Now that the second wave of COVID-19 is well underway, the pandemic's overall impacts on Canadian mortgages is becoming more apparent.

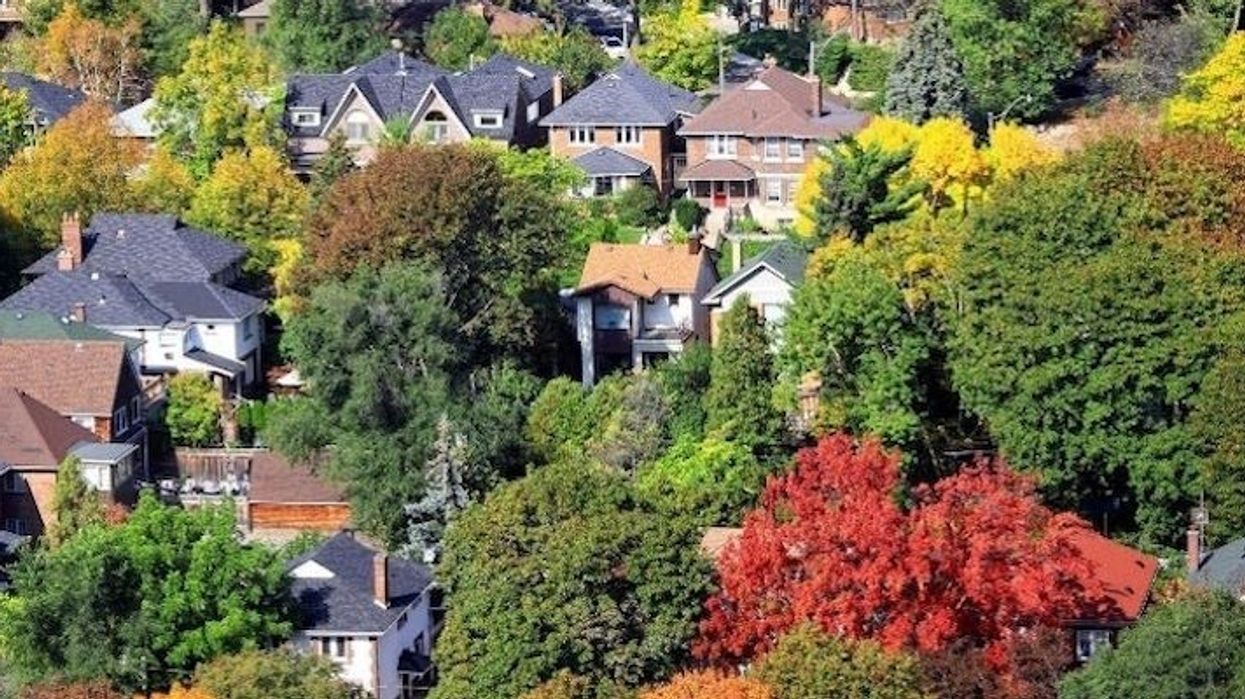

In the pre-pandemic era, million-dollar mortgages in Toronto were relatively rare. But since the pandemic arrived, brokers are reporting an increasing number of mortgages in the $1-3 million dollar range, according to the latest mortgage trends report from LowestRates.ca.

“A combination of CERB, record-low mortgage rates, and remote work are pushing the housing market to new heights,” says Justin Thouin, founder and CEO of LowestRates.ca. “People aren’t spending on commutes, or going out. The savings rate is currently at a level we haven’t seen since the 1960s. And many people are funnelling those savings into housing.”

The Bank of Canada’s decision to buy mortgage-backed bonds also contributed, driving down mortgage interest rates and keeping demand for mortgages high.

READ: Average Toronto Home Prices Forecast to Rise Another 6% in 2021

Shawn Stillman, principal broker at Mortgage Outlet, told LowestRates he’s now seeing larger mortgages in the GTA than he did before the pandemic. "Up until this year, mortgages of $1 million or more have been rare," said Stillman.

In the 10 years Stillman has been a mortgage broker, he told LowestRates he’s done about 20 of them. This year, however, he’s regularly seeing mortgages in the $1- to $3-million range.

“People are still looking around and have a lot of inquiries since rates have gone down,” says Stillman. “The mortgage market is definitely fluid right now and it’s healthy. It’s not quite a buyers market, and not quite a seller's market.”

The increase in mortgages is being attributed to more people "moving up the economic ladder" as more workers are experiencing decreased costs due to working remotely and subsequently, taking advantage of the lower mortgage rates.

What's more, property values have also increased in the Toronto-area, meaning that people have more equity in their homes.

“The government has done a very good job of protecting property values,” says Stillman. This is due to the federal government's CERB program which protected people's cash flow and through the Bank of Canada’s decision to buy mortgage-backed bonds, which Stillman says drove down mortgage interest rates and kept demand for mortgages high.

“The combination of those two things was very powerful,” said Stillman.

The report also noted that the end of mortgage deferrals might not trigger a drop in national home prices, as previously predicted.

The mortgage payment deferral period, which lenders implemented at the beginning of lockdown, has officially ended. The last chance for those to request deferrals was at the end of August, which allowed people to defer payments until the end of December.

Throughout the pandemic, experts warned that once mortgage deferrals came to an end, the country could face a mortgage "deferral cliff", with CMHC president and CEO, Evan Siddall, warning that one-fifth of all outstanding mortgages could potentially be at risk of going into default.

However, Leah Zlatkin, principal broker at Brite Mortgage, says that there won't be a cliff, rather "more of a little ditch."

"A few people might fall into it, but I don't think it's going to be a big deal," said Zlatkin.

What's more, even if homeowners can’t afford to pay for their mortgage once the deferral period ends, Zlatkin doubts a significant amount of those deferrals will turn into defaults right away. Foreclosure, she says, is a lengthy and complex process.

“It's going to be a slow-rolling process because this kind of thing doesn't happen overnight,” says Zlatkin. “There's a lot of extenuating circumstances. Every single home is different and every single lender is different, too. Just because one lender does it a certain way doesn't mean every lender does it that way.”