When the going gets tough, the tough... look to the Canadian housing market for inspiration on how to keep their cool.

Or, at least, that's what you'd expect to be true, considering how resilient the market has proven itself to be since the dawn of the COVID-19 pandemic.

Since this time last year, countless offices have closed, small businesses have shuttered -- many for good -- and we've bid goodbye to most facets of life considered "non-essential."

But through it all, holding strength, the nation's housing market has soared. Now, newly-released data from BMO Bank of Montreal is showing just how much gumption the sector has held through the last year; a measurement that, per the data, puts Canada's housing market action high above that of our southern neighbours.

READ: “Heat and Hangovers” in Toronto Real Estate 2021 Forecast

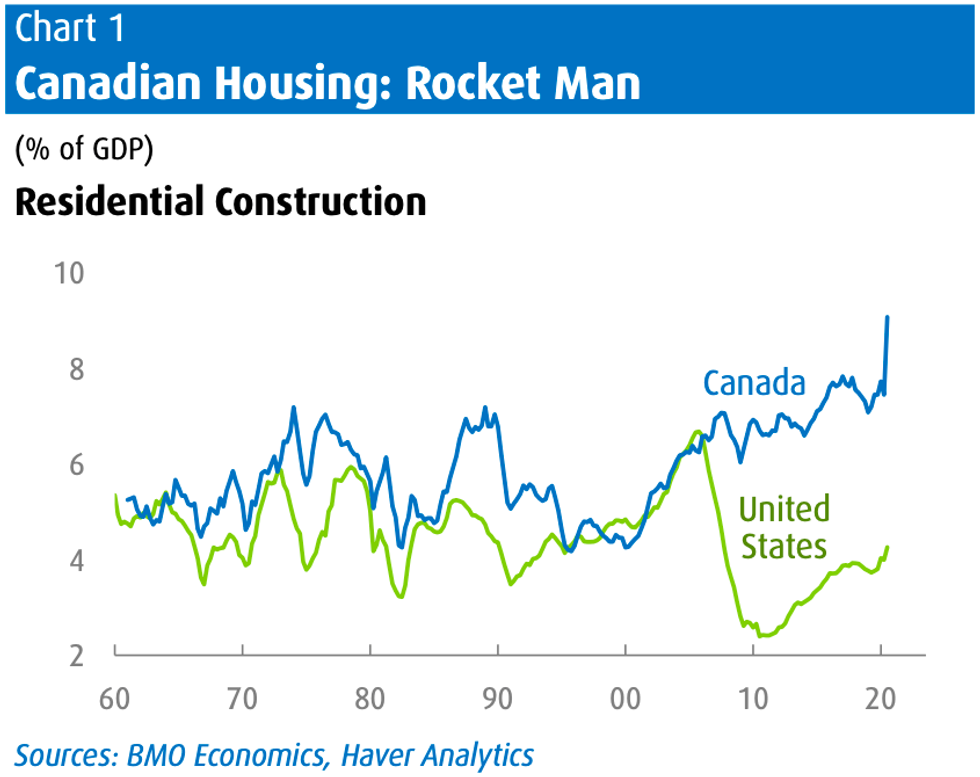

Resilient sales, continued construction activity, and record prices worked together to bring housing's share of Canadian nominal Growth Domestic Product above 9% by 2020's third quarter.

"To say 'that’s an all-time high' would be an understatement," reads BMO's Unbreakable Canadian Housing?, which notes the percentage floats well over the long-run norm of "a bit less than 6%," and more than doubles the current US ratio of 4.3%.

"Historically, housing takes up a bigger share of Canada’s GDP compared with the U.S., but the spread has gapped up from an average of less than 1 percentage point in the 50 years to 2010 to today’s extreme of almost 5 [percentage points]," the report explains.

"Suffice it to say that this was diametrically opposed to what the conventional wisdom expected for the housing market during the depths of the spring lockdown, including an official call for a double-digit price decline. Instead, residential investment—which includes new building, renovation activity, and sales costs—was a rare source of growth."

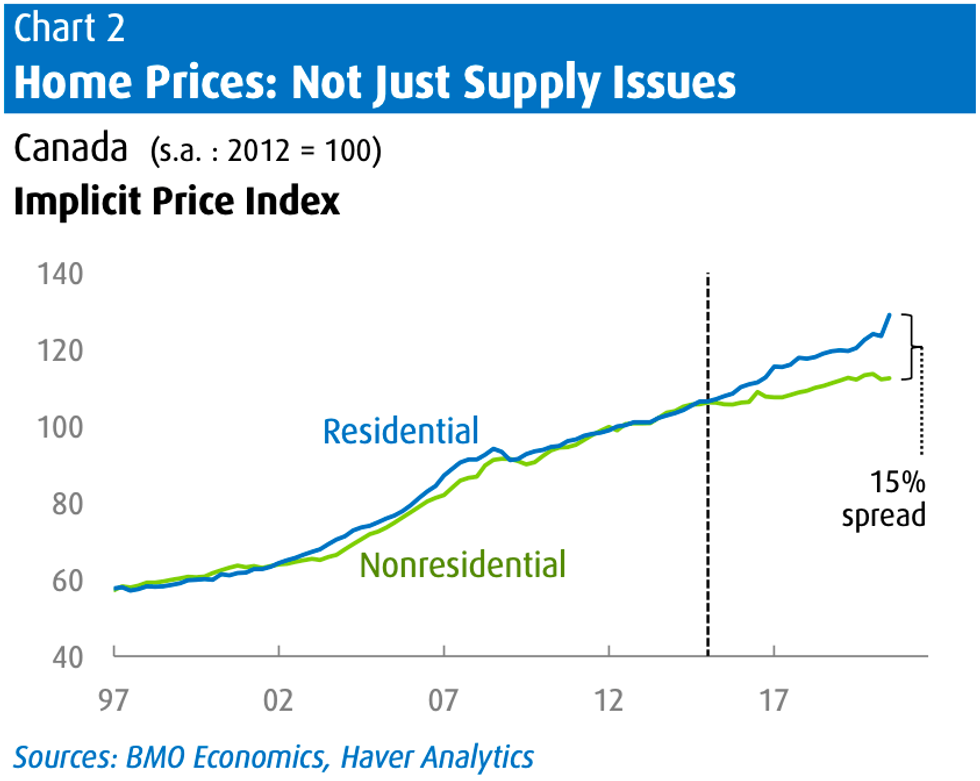

What's more, the report notes: the U.S. isn't lagging in its housing-related recovery. In fact, the country's rebound has been called "relatively quick," but even so, the neighbouring nations are seeing large divergence. To this point, the report highlights that while strong building activity plays a major role in overall spending on housing, "raging home prices" play just as large a part.

"The real residential construction-to-GDP ratio is at a 30-year high of 7.8%, but actually not far from the average of the 1970s and 1980s (7.6%). So, the true extremes are on prices. Many have pointed to supply issues as the main cause of lofty home prices, including zoning constraints or building costs."

Those factors would play into construction projects across the board -- not solely residential ones -- and as a result, non-residential prices rose mostly in-line with housing prices up until 2015, approximately. After that year, clear separation in the costs is obvious; home prices increased much more rapidly in the last five years, which is something the report says points to "a fundamental change on the demand side."

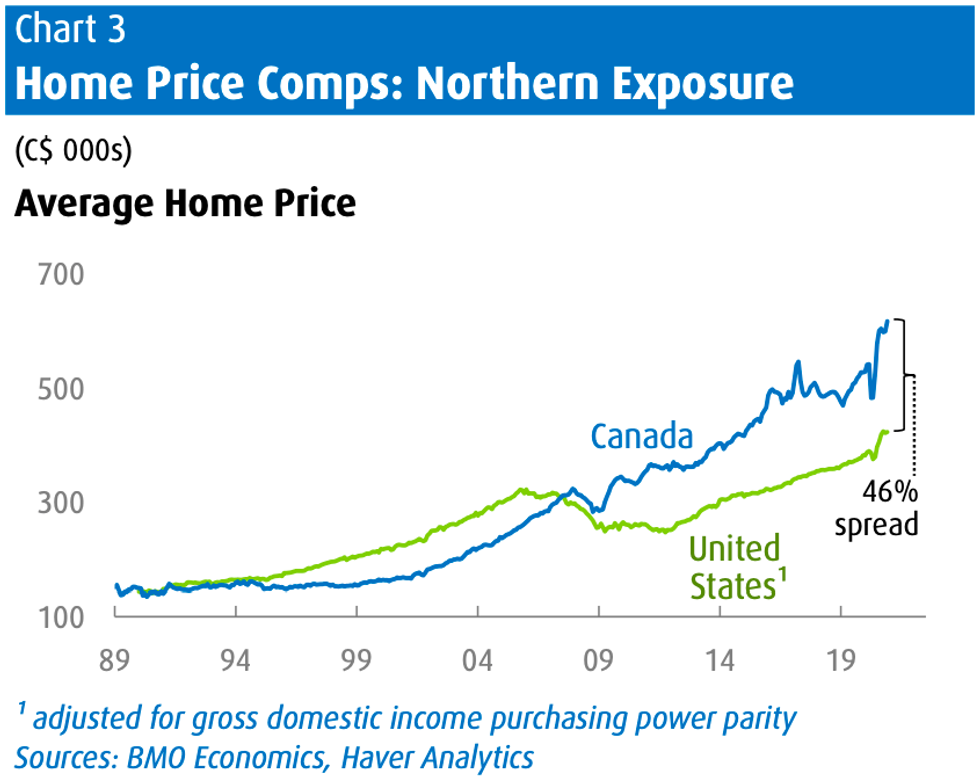

And although comparisons with U.S. activity are "always fraught with serious challenges given differences in incomes, mortgage markets, interest rates, urban/rural splits, housing stocks, and a variable exchange rate," such a practice, the report says, is still worth seeing through; the results can help illustrate "just how extreme Canadian home prices have become."

Via a purchasing power exchange rate -- which is a "very stable measure" that considers income differences -- existing average U.S. home prices were converted into CAD terms. In December, the seasonally adjusted average Canadian home price was $617,000, while the U.S. mean home price was roughly $420,000 (US$350,000).

That's a gap of approximately 46%.

Now, well into January, the comparison continues to be dramatic. With the current market exchange rate, the average U.S. price is equal to approximately C$445,000, meaning Canada's average home prices continue to hover a whole 40% over those in the states.

It's a gap of 40% to 50%, and, the report says, the answer to "why?" isn't particularly straightforward, as the question can be approached from various facets of both demand and supply.

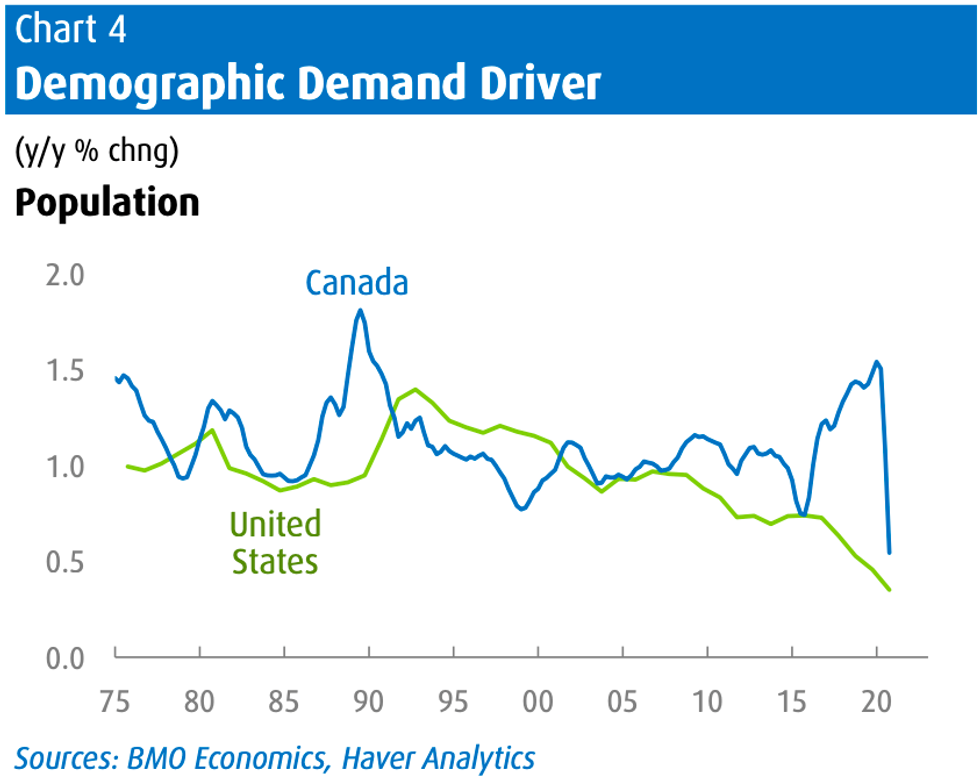

In terms of demand, the report begins by highlighting demographics: "in particular, stronger population growth in recent years."

Beyond demographics, lower interest rates are cited as a contributing factor, as "Canadian mortgage borrowing is clustered in the 5-year space or under, versus the U.S. preponderance of 30-year mortgages, which tend to carry higher rates." Also, though the rate of urbanization is similar between the U.S. and Canada (just over 80%), a higher share of Canada's population lives in the largest and priciest cities.

"For example, a third of all homes sold last year in Canada were in the three biggest cities; and, these are precisely the three cities where prices look stretched relative to incomes," says the report.

Further, after the U.S. housing bust of 2007-11, home ownership levels "plunged well below" those of Canada. (That said, however, levels have begun to recover "notably" in recent years -- Canada's were at 68.7% according to the 2016 Census, while much more updated U.S. figures put the country at 68.4%.) Lack of capital gains taxes on Canadian principal residences, too, reportedly plays a role in "juicing investment in real estate" and would, naturally, contribute to high home prices relative to those in the U.S. In the states, gains exemptions are reportedly limited to $250,000 (or $500,000 for joint filers) and can be claimed every two years only.

This factor is countered though, the report says, by partial mortgage deductibility for those in the U.S.

"Sorting through that list, the only truly compelling factor is Canada’s relatively robust population growth, driven primarily by net immigration. (That growth happens to have nearly stalled out in 2020, but will almost certainly rebound in coming years; but, so too will U.S. inflows with the new Administration looking to reset immigration policies,)" the report says.

"As mentioned, many also point to supply constraints and costs as a relative driver. While a factor, we view it as secondary to the demand side forces."

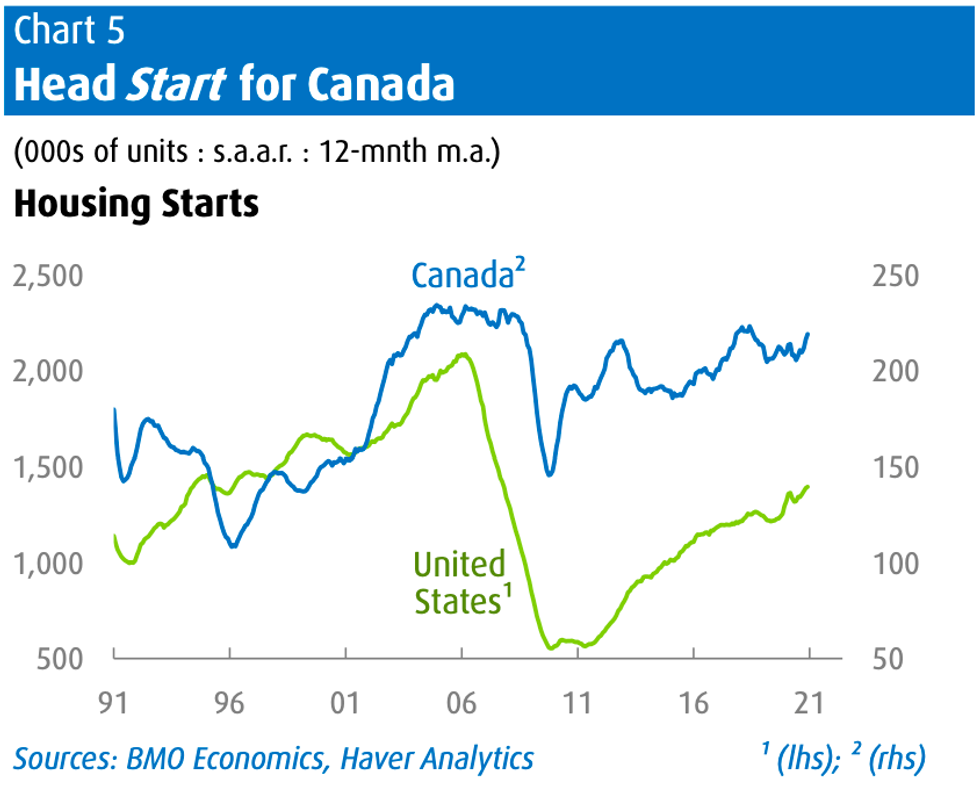

Indeed -- supply issues and all, as they've arisen -- Canada's new housing starts have been above those of the U.S. pace, on per-capita terms, for years. This is due to "robust population growth," (and, perhaps, it may also be a response to people voting with their dollar).

Indeed, the report acknowledges that a "more fundamental answer" may exist in that Canadians have, en masse, decided to allocate more resources to housing than other countries have, thus, "consuming" more properties as well.

"That’s not necessarily a bad thing," the report says. "Just a consumption choice."

But it is up for debate, whether the strong investments that go toward housing in Canada really reflect the preferences of those who live here. It could be considered, some may suggest, "a misalignment of resources."

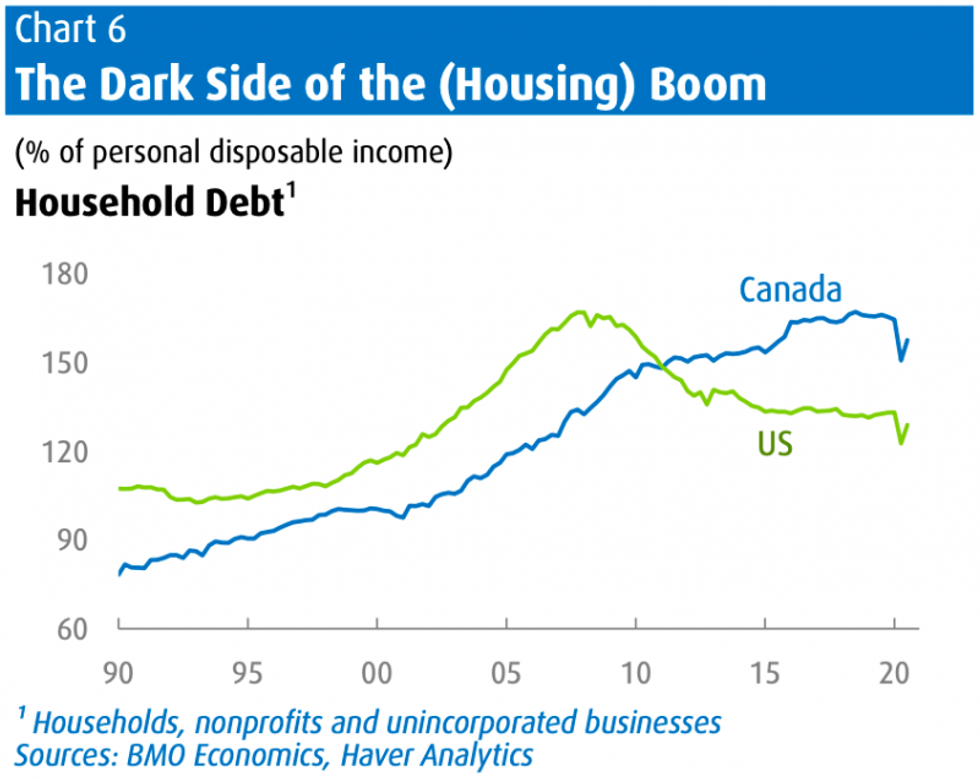

Whether it's truly the desires of Canadians or not, when it comes to a heavy investment in "housing consumption," there is a price to pay, and that's debt.

"Canada's household debt/income ratio forged above the U.S. about a decade ago and never looked back," the report notes. In 2020, the ratio "took a step down" due to a spike in household incomes (see: government support), alongside dept-growth cooling (even if only momentarily).

But in the last year, mortgage debt growth has increased 7.5% -- the fastest heightening in over nine years -- and while general household debt has been held back by "a slide in consumer credit," the report foresees a reverse in that when life (and, by association, spending) returns to relative normalcy.

"Incomes will inevitably take a small step back when some of the exceptional government support programs begin to wind down," the report says. "The point is that the respite for household debt ratios is expected to prove temporary, and the focus will revert to this underlying issue when the pandemic eventually fades as economic concern #1."