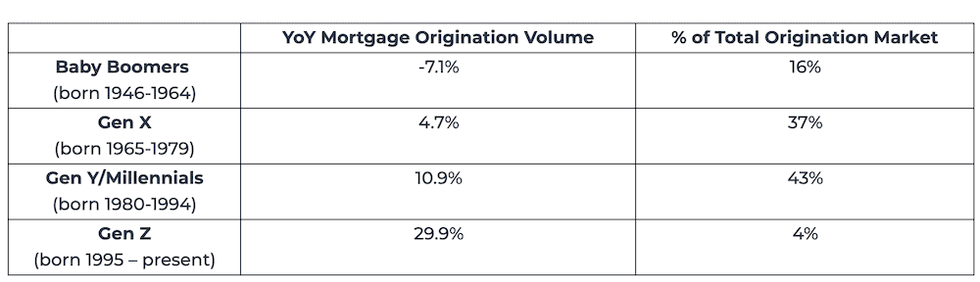

As the Canadian housing market reached frenzied new peaks over the course of 2021, it’s no shock that the number of new mortgages taken out has also swelled -- but what is perhaps surprising is that the Generation Z age group (those born between 1995 - present) are steadily accounting for a bigger share of those borrowers.

The Q4 2021 TransUnion Credit Industry Report (CIIR) reveals that in the third quarter of 2021, the number of mortgage originations rose 5.6% year over year, with the proportion of Gen Z mortgage borrowers surging 30%, well outpacing any other age group. While still accounting for just a fraction of the mortgage market overall at 4% (compared to 43% for Millennials and 37% for Gen X), it’s an interesting development given how housing affordability has eroded in markets across the nation. Overall, mortgage balances rose 11%, reflecting hot price growth, reveals the report.

TransUnion

TransUnion

TransUnion says that as home prices soared over the course of the fourth quarter, fueled by cheap borrowing rates and tight inventory, the average mortgage balance for individual consumers increased 10% year over year, to $320,835. This was especially prevalent in Ontario and British Columbia, where balances rose 22% and 19%, respectively.

Not surprisingly, this was concentrated in the most expensive urban centres: the average Torontonian who took out a home loan last quarter now carries a 16% higher mortgage load, at $580,470, while Vancouverites carry a mortgage balance sheet of nearly $700,000, up 13% to $691,780. Additional consumer research from TransUnion’s Consumer Pulse survey shows rising home prices are a barrier to homeownership for 44% of respondents.

Canadians Have Been Better at Paying Off Debt During Pandemic

Despite taking on much larger chunks of mortgage debt, though, consumers have been all around better at paying their overall debt off, as the level of delinquencies have been lower than expected for several quarters.

Credit card delinquencies (defined as going 90 days or more past due on at least one credit card) rose two basis points (bps), while personal loan delinquencies (past due by 60 days on at least one installment loan) rose by 9 bps in Q4. While it was the second consecutive quarter for increases, TransUnion says that's a sign of recovery and a growing economy as consumers return to pre-pandemic credit behaviours.

Rising Rates Will Hit Canadians' Ability to Pay

Of course, the cost to borrow is now officially on the rise: the Bank of Canada announced its first rate hike since 2018, to 0.5%, this morning. Consumer lenders have already started to pass the higher benchmark down to their Prime rates, and by extension, their variable-rate products. As a result, variable mortgage holders and those with lines of credit will see their payments increase, or less of their monthly payments going toward their principal debt.

READ: More Than Half of Canadians Can't Keep Up With Bills as Inflation Soars

Matt Fabian, director of financial services research and consulting at TransUnion, says rising interest rates will indeed cause a regression to pre-pandemic delinquency levels, though they’re expected to remain at manageable levels for the foreseeable future.

“Mortgage lenders are now contemplating interest rate increases, which may raise rates for Canada’s variable-rate holders, and this increased cost of debt may create some additional stress on consumer wallets,” he says. “Based on TransUnion’s previous payment hierarchy research, we do not traditionally see this impacting mortgage delinquency, as consumers prioritize mortgage payments, but other payments like credit cards may see an impact as consumers manage the allocation of disposable income to debt coverage.”

It’s good news that Canadians are foreseen to continue to be prudent with their payments, as the data also reveals the appetite for credit overall has effectively rebounded to pre-pandemic levels, with TransUnion’s Credit Industry Indicator (a measure based on demand, supply, consumer behaviour and performance) increasing 32 points year over year to 101.6. Total balance growth across all credit products rose 8.5%, driven mostly by non-revolving debt types, which include mortgages and installment loans. Revolving debt types, which include credit cards, rose 2%, as overall credit card spend rates are up 20% year over year, as the economy has re-opened.

Says Fabian, “Canadian consumers have demonstrated resiliency, with increased savings aided by government and lender assistance programs, and the credit market has remained stable throughout the pandemic.”