Prime Rate

Learn what the prime rate is in Canadian real estate, how it influences mortgage rates, and what it means for borrowers with variable-rate loans.

May 22, 2025

What is the Prime Rate?

The prime rate is the benchmark interest rate set by major Canadian banks, used as the basis for determining variable interest rates on loans and lines of credit.

Why the Prime Rate Matters in Real Estate

In Canadian real estate, the prime rate directly affects borrowing costs for variable rate mortgages, Home Equity Lines of Credit (HELOCs), and personal loans. It is influenced by the Bank of Canada’s overnight lending rate and typically adjusts several times a year in response to monetary policy.

Key features of the prime rate:- Published by major financial institutions (e.g., RBC, TD)

- Used to price variable loans (e.g., Prime - 0.5%)

- Responds to economic conditions like inflation or growth

Borrowers with variable-rate mortgages or floating-rate HELOCs will see their interest rates fluctuate as the prime rate changes. Conversely, fixed-rate mortgages are not directly tied to the prime rate but may still be influenced by related bond yields.

Understanding the prime rate helps buyers assess interest risk, choose between fixed or variable products, and anticipate changes in monthly payments over time.

Example of the Prime Rate in Action

A borrower with a variable-rate mortgage at Prime - 0.75% sees their rate increase from 4.70% to 5.20% after the prime rate rises by 0.5%.

Key Takeaways

- Base rate for variable loans in Canada.

- Adjusted by banks based on Bank of Canada policy.

- Affects mortgages, HELOCs, and credit lines.

- Impacts affordability and payment amounts.

- Important for borrowers with variable products.

Related Terms

- Variable Rate Mortgage

- Bank of Canada Rate

- HELOC

- Interest Rate

- Mortgage Term

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

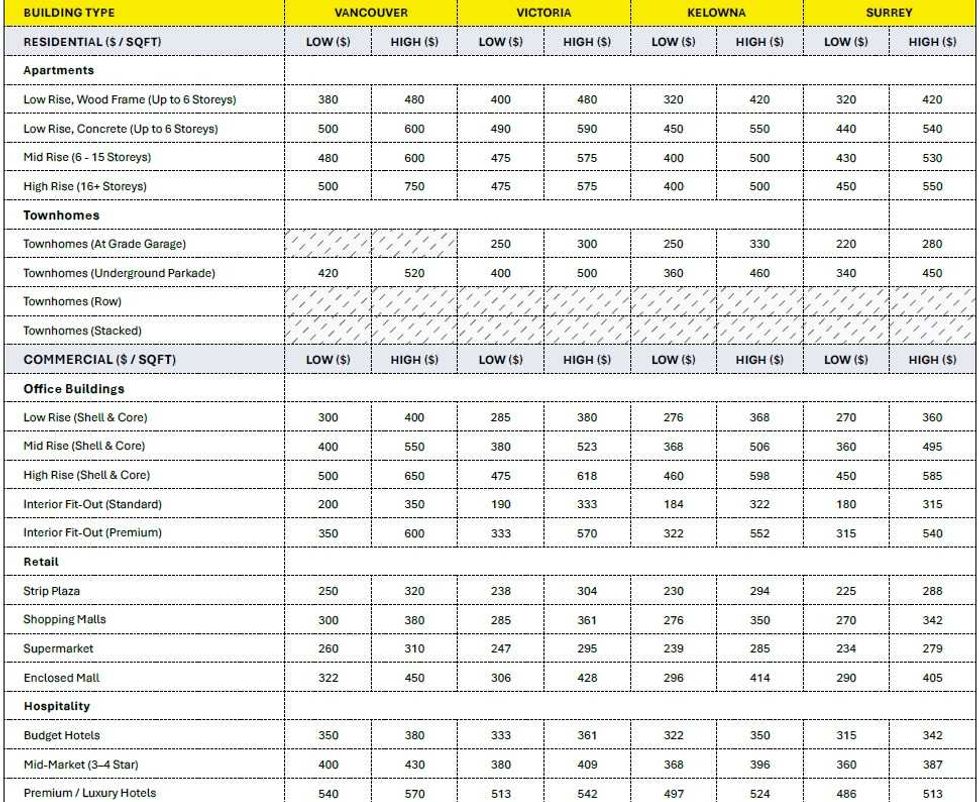

Construction cost ranges for British Columbia. (BTY Group)

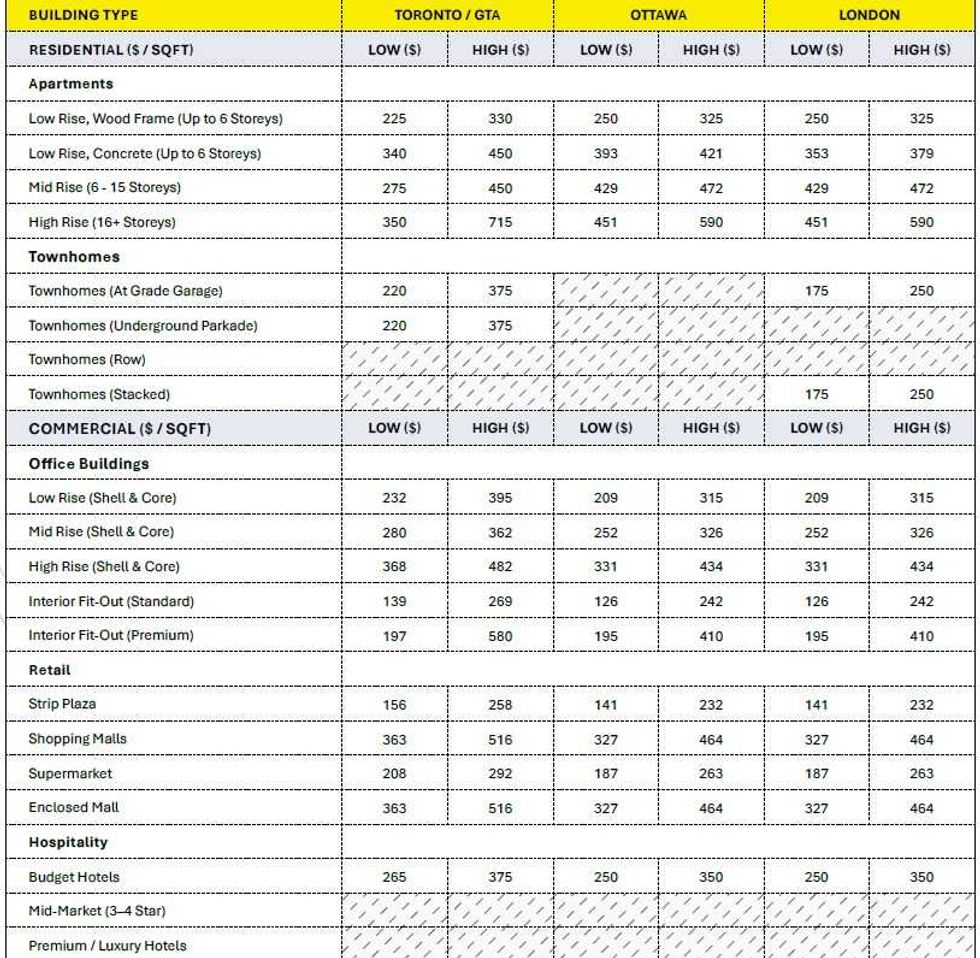

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

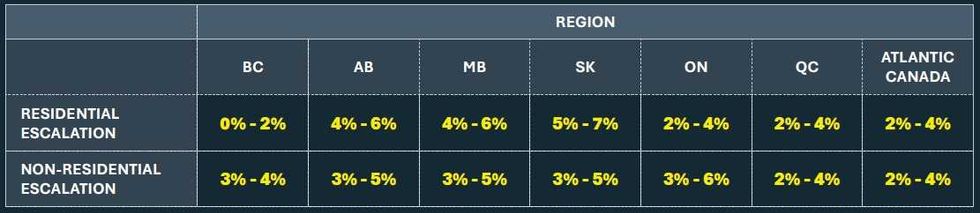

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)

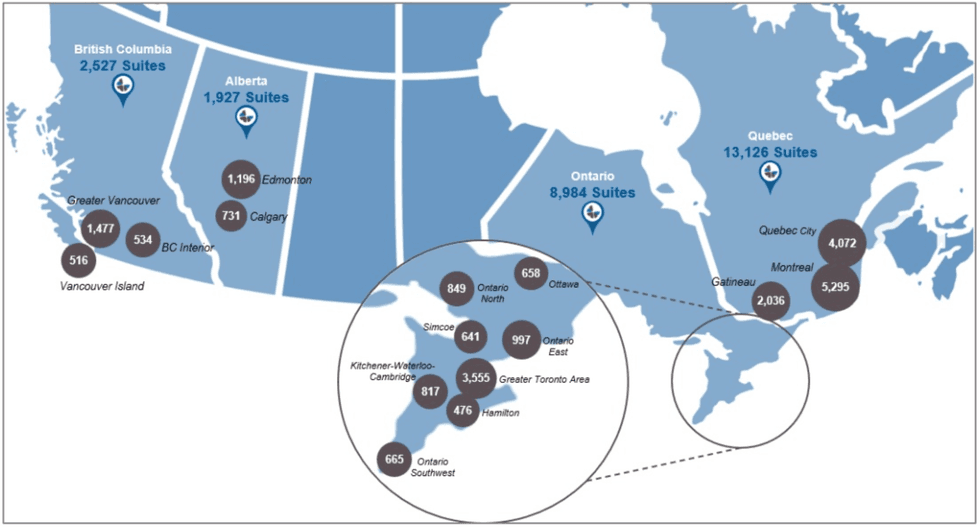

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)