Newly-released stress testing from the Canada Mortgage and Housing Corporation (CMHC) presents that, in a worst-case scenario, the country could see a drop in housing prices of nearly 50% by 2030.

The CMHC stress testing is based on its own capital and liquidity levels and is, of course, impacted by the affects of the ongoing COVID-19 pandemic.

"[The stress testing] shows that the impact of a range of pandemic scenarios is mitigated through actions taken by the government and CMHC management," reads the testing's write-up.

READ: RE/MAX Claims CMHC is ‘Fear-Mongering’ in Housing Market Forecast

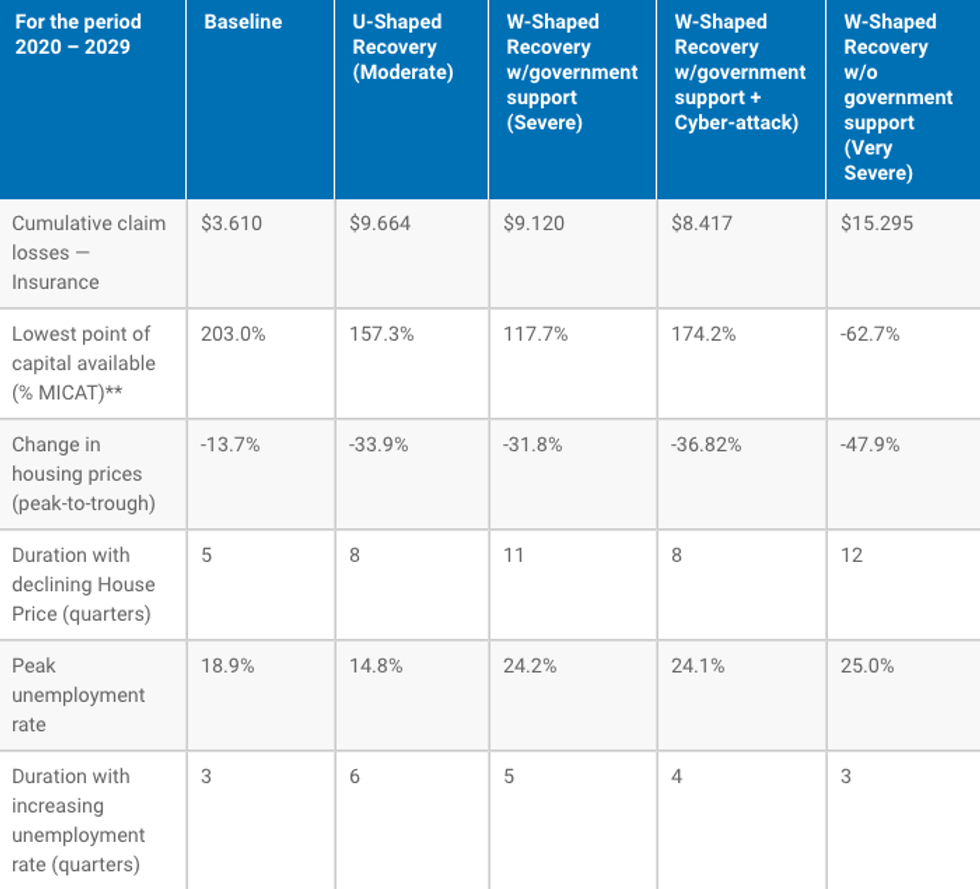

The results of the testing present three scenarios described as "plausible," which are outlined as follows:

U-Shaped Recovery (Moderate)

This is the least severe scenario. Here, pandemic measures prove successful, and economic activity sees a steep but short decline before bouncing back relatively quickly. This assumes a cumulative, peak-to-trough decline in Gross Domestic Product (GDP) of 7%.

W-Shaped Recovery with Government Support (Severe)

A partial recovery, followed by a return of COVID-19 outbreaks, loss of confidence and a prolonged recession. Government intervention, in this scenario, limits impact; the result is an assumption of a sharp and immediate decline in equity and oil prices, the failure of four mid-size financial institutions and one private mortgage insurer.

W-Shaped Recovery with Government Support and Cyber-Attack (Severe)

This plot's goal was to assess an imminent cyber-attack on the financial system during COVID-19 outbreaks. This is another scenario assuming a W-shaped recovery, albeit with less severe economic assumptions compared to the above Severe scenario.

The gravest scenario the CMCH presents is that of "W-Shaped Recovery without government support." The storyline mirrors the first W-shaped government support scenario above, but this time, "assumes no government intervention."

Described as "Very Severe," the plot is categorized as "implausible," and maintained a goal of assessing the mitigating effect of government support on businesses and individuals to better reflect a stressed version of the current situation.

The pandemic stress scenarios were completed between Q1 and Q3, 2020, and included "sensitivity analysis to key macroeconomic variables." Considering the timeline the theories were posed within, the recorded results don't include any data that would have been made available past the end of Q3.

The report also emphasizes that the scenarios are for testing purposes only, and aren't to be read as predictions or forecasts. This caution is an important one, as CMHC has come under fire -- more than once -- in recent months, as phrases including "fear-mongering" and "no longer relevant" have been used with regards to their Housing Market Forecast.

(In the latter half of 2020, several Canadian economists surveyed said they didn’t believe the Canadian property market would fall as far as what was initially forecast for the year in regards to the CMHC's previous property forecast, which called for a 9-18% price drop.)

However, the stress testing exercise is unique, and does stretch the imagination to consider what could happen, if the perfect storm of circumstances occurred. To be fair to even the most severe of the above scenarios, thinking back to January of last year, who could have realistically predicted what the year had in store?

(And if someone had, would anyone have believed them?)

“As we continue to deal with the impacts of the COVID-19 pandemic, it is important to monitor the evolving financial risks facing Canadian housing markets including an uneven economic recovery impacting most vulnerable populations," says Nadine Leblanc, Chief Risk Officer, Canada Mortgage and Housing Corporation.

"Stress testing exercises like this are an essential part of effective risk management and vitally important to the long-term health and stability of Canada’s housing finance system.”

According to the stress testing write-up, CMHC would remain solvent and well capitalized in all scenarios, except for the one described as Very Severe. In that situation, CMHC would be forced to call upon its recapitalization plan. Further, in all of the scenarios, CMHC retains access to sufficient liquidity to meet its insurance and Timely Payment Guarantee (‘TPG’) obligations.

READ: Why Hasn’t the Much-Feared “Mortgage Deferral Cliff” Happened?

The report says the range of estimated losses in mortgage loan insurance between 2020 and 2029 is between $3.61B and $15.30B. A wide range, indeed, which reflects the above varying scenarios and "the high level of uncertainty in outcomes." Another key factor for estimating future losses, the report says, is the percentage of deferred mortgages that recover.

Ultimately, CMHC says the combination of available government support and the shape of recovery will determine economic outcome. A second COVID-19 wave could create significantly higher risks, they said (perhaps, considering the Q3 end date, before the second wave had made such an entrance into many Canadian lives).

The impacts of those second-wave risks would be determined by a borrower's geographical location, employment type, and dwelling type.