Depreciation

Explore how depreciation works in Canadian real estate, how it affects insurance, investment taxes, and how it’s calculated for assets and property value.

May 22, 2025

What is Depreciation?

Depreciation is the reduction in the value of a property or asset over time due to wear and tear, aging, or market conditions.

Why Depreciation Matters in Real Estate

In Canadian real estate, depreciation plays an important role in property valuation, insurance claims, investment accounting, and taxation.

Depreciation affects:

- Actual Cash Value (ACV) of insurance claims

- Capital cost allowance for rental properties

- Resale value and maintenance planning

For investment properties, the Canada Revenue Agency (CRA) allows owners to claim depreciation (called capital cost allowance) as a tax deduction, although it may affect capital gains tax on sale.

Understanding depreciation helps owners plan maintenance, assess insurance claims, and track asset value over time.

Example of Depreciation in Action

An older furnace is worth less today than when it was installed. Depreciation is deducted from its value in an insurance claim after a fire.

Key Takeaways

- Reflects wear and aging over time.

- Lowers insurance payouts under ACV.

- Impacts taxes for investment properties.

- Important for asset and claim evaluations.

- Can affect resale value.

Related Terms

- Actual Cash Value

- Capital Cost Allowance

- Replacement Cost

- Home Insurance

- Property Value

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

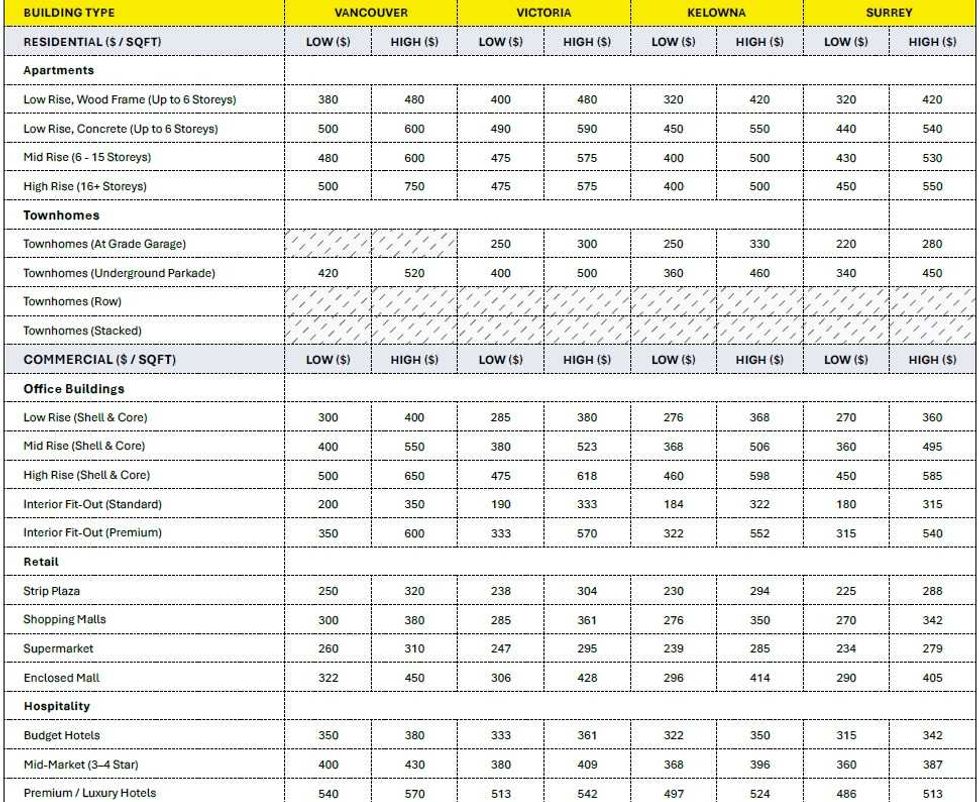

Construction cost ranges for British Columbia. (BTY Group)

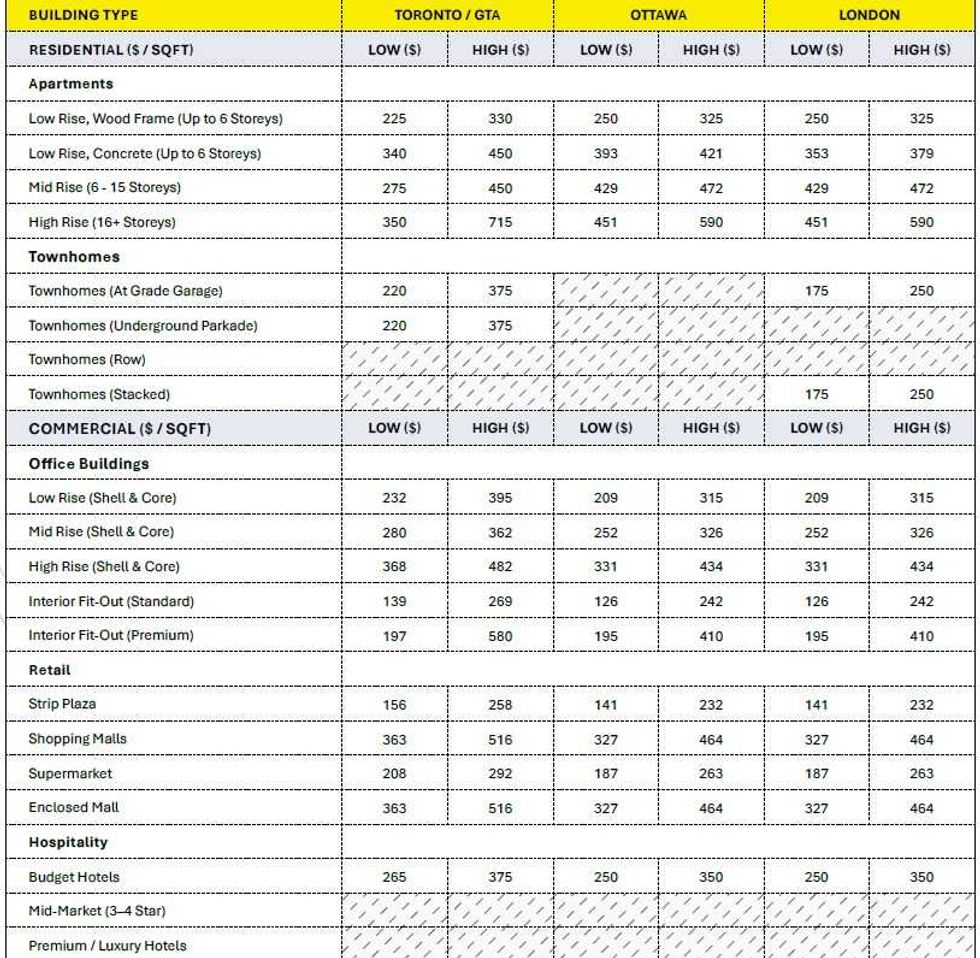

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

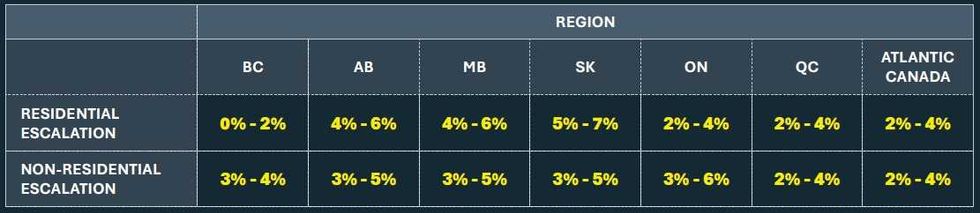

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)