Down Payment

Learn what a down payment is in Canadian real estate, how much is required, and how it impacts your mortgage, insurance, and homeownership affordability.

May 22, 2025

What is a Down Payment?

A down payment is the initial lump sum a homebuyer pays upfront toward the purchase price of a property, with the remainder covered by a mortgage.

Why Down Payments Matter in Real Estate

In Canadian real estate, the down payment plays a critical role in determining mortgage size, eligibility, insurance requirements, and monthly payments. The minimum required down payment depends on the home’s purchase price:

- 5% for homes under $500,000

- 5% of the first $500,000 + 10% of the remainder for homes priced between $500,000 and $999,999

- 20% for homes priced at $1 million or more

If a buyer puts down less than 20%, the mortgage is considered a high-ratio mortgage and requires CMHC insurance. A larger down payment reduces the mortgage principal, lowers interest over time, and may eliminate the need for insurance.

Saving for a down payment is often the biggest hurdle for first-time homebuyers, who may also benefit from programs like the First-Time Home Buyer Incentive or use of RRSP funds through the Home Buyers’ Plan (HBP). Buyers should ensure their down payment funds are accessible and verifiable by their lender before closing.

Example of a Down Payment in Action

A buyer purchases a $600,000 home in Ontario. They contribute a 10% down payment of $60,000 and finance the remaining $540,000 through a mortgage.

Key Takeaways

- The upfront payment made when purchasing a home.

- Required minimum depends on the property’s price.

- Affects mortgage size, insurance needs, and interest paid.

- Less than 20% down requires mortgage loan insurance.

- Programs exist to help first-time buyers save or borrow.

Related Terms

- Mortgage Pre-Approval

- CMHC Insurance

- High-Ratio Mortgage

- Closing Costs

- Equity

CBRE Canada

CBRE Canada CBRE Canada

CBRE Canada

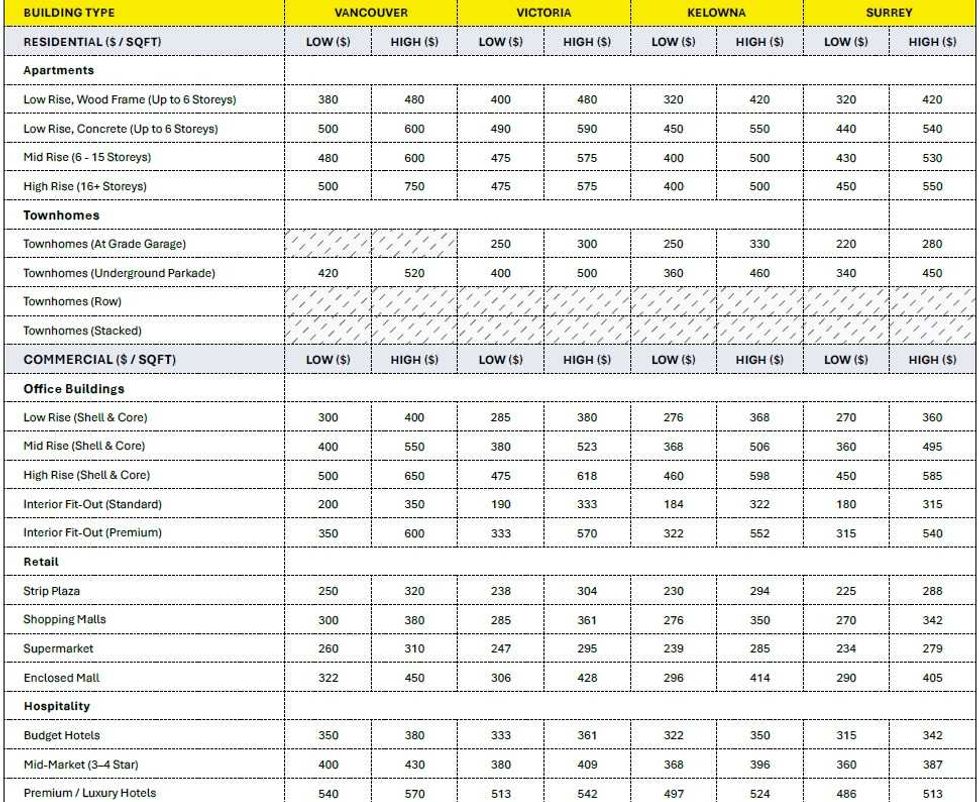

Construction cost ranges for British Columbia. (BTY Group)

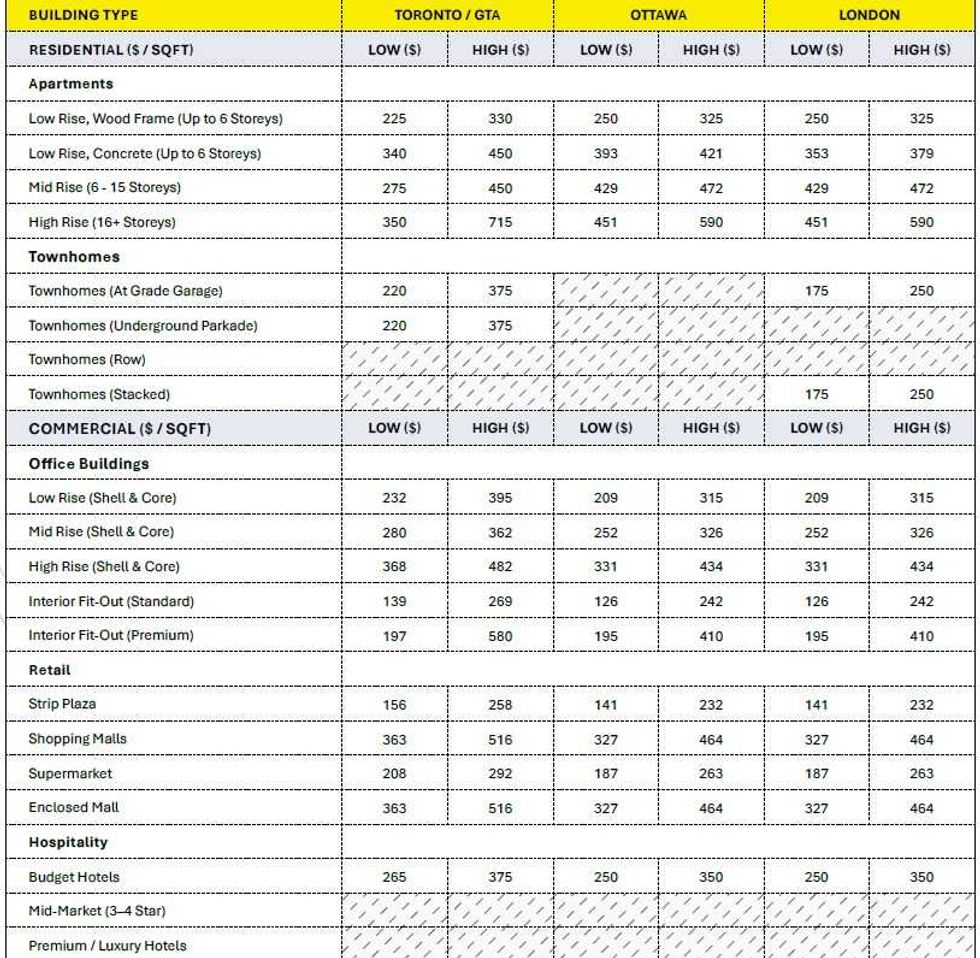

Construction cost ranges for British Columbia. (BTY Group) Construction cost ranges for Ontario. (BTY Group)

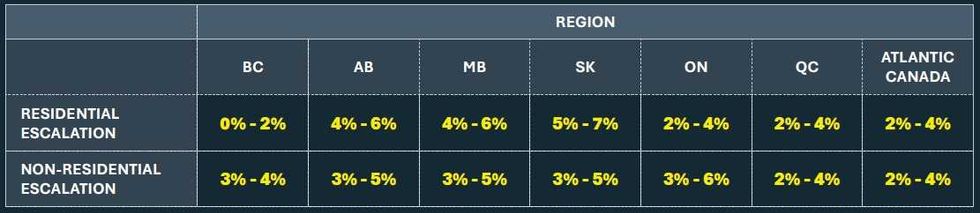

Construction cost ranges for Ontario. (BTY Group) Construction cost escalation projections by region. (BTY Group)

Construction cost escalation projections by region. (BTY Group)