Financing Condition

Learn what a financing condition is in Canadian real estate, how it protects buyers, and why it’s important when making offers on property.

May 22, 2025

What is a Financing Condition?

A financing condition is a clause in a real estate purchase agreement that makes the offer contingent on the buyer securing mortgage approval within a set timeframe.

Why Financing Conditions Matter in Real Estate

In Canadian real estate, the financing condition protects buyers by giving them time—usually 3 to 5 business days—to obtain a mortgage commitment without risking their deposit.If financing is not secured:

- The buyer can back out with no penalty

- The deposit is refunded in full

Understanding the financing condition ensures buyers make informed decisions about risk tolerance, offer strength, and financial readiness.

Example of Financing Condition

A buyer includes a five-day financing condition in their offer, allowing time to receive final approval before committing to the purchase.

Key Takeaways

- Gives buyers time to secure financing.

- Allows withdrawal without penalty.

- Standard in most residential deals.

- Waiving increases risk.

- Part of offer negotiation strategy.

Related Terms

- Conditional Offer

- Firm Offer

- Mortgage Pre-Approval

- Buyer Risk

- Deposit

Sutton Group CEO Ross McCredie (left) and Douglas Elliman CEO Michael S. Liebowitz (right).

Sutton Group CEO Ross McCredie (left) and Douglas Elliman CEO Michael S. Liebowitz (right).

(OREA)

(OREA) (OREA)

(OREA)

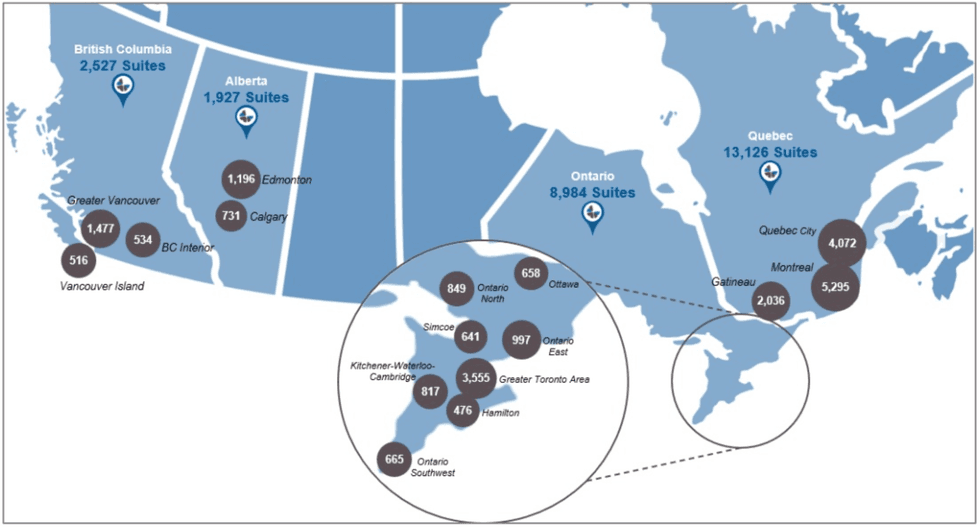

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)

Chartwell’s portfolio as of December 31, 2025. (Chartwell Retirement Residences)