Pre-Approval Vs. Pre-Qualification

Compare mortgage pre-approval vs. pre-qualification in Canada to understand which gives buyers stronger offers and more reliable borrowing estimates.

May 22, 2025

What is Pre-Approval and Pre-Qualification?

Pre-approval and pre-qualification are two stages of the mortgage process that assess a buyer’s ability to borrow, but differ in their depth and reliability.

Why do Pre-Approval and Pre-Qualification Matter in Real Estate

Pre-qualification is an informal estimate of how much a buyer might be able to borrow based on self-reported information. It does not involve credit checks or document verification.

Pre-approval, on the other hand, is a formal process in which a lender:

- Reviews credit history

- Verifies income and debts

- Provides a conditional commitment for a mortgage amount

In competitive markets, pre-approval strengthens a buyer’s offer and shows sellers that financing is secure.

Key differences:- Pre-qualification = quick estimate

- Pre-approval = documented, lender-reviewed approval

Buyers should seek pre-approval before shopping seriously, as it provides clarity on budget and helps avoid disappointment. Sellers are also more likely to accept offers backed by pre-approval letters.

Understanding the distinction empowers buyers to navigate the financing process more effectively and make stronger offers.

Example of Pre-Approval and Pre-Qualification in Action

A buyer receives a pre-approval letter for $700,000 from their bank, allowing them to confidently bid on homes in that range.

Key Takeaways

- Pre-qualification = estimate, no verification.

- Pre-approval = verified by lender.

- Pre-approval offers stronger buying power.

- Essential for serious home shopping.

- Boosts credibility in competitive markets.

Related Terms

- Mortgage Pre-Approval

- Mortgage Qualification

- Credit Score

- Debt Service Ratios

- Conditional Offer

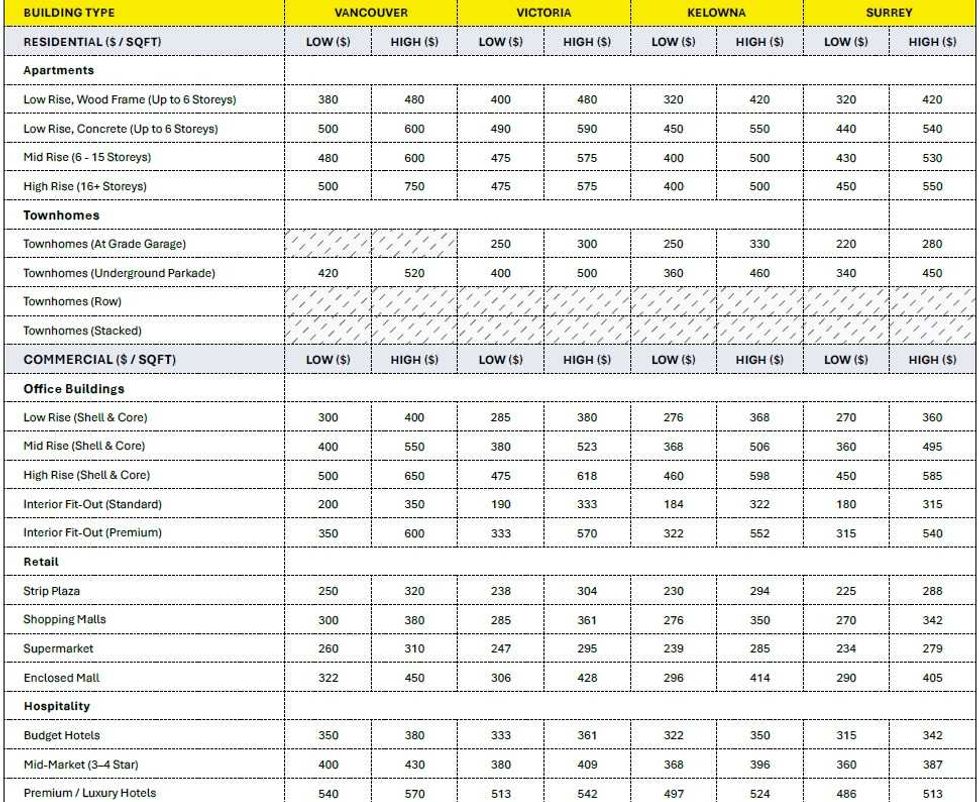

Construction cost ranges for British Columbia. (BTY Group)

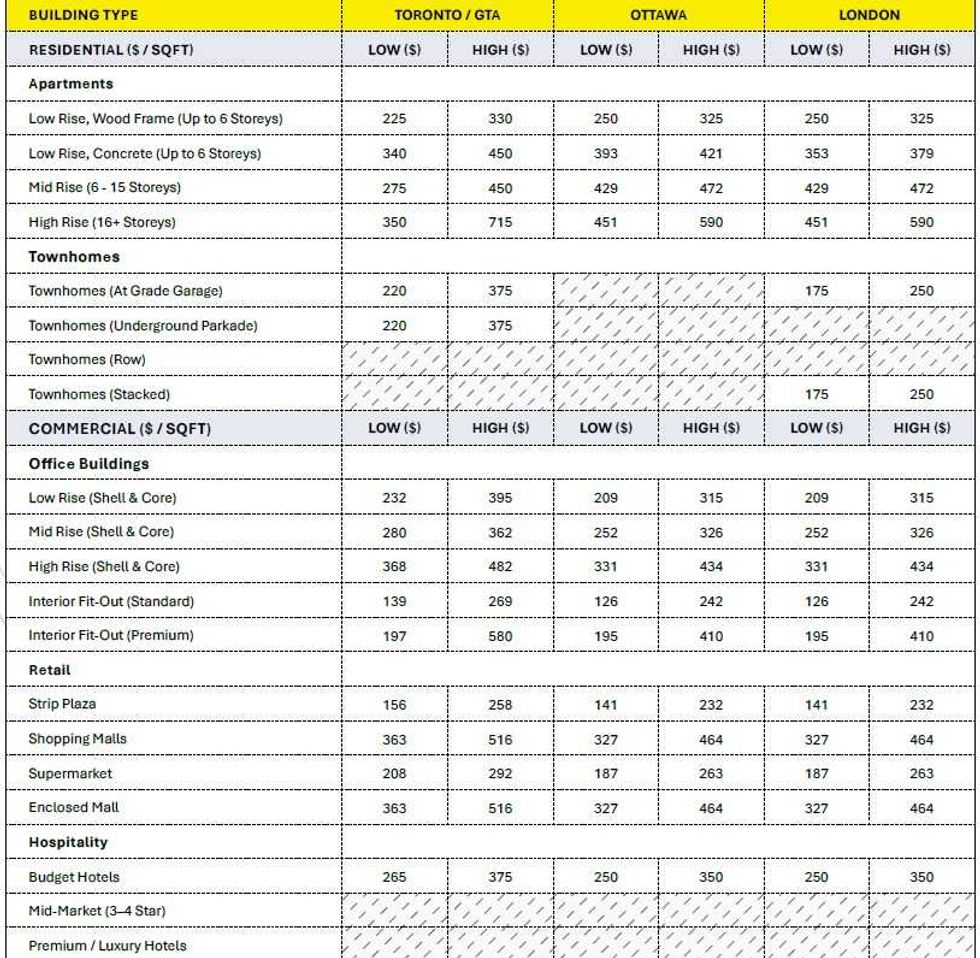

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

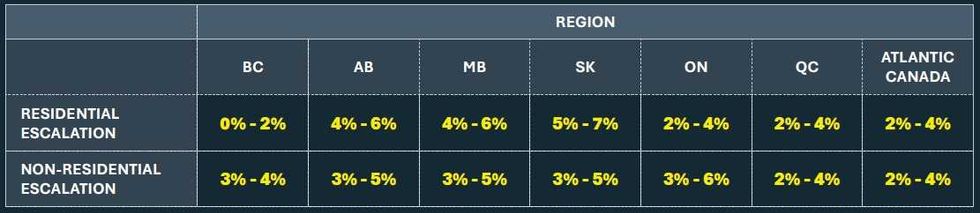

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)

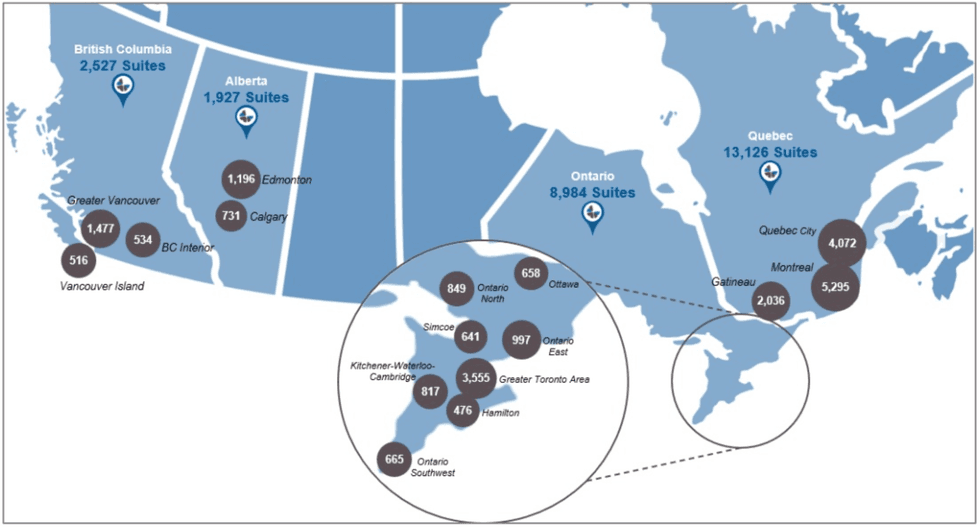

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

The Marine Terrace apartments at 605 SE Marine Drive. (MCMP Architects, Peterson)

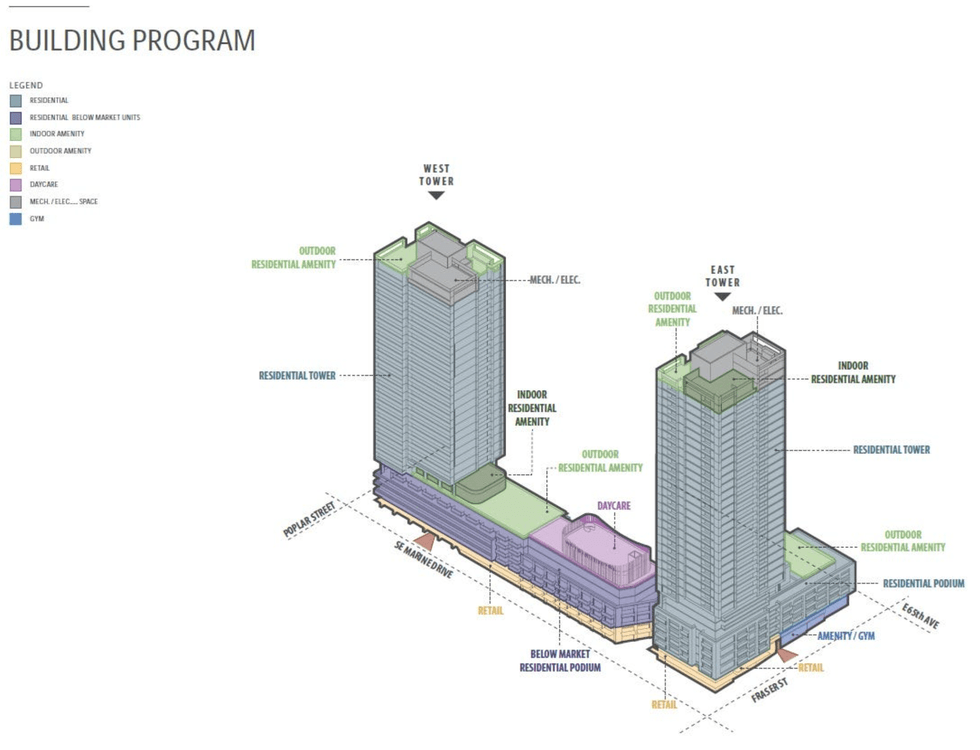

The Marine Terrace apartments at 605 SE Marine Drive. (MCMP Architects, Peterson) An overview of the 605 SE Marine Drive proposal and uses. (MCMP Architects, Peterson)

An overview of the 605 SE Marine Drive proposal and uses. (MCMP Architects, Peterson) A rendering of the 605 SE Marine Drive proposal from the corner of SE Marine Drive and Fraser Street. (MCMP Architects, Peterson)

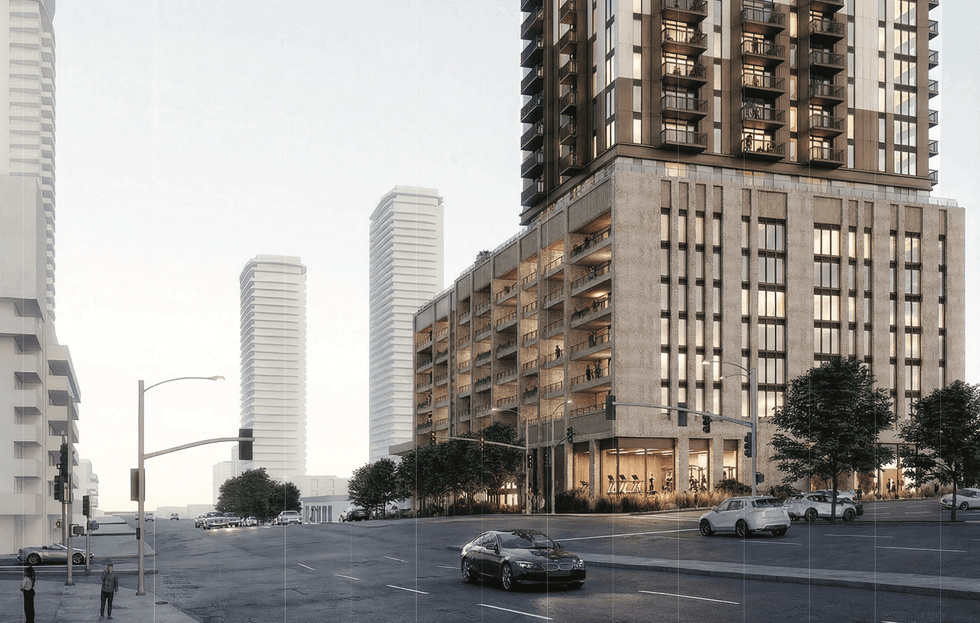

A rendering of the 605 SE Marine Drive proposal from the corner of SE Marine Drive and Fraser Street. (MCMP Architects, Peterson)

Renderings of the proposal for 605 SE Marine Drive in Vancouver. (MCMP Architects, Peterson)

Renderings of the proposal for 605 SE Marine Drive in Vancouver. (MCMP Architects, Peterson)

Manuela Preis/Instagram

Manuela Preis/Instagram