Editor's Note: The headline of this article has been edited from a previous version that indicated that there are three times as many insured mortgages than uninsured.

It’s no secret that the landscape of mortgage lending in Canada has shifted amid higher interest rates, but a just-released study from Statistics Canada shows that things started to take a turn years before the Bank of Canada began to dial up the heat on rates. The culprit: home prices.

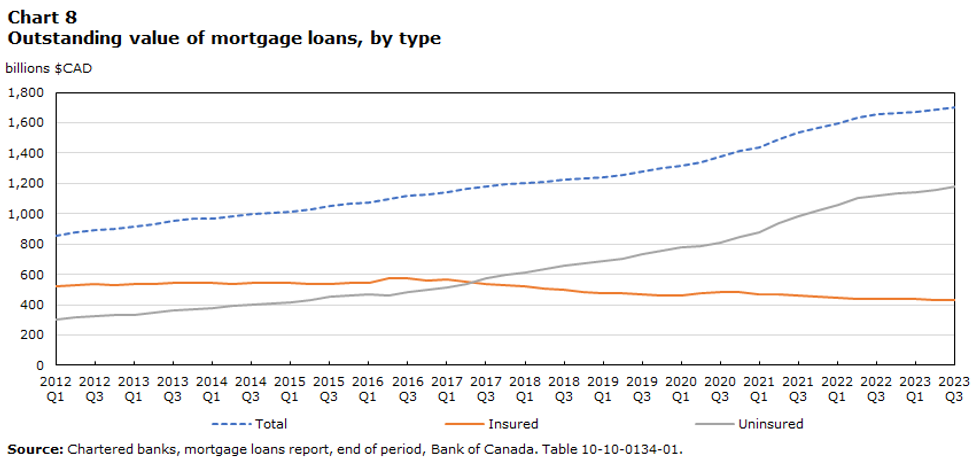

StatCan reported on Wednesday that “uninsured mortgages have predominated in Canada” since 2017, “overtaking insured ones for the first time that year.”

“From 2012 to 2019, the outstanding value of uninsured mortgages grew by an average quarterly rate of 3.0%, compared with a decline of 0.4% for insured mortgages,” the government agency said. “This disparity widened during the pandemic as house prices soared, driven by lower borrowing costs and pent-up demand, accelerating the quarterly growth rate of uninsured mortgages to 3.4% from 2020 to 2022, while that of insured mortgages fell slightly to a decline of 0.5%.”

In terms of dollar amounts, the data shows that, in the fourth quarter of 2020 — the thick of the pandemic — the outstanding value of uninsured mortgages, at $846B, was about double that of insured mortgages, at $481B. Fast forward to the third quarter of 2023, the most recent quarter included in StatCan’s study, and the value of uninsured mortgages surged to $1,178B, while the value of insured mortgages dropped down to $431B.

And this is all notwithstanding the fact that housing market activity began to cool off in early 2022 through the third quarter of 2023, which resulted in less of a discrepancy between insured and uninsured mortgage values.

It would be misleading to say that the trajectory of these figures stems from high house prices alone, however. As stated in Wednesday’s study, Canadians are facing “regulatory constraints” that render homes valued over $1,000,000 ineligible for insurance.

These days especially, that criteria is extremely restrictive, and can leave buyers with no other choice than to go the uninsured route. This is particularly true when it comes to single-detached homes, which tend to come at a higher price-point, and of buyers in Canada’s largest markets for residential real estate: Toronto and Vancouver. The study points out that the average price for a single-family detached home was $1.5M in the Toronto area and $2M in the Vancouver area in the third quarter of 2023.

StatCan said that, according to the latest data available, “the share of newly originated uninsured mortgages was 87% in Toronto and 90% in Vancouver.” Although house prices are lower in markets like Calgary and Montreal, the shares of newly originated uninsured mortgages still account for a roaring majority, at 64% and 68%, respectively.