Community Land Trust (CLT)

A community land trust is a non-profit that owns land to keep housing affordable permanently through resale restrictions.

September 29, 2025

What is a Community Land Trust?

A community land trust (CLT) is a non-profit organization that owns land to preserve long-term housing affordability. Homes are sold or rented at below-market rates while the trust retains ownership of the underlying land.

Why a Community Land Trusts Matter in Real Estate

CLTs matter in real estate because they protect against displacement, stabilize neighborhoods, and ensure permanent affordability. They give communities control over land use and housing outcomes.

Example of a Community Land Trust in Action

A non-profit community land trust in Vancouver acquires land and sells homes at affordable prices, ensuring resale restrictions keep them affordable for future buyers.

Key Takeaways

- Non-profit ownership of land to ensure affordability.

- Homes sold or rented below market rates.

- Prevents displacement and supports community stability.

- Ensures permanent affordability with resale restrictions.

- Empowers communities to guide housing outcomes.

Related Terms

- Affordable Housing Agreement

- Inclusionary Housing Policy

- Non-Profit Housing

- Housing Affordability

- Land Lease Community

The Marine Terrace apartments at 605 SE Marine Drive. (MCMP Architects, Peterson)

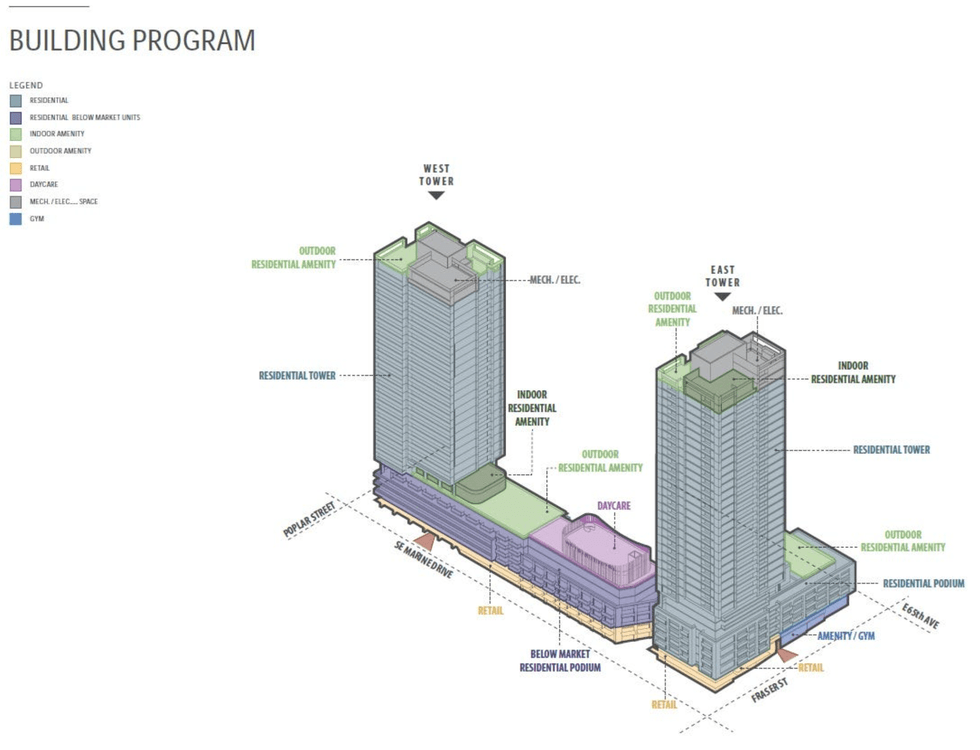

The Marine Terrace apartments at 605 SE Marine Drive. (MCMP Architects, Peterson) An overview of the 605 SE Marine Drive proposal and uses. (MCMP Architects, Peterson)

An overview of the 605 SE Marine Drive proposal and uses. (MCMP Architects, Peterson) A rendering of the 605 SE Marine Drive proposal from the corner of SE Marine Drive and Fraser Street. (MCMP Architects, Peterson)

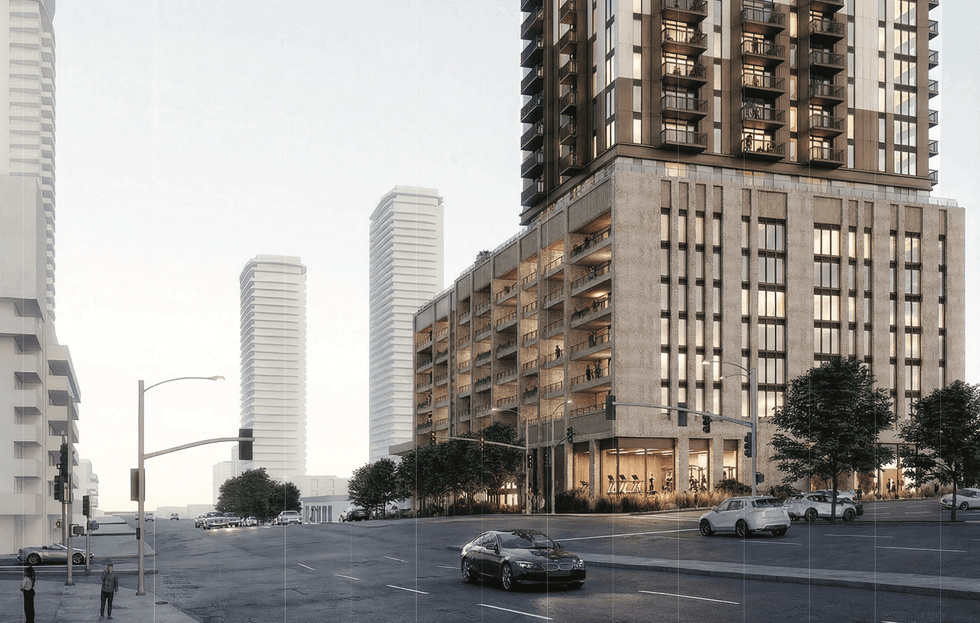

A rendering of the 605 SE Marine Drive proposal from the corner of SE Marine Drive and Fraser Street. (MCMP Architects, Peterson)

Renderings of the proposal for 605 SE Marine Drive in Vancouver. (MCMP Architects, Peterson)

Renderings of the proposal for 605 SE Marine Drive in Vancouver. (MCMP Architects, Peterson)

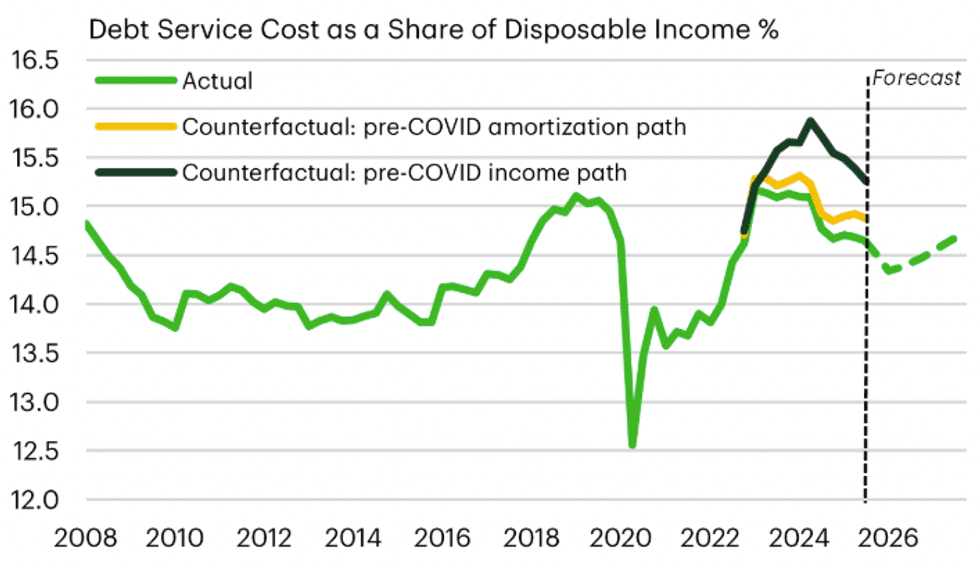

Income growth and longer amortizations are blunting mortgage shock/Statistics Canada, TD Economics

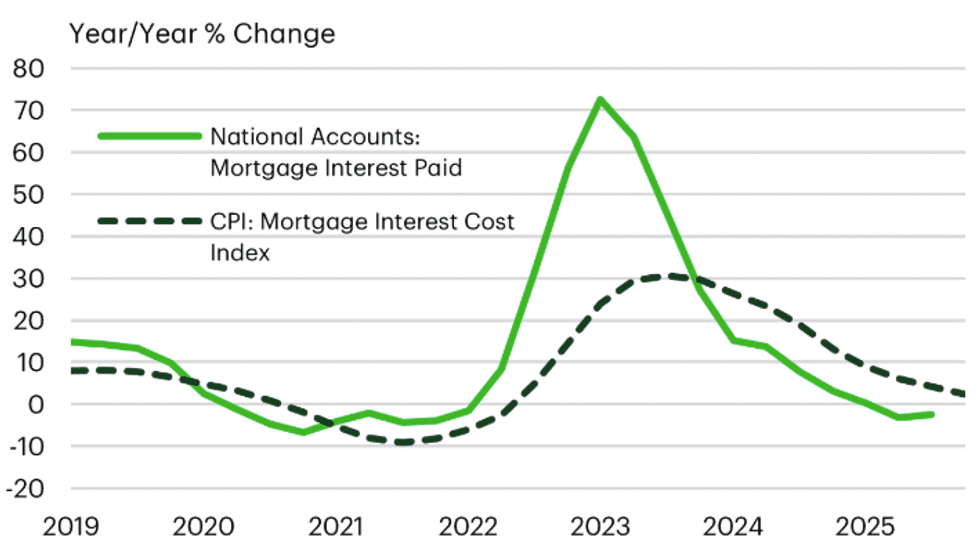

Income growth and longer amortizations are blunting mortgage shock/Statistics Canada, TD Economics Canada's mortgage interest cost index is nearing deflation/Statistics Canada, TD Economics

Canada's mortgage interest cost index is nearing deflation/Statistics Canada, TD Economics Canada's mortgage stock is more rate-sensitive today/Bank of Canada, TD Economics

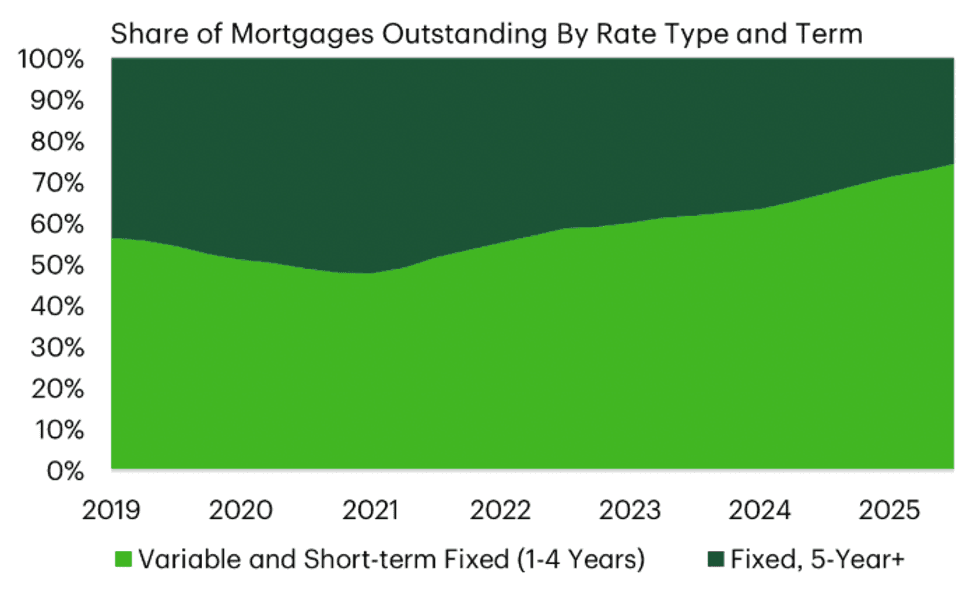

Canada's mortgage stock is more rate-sensitive today/Bank of Canada, TD Economics

Manuela Preis/Instagram

Manuela Preis/Instagram