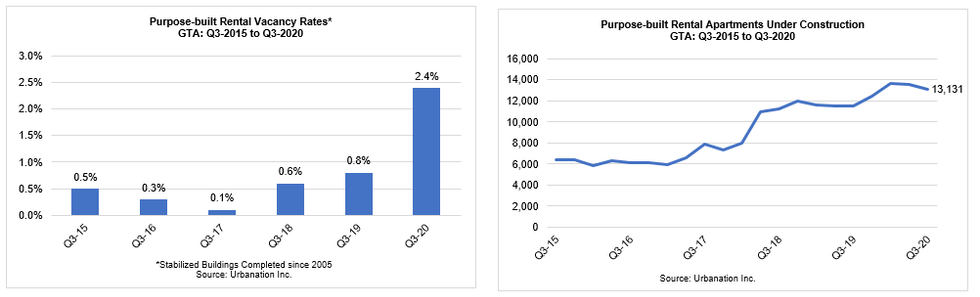

Vacancy rates for purpose-built rentals in Toronto have reached a 10-year low, rising over 2% in Q3-2020, while the Greater Toronto Area (GTA) saw rental rates reach 2.4% -- or three times higher (0.8%) -- than the same time last year, according to Urbanation's latest rental market results.

According to Urbanation, within the former City of Toronto -- which mainly represents the downtown and midtown markets -- vacancy rates increased to 2.8% from 0.7% a year ago, during Q3-2020.

Despite the initial COVID-19 restrictions, which halted construction, purpose-built rental development remained elevated in the third quarter compared to previous years, with 13,131 units under construction -- down from the recent high of 13,663 units in Q1-2020. However, this is still up from a year ago (11,522 units) and more than double the level from four years ago (6,117 units).

What's more, a total of 5,276 new rental units are scheduled for completion in the GTA in 2021 -- the highest level in more than 25 years and up from 988 units completed in 2020.

READ: Toronto Rental Market Expected to Hit Price Floor “Soon”: Report

The Urbanation data also revealed that average monthly rents for units that became available for rent in the GTA during the third quarter (within buildings that have been completed for at least one year) declined by 5.8% year-over-year to $2,373.

While rents were down in some pockets, Urbanation says average rents did increase 1.1% quarter-over-quarter in both the outer 416 and 905 regions, while continuing to fall in the former City of Toronto with an accelerated quarterly decline of 5.0%.

Within the former City of Toronto, the steepest year-over-year declines in average per square foot rents were found in the East Bloor/The Village submarket near U of T and Ryerson University (-16.8%), the Downtown Core (16.0%), the Entertainment District (-15.9%), and CityPlace (-14.3%).

The report also suggests that the rent price decline could stem from a decrease in the average available unit size, which reached a record low 740-square-feet from 767-square-feet a year earlier, indicating that turnover has been relatively stronger for smaller units.

On a per square foot basis, Urbanation says rents declined by 2.4% year-over-year to $3.21-per-square-foot. Within the former City of Toronto, monthly rents declined 9.3% year-over-year to $2,549 with average available unit sizes down from 716-square-feet in Q3-2019 to a low of 676-square-feet in Q3-2020.

On a per square foot basis, rents in former Toronto were also down 3.8% year-over-year to $3.77-per-square-foot.

This data coincides with a new report from Padmapper, which suggests that after months of price declines, the “rent free fall” in Toronto might come to an end — and soon — as Canada’s priciest rental markets are expected to hit a price “floor.”

What's more, Rentals.ca’s and Bullpen Research & Consulting’s latest rental data also showed that month-over-month, average rent in September for a one-bedroom was down 2.2% and down 3.3% for a two-bedroom, while year-over-year, average monthly rent for a one-bedroom was down 14.9% and down 12% for a two-bedroom.

“Toronto is seeing the biggest decline in rental and condo apartment rental rates on average among major municipalities in Canada; this is driven by the rapid decline in downtown condo rents, with many recently completed buildings seeing rates drop by 10% to 15% annually,” noted Ben Myers, president of Bullpen Research & Consulting.

Additionally, what's interesting to note is that Urbanation found that the reported decline in rents was additional to incentives. Most rental buildings surveyed were offering incentives to attract new tenants, which mainly included one month of free rent, move-in bonuses and, to a lesser extent, two months of free rent.

Shaun Hildebrand, President of Urbanation, says while the GTA rental market showed some improvement in the third quarter within more suburban areas, there were weakened conditions in the downtown areas as "renters reevaluated the costs of living in the central core as most offices, post-secondary schools, and entertainment venues remained closed."

"While it was encouraging to see the large increase in lease activity in third quarter as renters took advantage of recent discounts, the market will continue to face challenges heading into 2021 from restrained demand caused by COVID-19 and elevated supply levels,” added Hildebrand.

You can read the full report here.