As the housing crisis in Canada became harder (and harder) to ignore, governments big and small have started taking more (and more) action. But not all actions are equal, and some may actually have a negative impact on housing affordability.

As complicated as the housing crisis may be, it really comes down to the basic law of supply and demand: If demand increases while supply stays flat, prices will increase.

This is why, according to a recent analysis article published by the CMHC, demand-side interventions by governments may actually reduce housing affordability in the long-term.

“Demand-side interventions, which directly help households secure housing, are often favoured because of their more immediate impact,” said CMHC Chief Economist and SVP of Housing Insights Mathieu Laberge. “The results are easier to see and measure compared to building new homes, which take years to deliver. “

Demand-side interventions are those that enable people to afford housing, such as by increasing household income or reducing housing costs. Recent examples include the Government of British Columbia’s Attainable Housing Initiative and the Government of Canada’s First-Time Homebuyers GST Rebate.

Laberge didn’t call out any real-world examples, but said that demand-side interventions can generate immediate new demand for housing that puts renewed upwards pressure on housing prices — for everyone, not just those who benefit from the intervention.

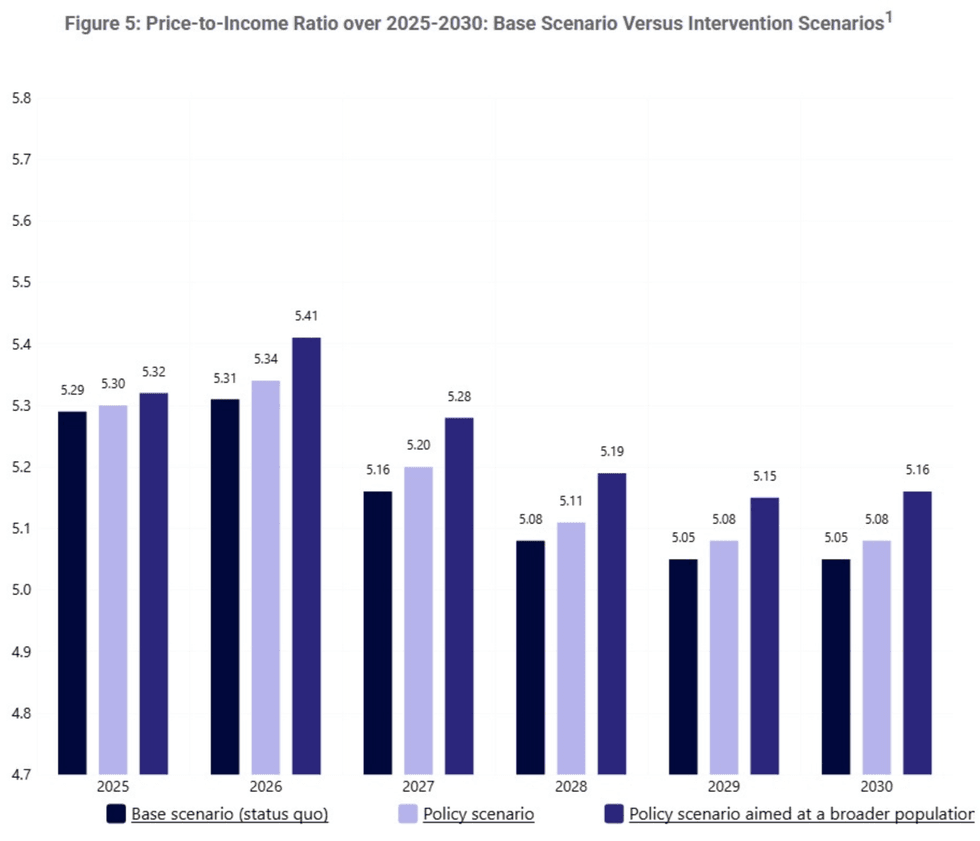

To prove this out, Laberge used two model scenarios: a limited scenario where support is provided to 20% of potential homebuyers, and an ambitious scenario where support is provided to 70% of potential homebuyers, with the support being a 4% reduction in monthly mortgage payments.

According to their modeling, 17,000 people would attain homeownership in the limited scenario, but the number would decrease over time because the increased demand would raise prices by 0.6%. The economic cost for the government would be between $2.7 billion and $4.3 billion, while also creating $1.6 billion in unintended increased costs for homebuyers who did not benefit from the support.

In the ambitious scenario, 52,000 people would attain homeownership, and everybody else would face a 2.1% increase in prices. The economic cost for the government would be $9.3 billion to $11.4 billion, while creating $2.1 billion in unintended increased costs for homebuyers who did not benefit from the support.

“The bottom line for both interventions is clear: While they support access to homeownership for a select group, they impose costs on a much larger number of households,” said Laberge. “As a result, housing affordability would decrease across the board with the broader intervention.”

(CMHC)

(CMHC)

Recognizing the social benefit of these kinds of actions, Laberge isn’t steadfastly against demand-side interventions, and suggests two ways to mitigate the negative impact on affordability.

The first is to target interventions as strategically as possible to those with the greatest need, in order to cap the increase in demand and the resulting pressure on prices, such as in the aforementioned limited scenario. “This makes demand-side interventions more niche, but still relevant for supporting some of the most vulnerable populations,” said Laberge.

The second way is to match demand-side interventions with proportionate new supply that would offset the price increase from increased demand. In the limited scenario, 7,800 new housing starts annually would help offset the impact, while 28,000 new starts would be needed in the ambitious scenario. “The broader and less targeted the intervention, the greater the increase in housing starts needed to offset the adverse impact,” said Laberge.

“Each intervention tool has its own benefits and drawbacks,” he concluded. “Demand-side interventions have the benefit of providing immediate relief, but can still harm housing affordability in the long term if not used carefully. Supply-side interventions are slow to impact affordability given the time it takes to build housing, but they positively impact a much broader range of households. The overarching conclusion is clear: They both go hand-in-hand.”