‘Newsmaker of the Year’ is part of STOREYS' annual editorial year-end series. You can find the rest of our 2024 selections here as they're released throughout the week.

It's an unfortunate part of the business, but amidst tough economic conditions over the past few years, some developers have been hit hard and we saw a surge in real estate insolvencies across the country this year.

Many of the biggest cases first came to light last year, including Stateview Homes, Mizrahi Development's The One, and Vandyk Properties in Ontario.

When a Receiver takes over a property, their work during the initial period typically entails painting a complete picture of the situation — identifying exactly how much debt there is and figuring out the state of the property, among other things. It's important work that serves as the foundation for the future of the insolvent entity and the property, but oftentimes the more arduous work doesn't begin until later on — launching the sales process, dealing with complications in the sales process that inevitably come up, and ensuring creditors are made whole.

Through that lens, this was a year when Receivers really had their work cut out for them, with many of last year's big cases progressing to those latter stages in addition to a wave of new cases. (For the purposes of this article, we're lumping Receivers in receiverships, Monitors in CCAA creditor protection cases, and brokers that take over properties in foreclosures and powers of sales all together.)

Alvarez & Marsal has had its work cut out for them with The One, in what is undoubtedly one of the most complex insolvency cases of the last few years, with mini battles between various parties arising at every turn. In the past 12 months, Alvarez & Marsal has replaced the general contractor on the project, launched the sales process, and found a new developer to complete the project, all while handling an insolvent entity that has been challenging to deal with, such as a claim from Mizrahi over payment. These days, they're also dealing with a looming lawsuit by a neighbour that could potentially force construction to pause, which would complicate the case even further.

Mike Czestochowski, Vice Chairman at CBRE

Mike Czestochowski, Vice Chairman at CBRE

KSV Advisory has perhaps been the most active of the various restructuring firms, serving as the court-appointed Receiver in both the Stateview Homes and Vandyk Properties cases (which both include cases-within-cases), as well as two other Mizrahi projects, and now three projects by Thind Properties in Metro Vancouver. (We could go on.)

There's been no shortage of insolvencies, so other firms have also had plenty of work. This year, Ernst & Young has been engaged in the receiverships of the King Square Shopping Centre in Ontario and the planned Garibaldi At Squamish ski resort in British Columbia, Deloitte has been engaged in the receivership proceedings of 1045 Haro Street in Vancouver and the recently-initiated CCAA proceedings of Burnaby Lake Village in Burnaby, and MNP, TDB Advisory, and BDO Canada have also had their fair share of cases across the country.

"2008 and 2009 was very minor compared to what we're going through today," said Mike Czestochowski, Vice Chairman at CBRE and Founder of CBRE's Land Services Group, which has handled numerous court-ordered sales. "The last time I've seen this [level of distress] was in the early 90s, and there's a big difference. In the early 90s, a lot of it was power of sale — usually one mortgage, very clean, lawyer deals with it, hires us, and we sell it to recoup the mortgage. The majority of stuff we're seeing today is court-appointed Receivers — usually we see that when there is more than one mortgage, other lien holders, maybe sales in place, construction commenced in some way, and it's more messy."

Similar to what has been observed in BC, Czestochowski says being overleveraged and lacking experience are the top two commonalities among the developers that have faced insolvency. This includes groups that may have been focused on single-family homes jump into high-rise projects without truly understanding the complexities.

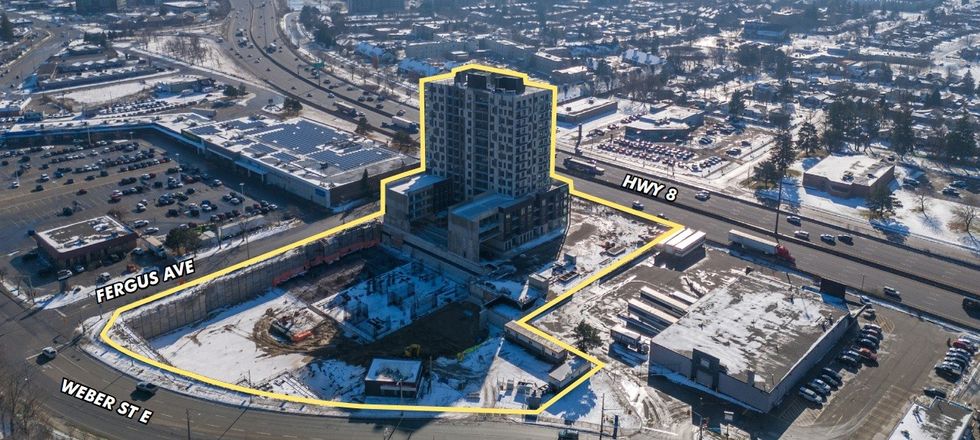

The Elevate project at 1333 Weber Street East site in Kitchener that was sold via receivership this year. / CBRE

The Elevate project at 1333 Weber Street East site in Kitchener that was sold via receivership this year. / CBRE

One byproduct of the volume of cases is that it has pushed insolvency law forward. Although the tool has been used before in the past from time to time, this year saw the use of reverse vesting orders (RVOs) truly emerge, after the Court of Appeal in British Columbia issued what some believe to be a precedent-setting ruling recognizing the legitimacy of RVOs — a tool that allows the shares of a company to be purchased instead of just the asset, bypassing property transfer taxes and maximizing creditor recovery. Since then, BC has seen several instances of insolvency sales with approved traditional vesting orders be restructured to make use of reverse vesting orders, and the tool is now also being explored in Ontario, says Czestochowski.

Another trend that has been observed is the adage of "extend and pretend," where lenders enter into forbearance agreements with borrowers in hopes that market conditions will improve and the borrowers will then be able to fulfill their financial obligations. Because of this, the amount of distressed sales that have occurred this year may actually just be the tip of the iceberg, say PricewaterhouseCoopers and the Urban Land Institute in the Canadian portion of their 2025 US Emerging Trends report.

"Some industry watchers said they saw fewer receiverships and distressed sales in early 2024 than expected," the report noted. "One possible reason is that many lenders are trying to avoid realizing substantial losses on their loans and aren't rushing to force indebted condo developers to liquidate assets in a depressed market. Instead, they're entering into forbearance agreements and exercising their right to place credit bids, giving developers opportunities to negotiate new terms."

"Unfortunately those forbearance agreements, a majority of the time, don't seem to work, because maybe there's something inherently wrong with the property, or just too much debt, and the sales have fallen off so dramatically for a lot of these projects," said Czestochowski. "So, depending on the project, sometimes the forbearance agreement can fix things, but in many cases time doesn't fix it because we're at the will of the market."

The insolvencies do not only impact those directly under distress, but also loom over the market at large. A big theme across the industry this year has been price discovery and the gap between asking prices and bids, and the distress permeating the market also clouds the ability to properly value properties, which carries a swath of potential downstream impacts.

"Some argue that an increase in foreclosures could add pressure to appraised property values, further tightening lending conditions," PwC and ULI found, adding that "these forces are exposing a widening market bifurcation" between larger, well-capitalized developers and smaller developers when it comes to access to credit, as STOREYS has previously reported. That can push the smaller developers toward non-bank lenders, who typically offer credit at much higher interest rates, leaving little room for error.

"The level of activity on distressed properties is increasing, not decreasing," said Czestochowski. "One trend that I see, which probably changed starting six months ago, is the properties are bigger. Before, stuff was smaller and under $25 million. Now, stuff is over $50 million and, for the first time, we're starting to see large income-producing properties — apartment buildings, plazas, industrial buildings — that we weren't seeing before. I think you can count on receiverships for 2025 being quite active."

In other words, the value of a tried and trusted Receiver could be greater now than ever – and this may also be just the beginning of their work.