Mortgage Arrears

Understand mortgage arrears in Canadian real estate, what they are, what causes them, and how borrowers can avoid or resolve them before legal action begins.

May 22, 2025

What are Mortgage Arrears?

Mortgage arrears occur when a borrower falls behind on scheduled mortgage payments, typically by more than 30 days.

Why Mortgage Arrears Matter in Real Estate

In Canadian real estate, falling into mortgage arrears signals a risk of default. Lenders closely monitor arrears and may begin legal proceedings if payments are not brought up to date within a set timeframe.

Consequences of arrears include:- Credit score damage

- Collection calls and late fees

- Initiation of power of sale or foreclosure

Borrowers in arrears may qualify for hardship programs, payment deferrals, or refinancing to catch up. Provincial laws govern how lenders must notify and respond to arrears, often requiring notice before legal action.

Understanding mortgage arrears helps homeowners take early action to avoid losing their home or facing long-term financial harm.

Example of Mortgage Arrears in Action

A borrower who misses three consecutive payments enters mortgage arrears and receives a lender notice warning of possible legal action.

Key Takeaways

- Indicates missed mortgage payments.

- Leads to penalties and lender notices.

- Can trigger legal recovery processes.

- Impacts credit and ownership rights.

- Can be resolved through proactive steps.

Related Terms

- Default

- Foreclosure

- Power of Sale

- Refinance

- Credit Score

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

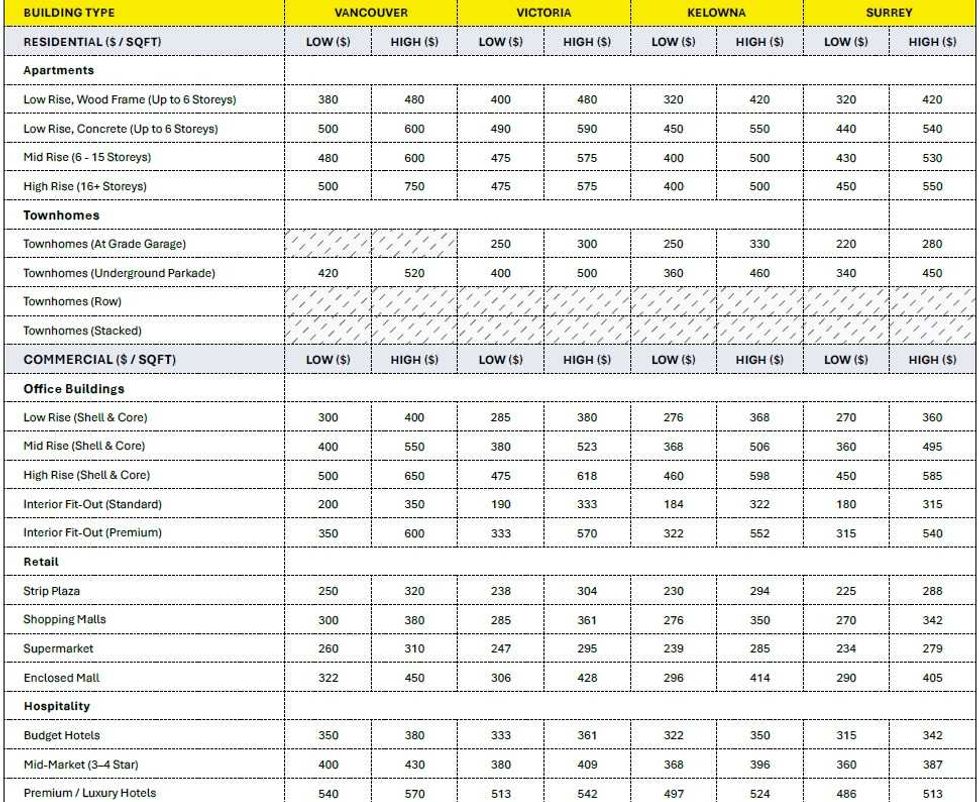

Construction cost ranges for British Columbia. (BTY Group)

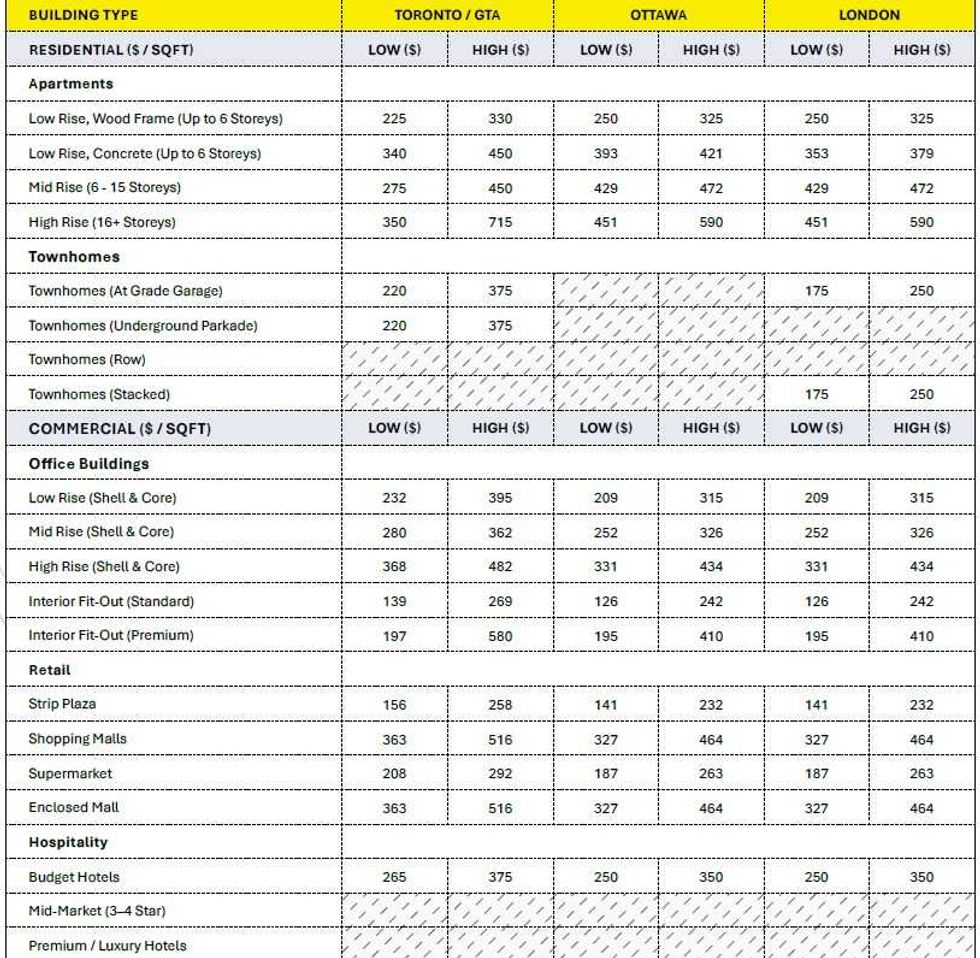

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

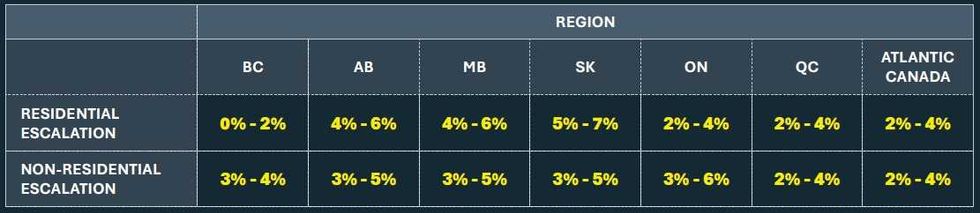

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)