Stress Test

Explore Canada’s mortgage stress test — how it works, what it means for your approval, and how it helps ensure sustainable homeownership.

May 22, 2025

What is the Stress Test?

A mortgage stress test is a regulatory requirement that ensures borrowers can afford mortgage payments even if interest rates rise in the future.

Why the Stress Test Matters in Real Estate

In Canada, all federally regulated lenders must apply a stress test to mortgage applicants, whether they are buying, refinancing, or switching lenders.

Borrowers must qualify at the greater of:

- The contracted mortgage rate + 2%

- The Bank of Canada’s benchmark qualifying rate

The stress test reduces the maximum loan amount a borrower can qualify for. It’s designed to protect both borrowers and the financial system from overleveraging during rate increases.

Understanding the stress test helps buyers calculate realistic budgets and avoid surprises during mortgage approval.

Example of the Stress Test in Action

A borrower applies for a 4.6% mortgage but must qualify at 6.6% under the stress test, reducing their purchasing power by $50,000.

Key Takeaways

- Required for all mortgage applications.

- Tests ability to handle higher rates.

- Lowers maximum approved mortgage.

- Protects borrowers from financial strain.

- Set by federal regulators and lenders.

Related Terms

- Mortgage Qualification

- Debt Service Ratios

- Interest Rate

- Mortgage Pre-Approval

- Lender Guidelines

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

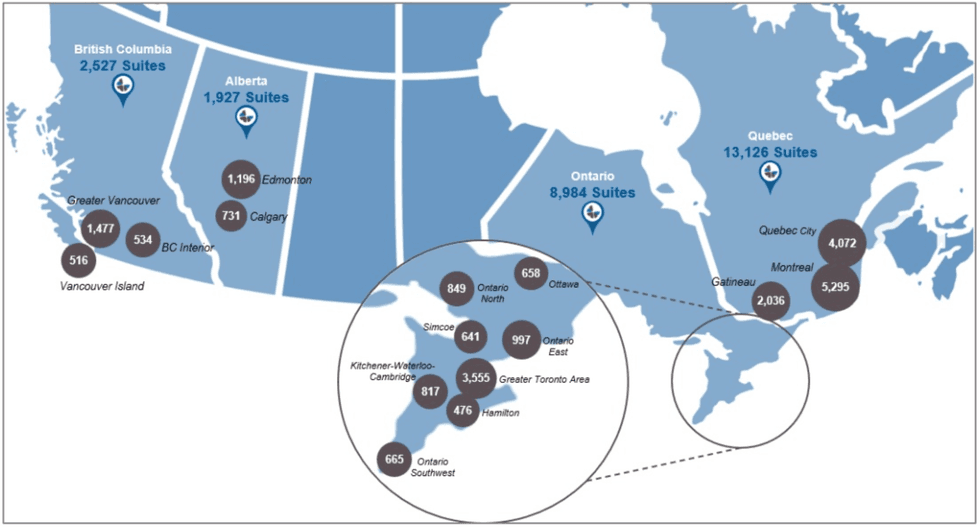

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

150 Slater Street in Ottawa. (Regional Group)

150 Slater Street in Ottawa. (Regional Group) 150 Slater Street in Ottawa. (Regional Group)

150 Slater Street in Ottawa. (Regional Group)

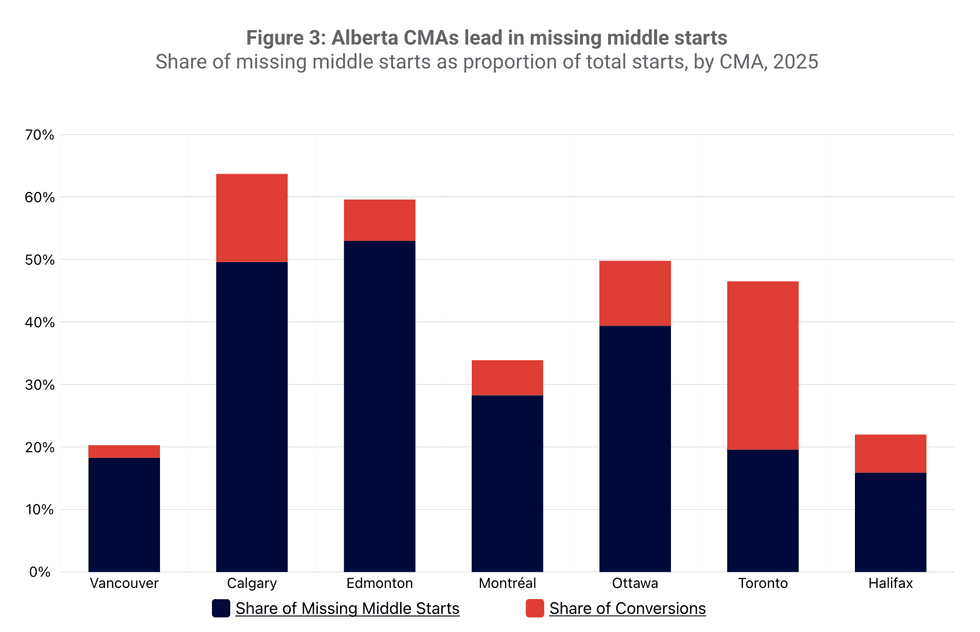

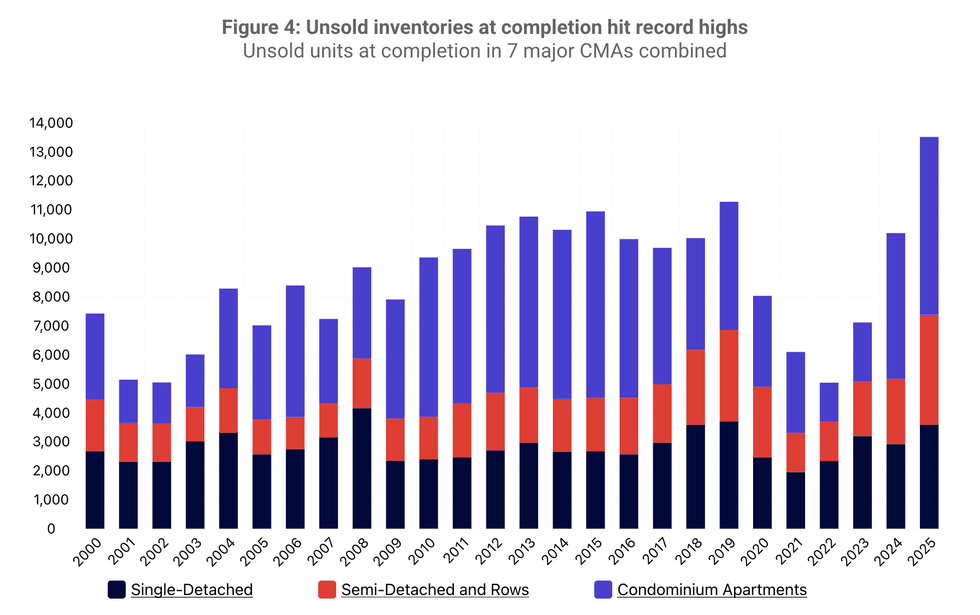

Spring 2026 Housing Supply Report/CMHC

Spring 2026 Housing Supply Report/CMHC Spring 2026 Housing Supply Report/CMHC

Spring 2026 Housing Supply Report/CMHC

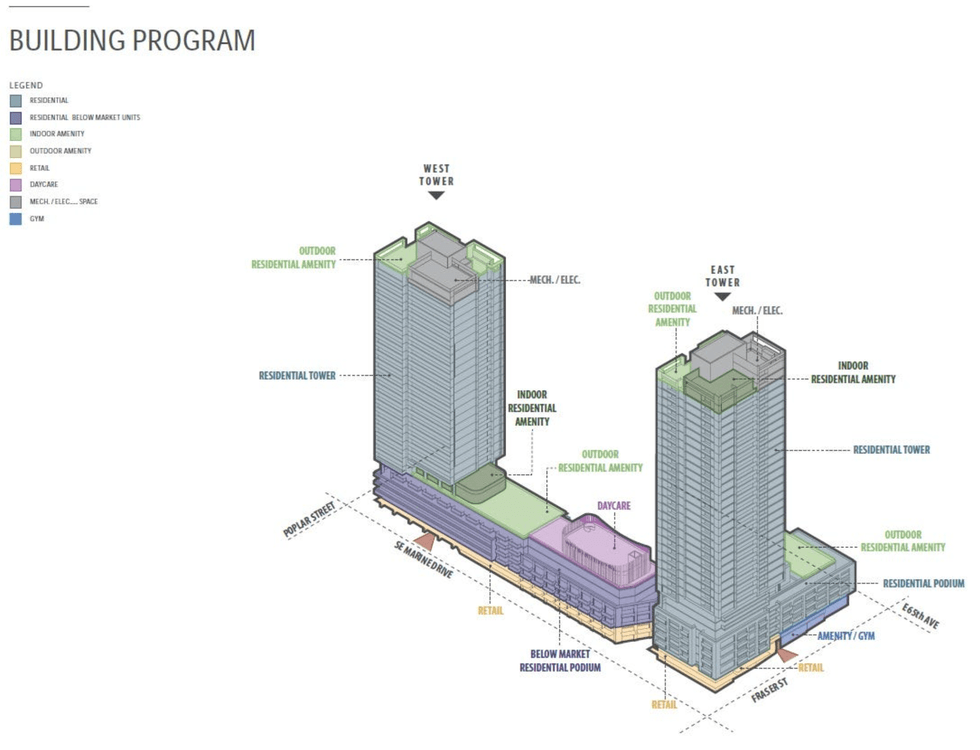

The Marine Terrace apartments at 605 SE Marine Drive. (MCMP Architects, Peterson)

The Marine Terrace apartments at 605 SE Marine Drive. (MCMP Architects, Peterson) An overview of the 605 SE Marine Drive proposal and uses. (MCMP Architects, Peterson)

An overview of the 605 SE Marine Drive proposal and uses. (MCMP Architects, Peterson) A rendering of the 605 SE Marine Drive proposal from the corner of SE Marine Drive and Fraser Street. (MCMP Architects, Peterson)

A rendering of the 605 SE Marine Drive proposal from the corner of SE Marine Drive and Fraser Street. (MCMP Architects, Peterson)

Renderings of the proposal for 605 SE Marine Drive in Vancouver. (MCMP Architects, Peterson)

Renderings of the proposal for 605 SE Marine Drive in Vancouver. (MCMP Architects, Peterson)