We’re closing in on almost a year since the Hudson’s Bay Company (HBC) filed for creditor protection. Liquidating the company’s assets and closing all of its stores was the easy part — and has mostly been completed already. The hard part is determining what to do with the huge blocks of vacant space left in the company’s wake.

Across Canada, HBC operated a total of 96 stores, including not just the traditional Hudson’s Bay stores, but also a handful of stores under the Saks Fifth Avenue and Saks OFF 5TH brands.

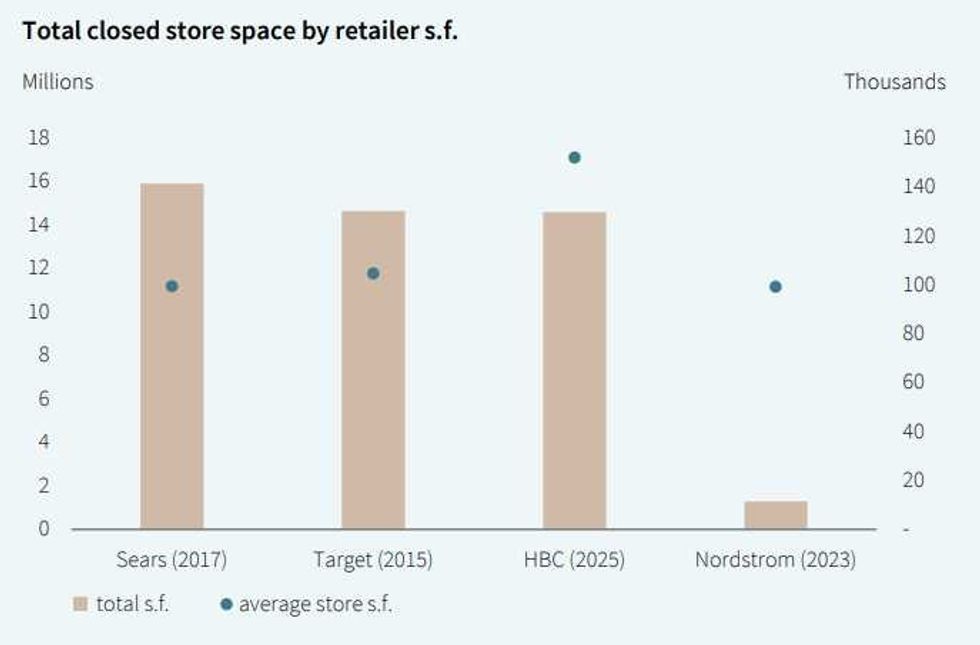

According to a recent report published by commercial real estate services firm JLL, the amount of space HBC vacated totals to approximately 15 million sq. ft; approximately the same amount of space vacated by Target in 2015, and just slightly less than the amount vacated by Sears in 2017 — although HBC had a larger average store size than both of those retailers.

JLL is now forecasting that tenants will be found for 65% of that 15 million sq. ft within the next two years — 31% within one year, and 34% within two years — while the remaining 35% may take longer than two years to fill.

“High interest from retailers, brokerage activity, and retail-leasing-market fundamentals indicate a manageable path for addressing HBC vacancies, maintaining retail use in most locations,” said JLL. “The prime, transit-oriented nature of many HBC locations remains their greatest asset, attracting serious interest from a new generation of expanding tenants. Their long-term performance as retail destinations provides a foundation of proven market viability.”

Hudson’s Bay vacated about as much space as Target did in 2015. (JLL)

Hudson’s Bay vacated about as much space as Target did in 2015. (JLL)

Geographically, about 41% of the 15 million sq. ft is located in Ontario, with 19% in British Columbia, 17% in Quebec, 16% in Alberta, 3% in Manitoba, and 2% in Saskatchewan. A commonality among all of HBC’s former spaces, which adds a new layer to the challenge, is that they are all extremely large.

“The size mismatch becomes clear when comparing tenant requirements with available space,” said JLL. “The average shopping centre lease in Canada sits at roughly 3,700 square feet, while HBC boxes average 152,000 square feet — roughly 40 average-sized retailers. Many of the locations are multi-storey complicating and adding costs to the process of remerchandising the boxes. This size differential requires creative leasing approaches and potentially substantial capital expenditures that impact net operating income.”

With Canada being home to increasingly fewer department stores and tenants that could take on spaces this large, many landlords — such as Primaris REIT — have plans to reconfigure the spaces, whether that be subdividing them into smaller boxes or demolishing them to make way for new construction.

JLL projects that just 14% of the 15 million sq. ft of vacant HBC space will be re-allocated to a single tenant, while 22% is planned for redevelopment and 64% is set to be subdivided into smaller mid-size boxes between 15,000 sq. ft and 40,000 sq. ft, which allow for the possibility of flagship fashion stores, furniture stores, sporting goods stores, and even dining concepts or entertainment venues.

“With a list of prospects that includes current tenants and tenants adjacent to the property, leasing teams are working to identify a tenant mix that complements their overall property offering,” JLL added. “This process involves investigating associated costs and evaluating how different tenants will enhance the property’s appeal. In many cases, landlords have already secured a major anchor tenant and need to fill the remaining space with complementary smaller businesses that drive performance.”

There was a time when mall redevelopments were the new hot development trend, but because of the market downturn and continued headwinds, HBC’s landlords — most of which are Canada’s largest REITs and pension funds — are being forced to pivot toward “less capital-intensive, income-generating retail strategies,” according to JLL.

Only time will tell what’s in store for all 15 million of those formerly-HBC sq. ft, but what’s certain today is that it’s officially — and undeniably — the end of an iconic era.