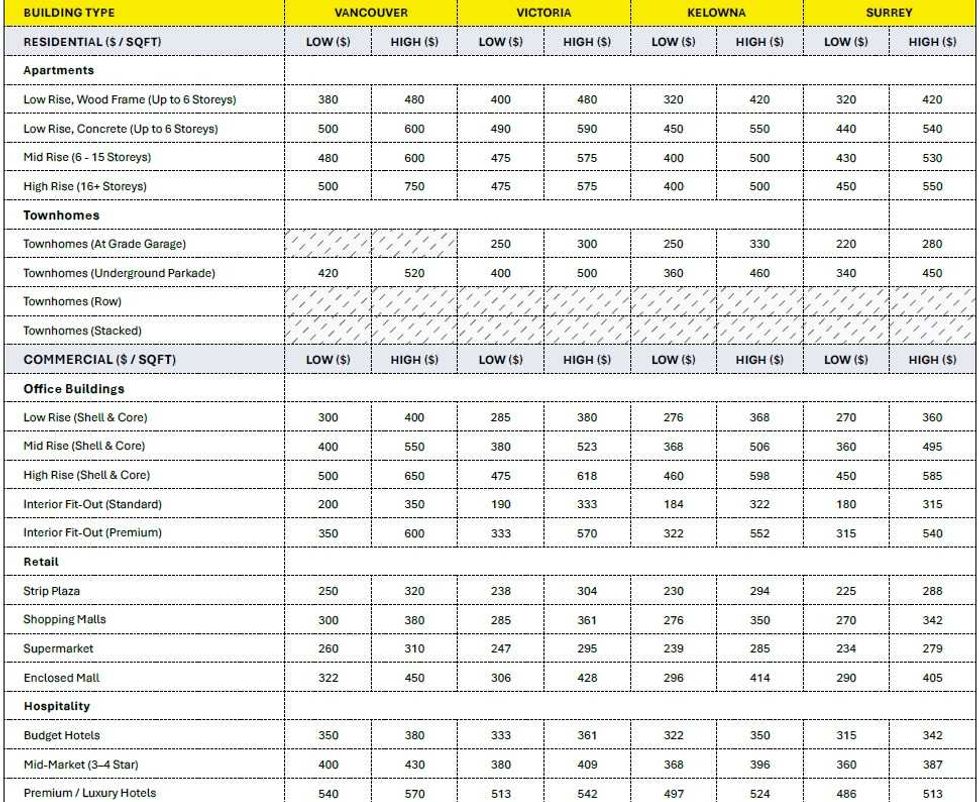

Construction cost ranges for British Columbia. (BTY Group)

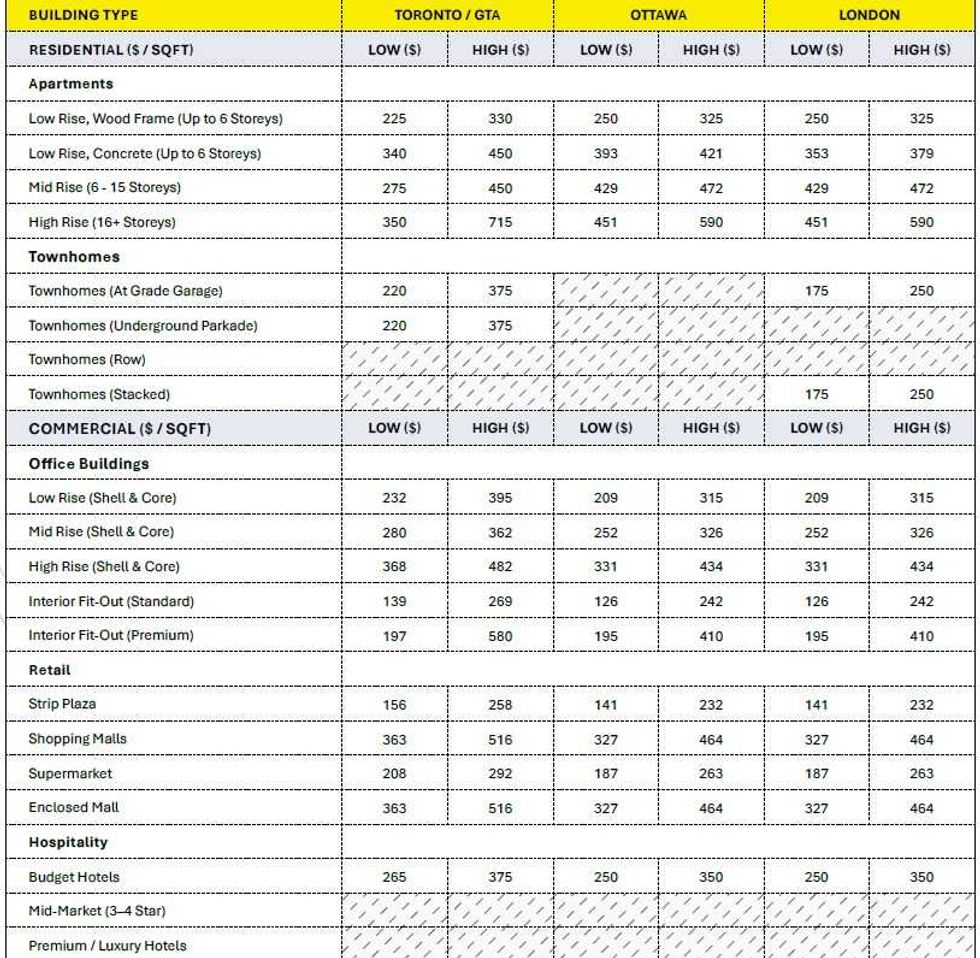

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

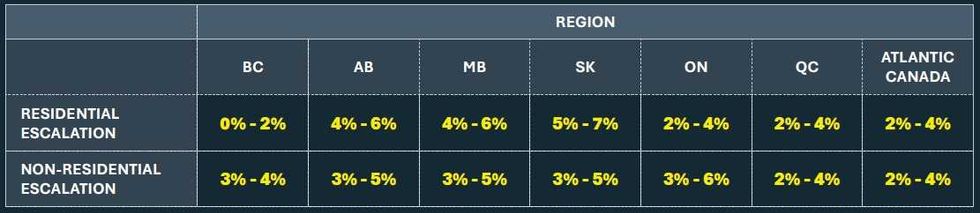

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)