Following a frenzied spring, back to back interest rate hikes have taken the momentum out of Canada’s housing market rebound. But, despite a forecast of falling prices, affordability is not expected to improve.

Home sales dipped 0.7% month-over-month in July, putting an end to six months of heightened activity. The decline occurred despite a 5.6% monthly increase in new listings, which helped bring balance back to the market.

Although the MLS Home Price Index (HPI) climbed 1.1% from June to July, the pace of appreciation has slowed from the 1.9% average seen over the last three months, a trend economists expect to persist for the foreseeable future.

In a new housing market update from RBC, Robert Hogue, Assistant Chief Economist, and Rachel Battaglia, Economist, predict that price gains will "continue moderating in the months ahead," as balanced demand-supply conditions reduce upward pressure, and high interest rates trim buyers’ budgets.

"The path ahead for Canada’s market is likely to be bumpy," Hogue and Battaglia said.

"We expect higher interest rates to keep curbing buyers’ enthusiasm for months to come, while possibly forcing the hand of some current owners to sell."

The expectation of stagnating prices, and continuously high interest rates, was shared by Robert Kavcic, Senior Economist and Director of Economics at BMO, in a recent economic publication. With interest rates remaining high, so too will mortgage rates.

The July Consumer Price Index (CPI) keeps the decision for future rate hikes "very much alive," Kavcic said, and at the very least, it makes the case for interest rates to stay elevated into 2024. As such, any meaningful near-term mortgage rate relief "looks unlikely."

As Farah Omran, Senior Economist at Scotiabank noted in a housing market update, the number of sales seen in July was aligned with the 2000-2019 average for the month, which indicates a "more sustainable level of housing activity." However, this "does not mean all is well with Canada’s housing market."

"Affordability remains out of reach for many first-time home buyers and supply continues to lag," Omran said, adding that July’s price increase reflects "fundamental imbalances in market conditions."

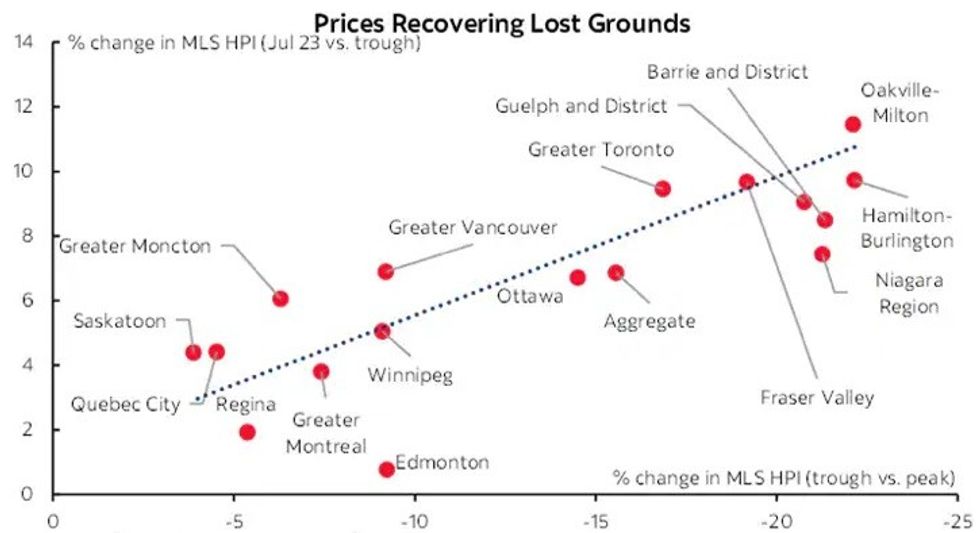

The cities that saw the greatest price correction over the latter half of 2022 have also seen the largest price increases thus far in 2023, leading to a reversal in any improvements in affordability.

After the Bank of Canada started raising interest rates in early 2022, prices declined approximately 22% in Oakville-Milton, but have since recovered more than 11%. The Fraser Valley experienced a roughly 20% drop following the start of rate hikes; since hitting bottom, they've risen about 9%. Meanwhile, in Montreal, home priced declined 7% during the correction, and have recovered less than 4%.

Scotiabank Economics

Scotiabank Economics

"We need a more proactive approach from all levels of government towards achieving more sustainable market conditions with concrete implications for prices and affordability rather than continue to be stuck in this pattern of what comes up must come down," Omran said.

"But the floor is a trampoline mounted too high for many Canadians to be able to reach and catch the jumping prices."