Renovation Permits

Learn about renovation permits in Canadian real estate - when they’re required, how they protect homeowners, and what projects need approval.

June 06, 2025

What are Renovation Permits?

Renovation permits are official approvals issued by a municipal government that allow homeowners or contractors to legally perform specific home renovations or alterations.

Why Renovation Permits Matter in Real Estate

In Canadian real estate, permits ensure that renovations meet current building codes, zoning bylaws, and safety standards.

Permits are typically required for:

- Structural changes (e.g., removing load-bearing walls)

- Electrical, plumbing, or HVAC modifications

- Basement finishing or additions

- Decks, fences, and roof work

Failure to obtain proper permits can result in fines, halted construction, difficulty reselling the property, or required removal of unpermitted work.

Understanding renovation permits helps homeowners plan legal, compliant upgrades and avoid costly setbacks during resale or inspections.

Example of Renovation Permits in Action

A homeowner applies for a renovation permit before converting their attic into a bedroom, ensuring compliance with local building codes.

Key Takeaways

- Required for many structural or system changes

- Enforce safety and code compliance

- Issued by local municipalities

- Affects property resale and insurance

- Helps prevent fines and legal issues

Related Terms

- Building Code

- Load-Bearing Wall

- Final Inspection

- Home Inspection

- Permit Compliance

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

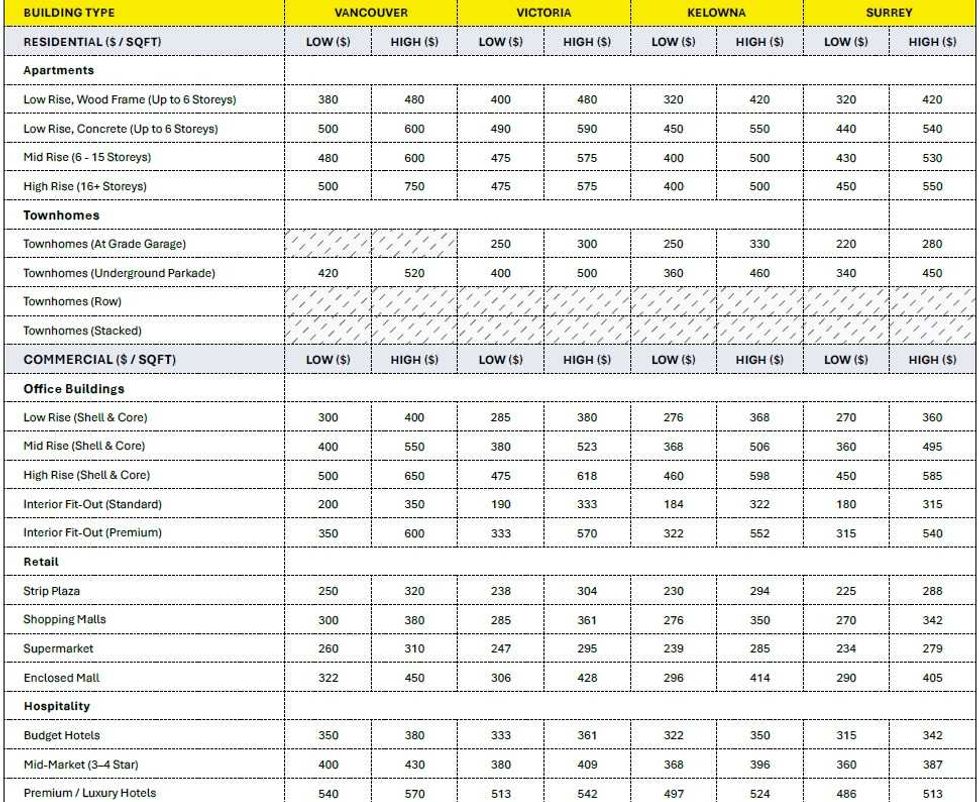

Construction cost ranges for British Columbia. (BTY Group)

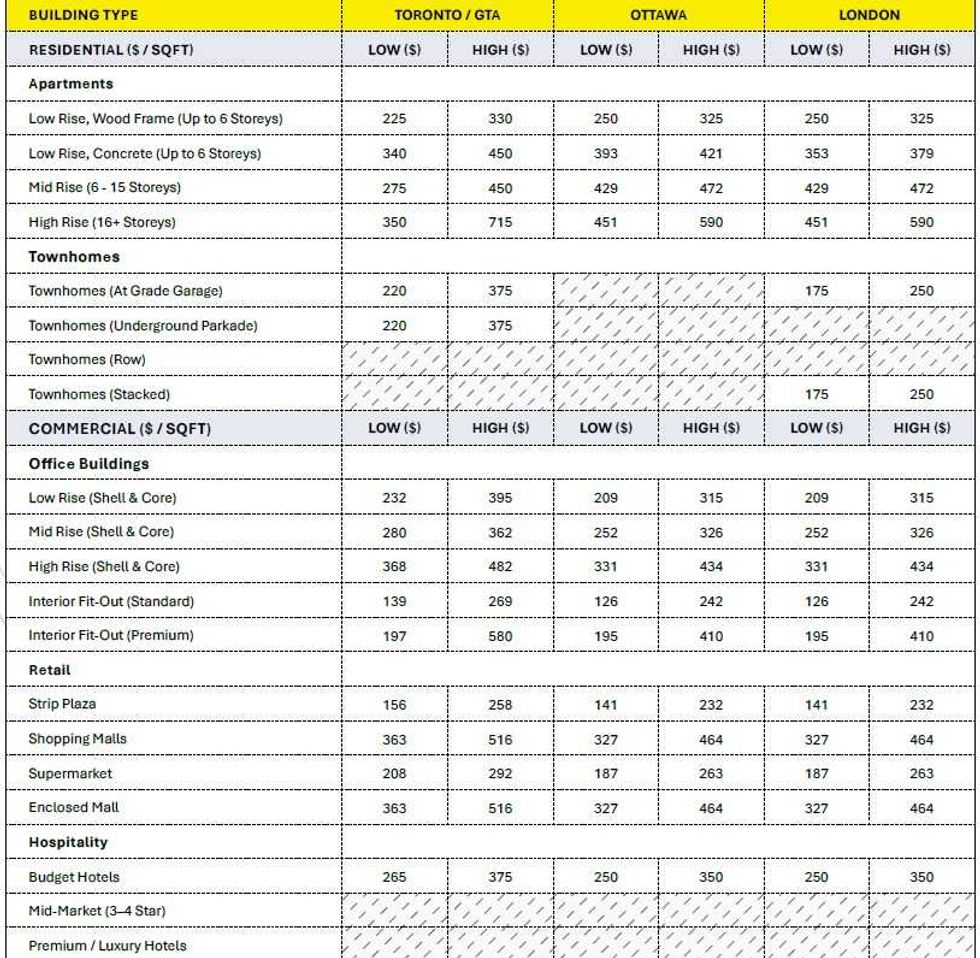

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

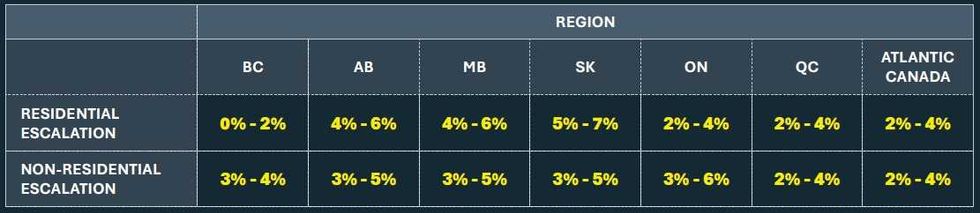

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)

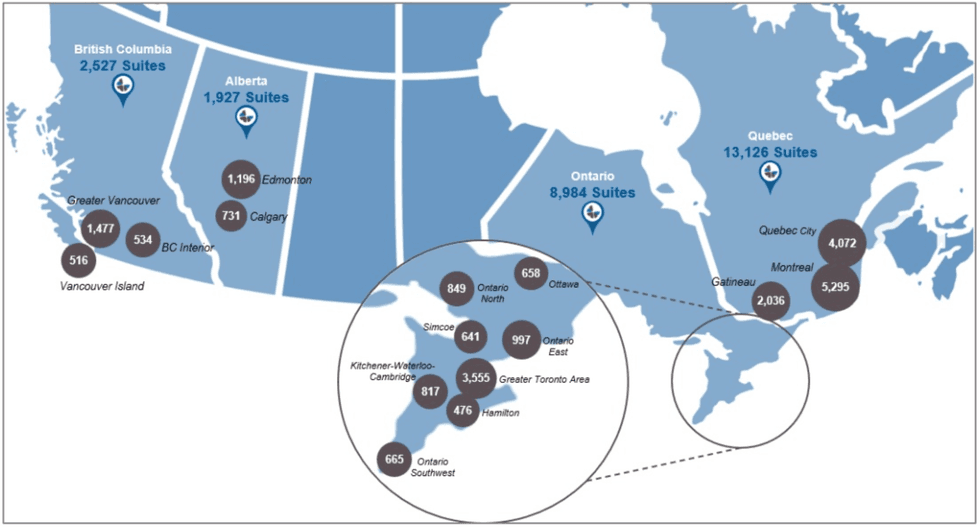

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)