Six years later, office markets across the country (and beyond) are still feeling the impacts of the COVID-19 pandemic, which changed the world forever by making remote work mainstream. But things are on the upswing.

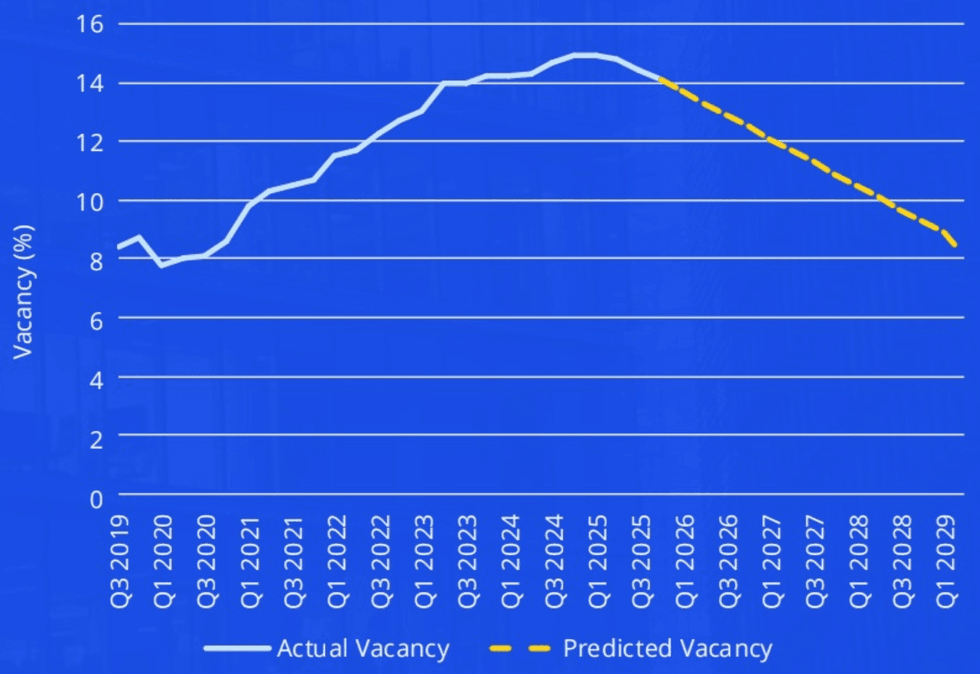

In Q1 2020, at the onset of the pandemic, the national office vacancy rate was just under 8% according to commercial real estate services firm Colliers. Since then, it has been steadily increasing every quarter until about midway through 2025, when it peaked at 14.9%.

We are now over the hump, and the national office vacancy rate is beginning to decline as governments and institutions — and large companies — continue mandating employees return to office.

According to AI-powered modelling and economic forecasts, Colliers says the national office vacancy rate is projected to decline back down to 8% by Q1 2029 — close to a decade after we first learned of the pandemic.

(Colliers)

(Colliers)

According to Colliers, the average in-office mandate has also been steadily increasing. In Q4 2022, the average was 2.5 days with about 49% of companies finalizing that plan. Those numbers jumped to 3.0 days and 55% by Q2 2023, 3.3 days and 62% by Q4 2023, and was at 3.5 days and 68% following Q4 2025.

“In the second half of 2025, downtown Toronto saw high levels of leasing activity not seen in well over a decade,” said Senior Managing Director of Brokerage Jon Olynick in a Colliers report published last month. “Return to office mandates by the Big Banks and the provincial government was a dominant factor, which has also carried over into Q1 2026.”

Such leases from the past two quarters include CIBC leasing 258,197 sq. ft at 8 Spadina Ave (The Well) and Scotiabank leasing 63,461 sq. ft at 3389 Steeles Avenue East (Steeles Technology Campus) in Q4 2025, and RBC leasing 326,347 sq. ft at 200 Front Street West (Simcoe Place) and Scotiabank leasing another 104,966 sq. ft at 351 King Street East (Globe and Mail Centre) in Q1 2026, the last of which was a sublease.

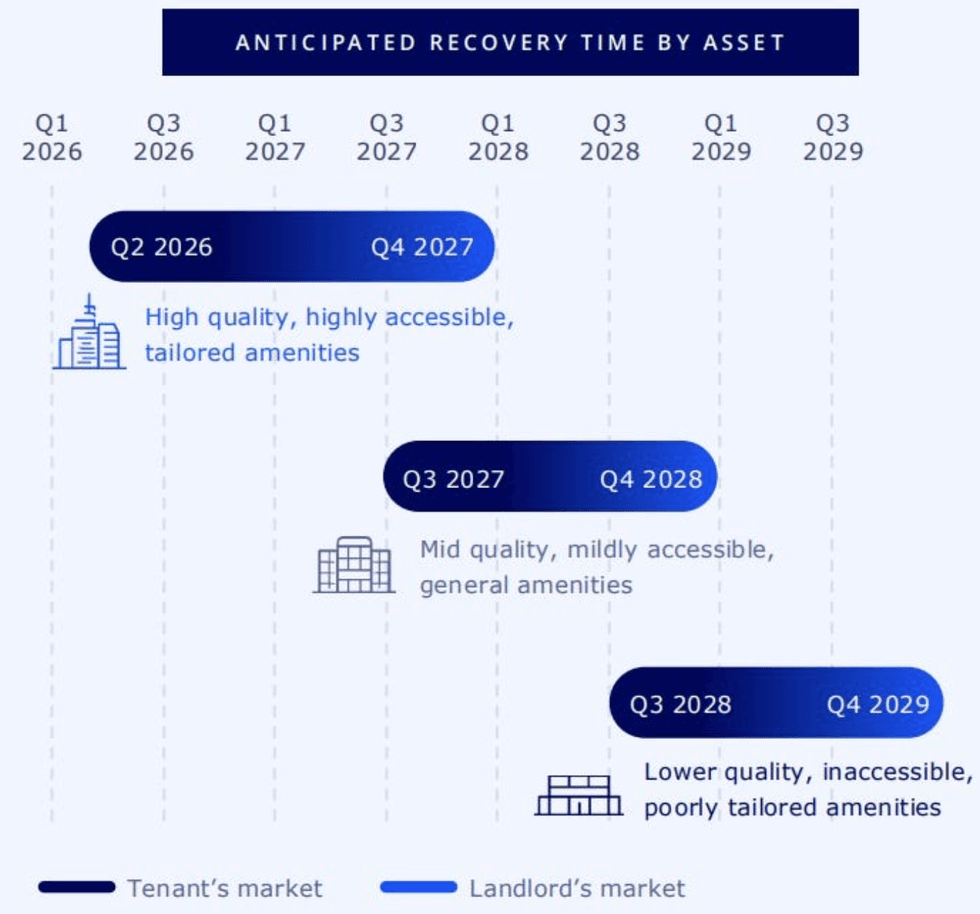

Along with terms like “coronavirus” and “social distancing,” the pandemic also made “flight to quality” a well-known term in the commercial real estate world. As the name suggests, the office market increasingly started to split into two: the top-tier buildings (Class AAA, A) and the rest (Class B and C), with the former still performing well, and the rest being more of a mixed bag.

This is also expected to be the case with the recovery, with Colliers forecasting that the top-tier buildings will return to pre-pandemic vacancy rates as quickly as Q4 2027, mid-market buildings returning to those levels by Q4 2028, and low-tier buildings getting there in Q4 2029.

“The speed of recovery is not uniform across all asset classes,” said Colliers. “Our analysis, based on predictive models incorporating more than 200 leasing variables, shows that demand is already tightening for the most competitive buildings. This includes high quality buildings that are highly accessible and equipped with tailored amenities. All asset classes will experience a gradual shift from a tenant’s market to a landlord’s market, yet it will begin and end at different points.”

(Colliers)

(Colliers)

The “right-sizing” cycle also seems to be nearing (or at) an end. In Q2 2020, 46% of tenants indicated that they needed less space. This number dropped to 37% a few months later, and then held steady at around 25% for four years. However, in Colliers’ most recent survey, just 11% of tenants indicated that they wanted to decrease the size of their space and 17% indicated that they wanted to increase the size of their space.

Another indicator is the median unit size lease-up rate, which was around 4,000 sq. ft in 2020, stayed between 3,300 and 3,500 sq. ft between 2022 and 2024, before rebounding back up to 3,900 sq. ft in 2025. Colliers says companies are moving on from the “wait and see” approach and now have more confidence.

All of this is to say that “the tide is shifting,” as Colliers phrased it, and that the office market’s pandemic era is nearing an end.