The pandemic, and the atypical years that followed, turned Canadians on their heads in more ways than one. For those who grabbed the opportunity for a cheap mortgage with both hands, the win was short-lived. Within years, the mortgage space would be rife with warnings of a renewal wave sold as nothing short of jarring.

In November 2024, Canada Mortgage Housing Corporation (CMHC) reported that around 1.2 million fixed-rate mortgages — $300 billion’s worth — would be up for renewal in 2025, and of those, over 85% were taken out when the policy interest rate was at or below 1%. At the time CMHC put these figures out, the benchmark rate was 3.75%.

Separate Bank of Canada estimates from July 2025 suggested that roughly 60% of Canadian mortgage holders renewing by the end of 2026 would face higher payments, with households expected to see payments that were 5% higher in 2025 — and 6% higher in 2026 ± compared to December 2024.

But the warnings have eased, and Canada’s mortgage space seems to be turning a corner. A new analysis from TD Economics’ Maria Solovieva highlights that debt serving costs have fallen, while mortgage interest costs are poised to — both indicators of a more palatable landscape for Canadian mortgagers.

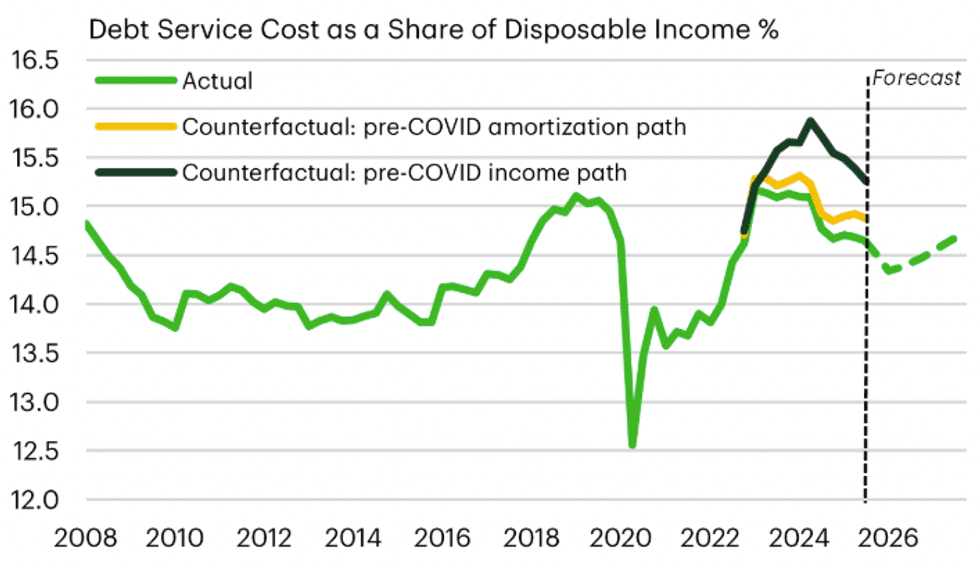

Income growth and longer amortizations are blunting mortgage shock/Statistics Canada, TD Economics

Income growth and longer amortizations are blunting mortgage shock/Statistics Canada, TD Economics

“The most telling sign that Canadian households have weathered the renewal shock is also the simplest: they are spending less of their income on debt. The debt service ratio for households is below its recent highs in 2023, suggesting the greatest strain on consumers has already passed,” writes Solovieva.

The ratio is down for two reasons: longer amortizations and healthy income growth. Internal data from TD shows that average mortgage amortization length has been on the rise since 2021, and is currently around 16 months longer than it was prior to the pandemic. Meanwhile, personal disposable income has grown at a faster pace in the past three years than the three years leading up to the pandemic.

“Faster income growth cushioned a meaningful share of the interest rate shock. This has turned a mortgage ‘cliff’ into a much gentler ‘hill,’” Solovieva explains.

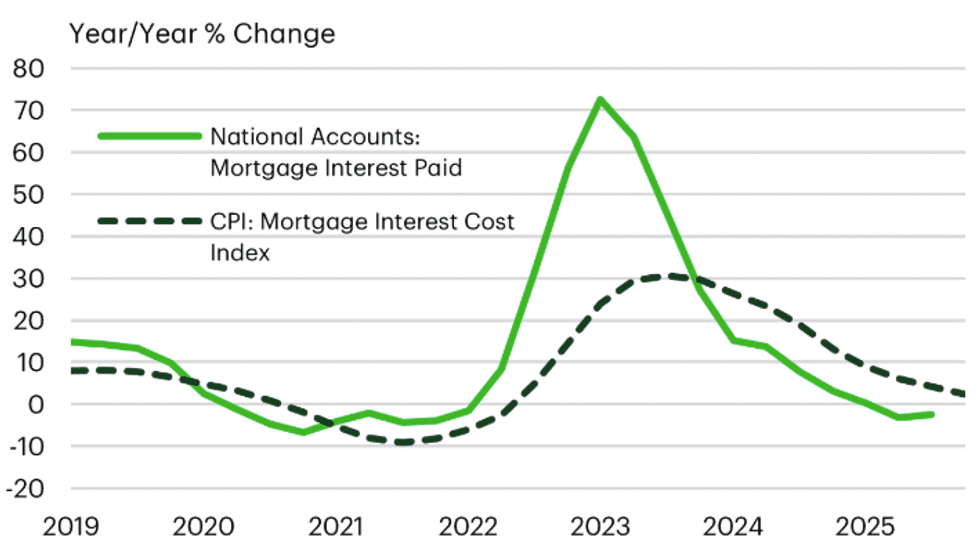

Canada's mortgage interest cost index is nearing deflation/Statistics Canada, TD Economics

Canada's mortgage interest cost index is nearing deflation/Statistics Canada, TD Economics

The report also looks at mortgage interest costs (MIC), which is a component within shelter inflation that came in at 31% (year over year) in August 2023, but is now down to just 1.2% (as of January). The metric is informed by changes in dwelling prices and changes in interest rates.

Solovieva notes that there tend to be “several quarters” of lag in MIC, but that that it is expected to come down gradually nonetheless.

“The more plausible base case for MIC turning negative end of 2026-beginning of 2027, based on national accounts’ mortgage interest paid as a leading indicator,” she writes. “Deflation in MICs is unlikely to be dramatic, as interest rates are projected to stabilize well above pre-pandemic levels. But its directional signal is consistent with the broader story: the mortgage renewal headwind that has suppressed consumer spending for three years is losing force.”

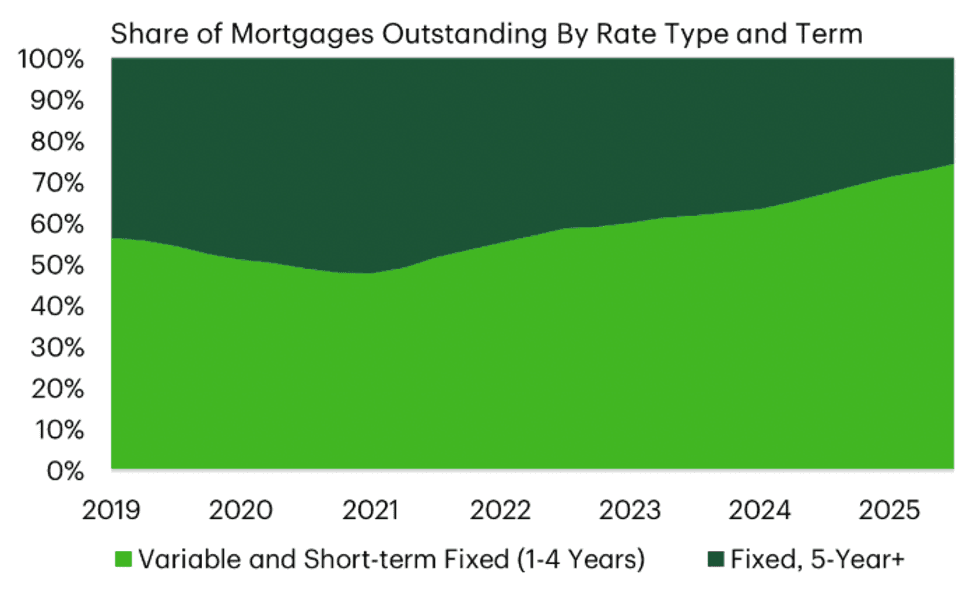

Canada's mortgage stock is more rate-sensitive today/Bank of Canada, TD Economics

Canada's mortgage stock is more rate-sensitive today/Bank of Canada, TD Economics

The final factor at play is the pandemic renewal cycle itself, and the reality that it is finally coming to and end. “Until recently, the dominant renewal dynamic was mortgages originated at ultra-low rates resetting higher. That trend is now reversing,” says Solovieva.

It also matters that there is now a larger share of variable-rate, variable payment mortgages, which are more interest rate sensitive than five-year fixed, at a ratio of 73 to 27. In 2022, the ratio was 55 to 45, and in 2024, it was 66 to 34.

“This shift implies that recent interest rate cuts should pass through to borrowers more quickly than rate hikes did during the tightening cycle,” says Solovieva. “Our internal mortgage data confirms that the turning point is on the horizon. Early in 2026, modest payment increases are expected to persist, but by the second half of the year, declines become the dominant outcome as the share renewing into lower rates takes over.”