There is a quiet tension running through Canada’s housing market. RBC’s latest report declares housing affordability to be at its “best” in three years, yet for most Canadians the reality feels unchanged. The dream of owning a home remains elusive, and the market is eerily still.

The truth lies beneath the headline. Three forces continue to exert pressure on affordability: house prices, interest rates, and household incomes. This trio does not operate in isolation. Together they form the core of every decision a buyer must make. Right now, all three remain out of alignment. Until they move in the same direction, the market will remain locked in a state of hesitation.

Progress That Feels Hollow

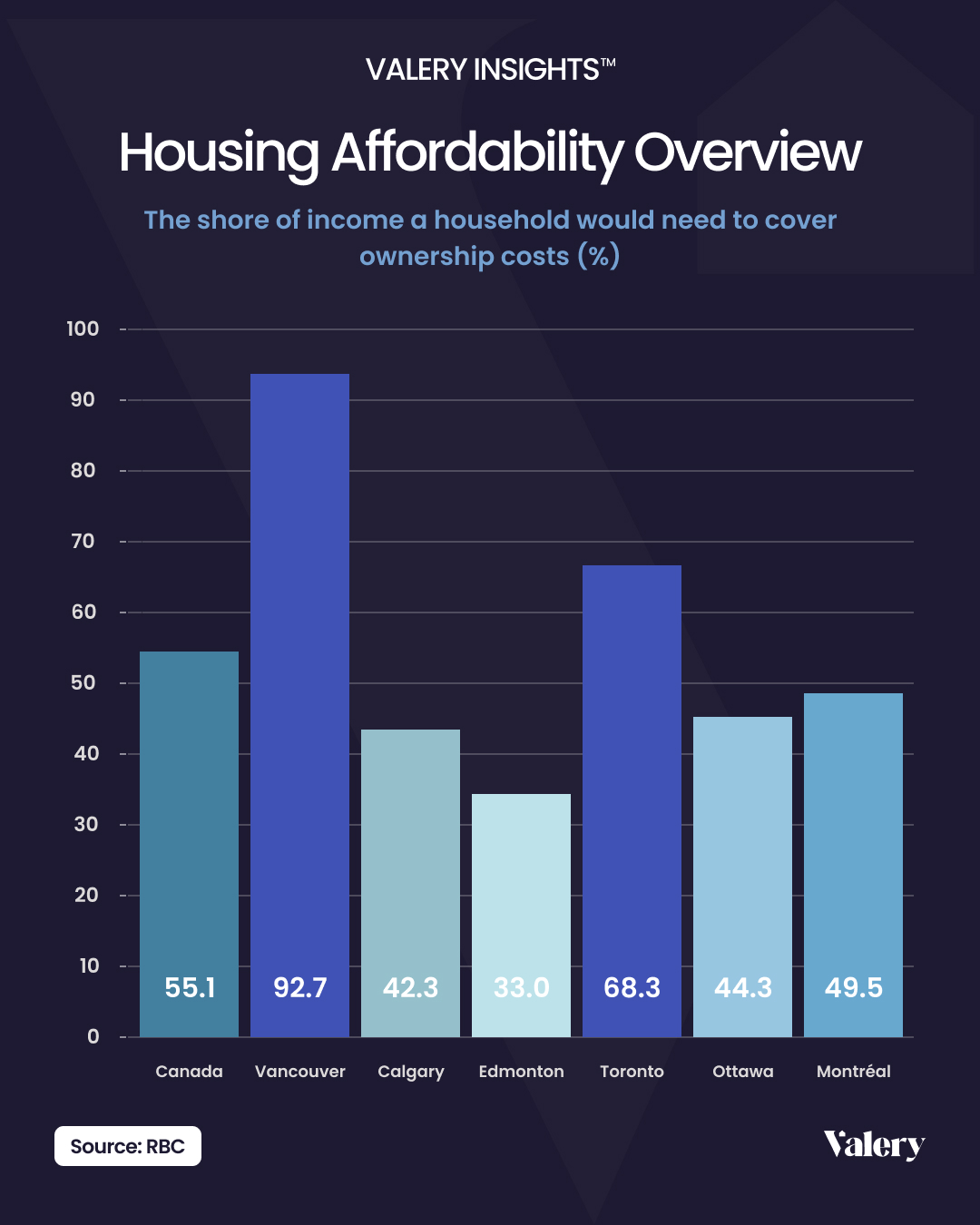

RBC calculates affordability by measuring the proportion of median household income required to carry the costs of homeownership. Nationally, this figure has dropped slightly to 55.1%.

The picture in Canada’s largest cities is far more severe. In Vancouver, ownership consumes an astonishing 92.7% of income. In Toronto, it takes 68.3%. Even Ottawa and Montreal sit far above historical norms. These numbers in addition to being alarming, are also symptomatic of a housing system where costs have decoupled from household earnings.

The charts tell the story, clearly.

via valery.ca

The Three Pillars Of Affordability

Affordability is often presented as a function of house prices alone, but this is a mistake. It depends on three intertwined elements: house prices, interest rates, and household incomes. All three must move in harmony to create a market where buyers feel confident to return.

House Prices

Home prices fell between 10% to 15% in Toronto and Vancouver after peaking in 2022. This adjustment gave some relief, but momentum has slowed. RBC’s analysis suggests only minor declines ahead, a scenario that leaves prices high relative to the earning power of Canadian households.

Without more significant price adjustments, ownership costs are likely to remain high relative to household incomes, stalling further gains in affordability.

Interest Rates

Interest rates have softened slightly from their peak, but the Bank of Canada now faces mounting pressure to hold steady. RBC’s recent interviews carried a clear message: Canadians hoping for significant rate relief may be out of luck.

Initially, RBC’s forecast diverged from those of other major Canadian banks, projecting more easing in the months ahead. But the tone across the financial sector has since shifted. Scotiabank’s Derek Holt went so far as to say the Bank of Canada “should not even be thinking about when to cut rates.”

The core issue is uncertainty over inflation. Economists remain split on how recent data will influence monetary policy, and this division has left buyers waiting in limbo. With rate cuts likely to be smaller and slower than many anticipated, affordability gains from borrowing costs alone seem limited.

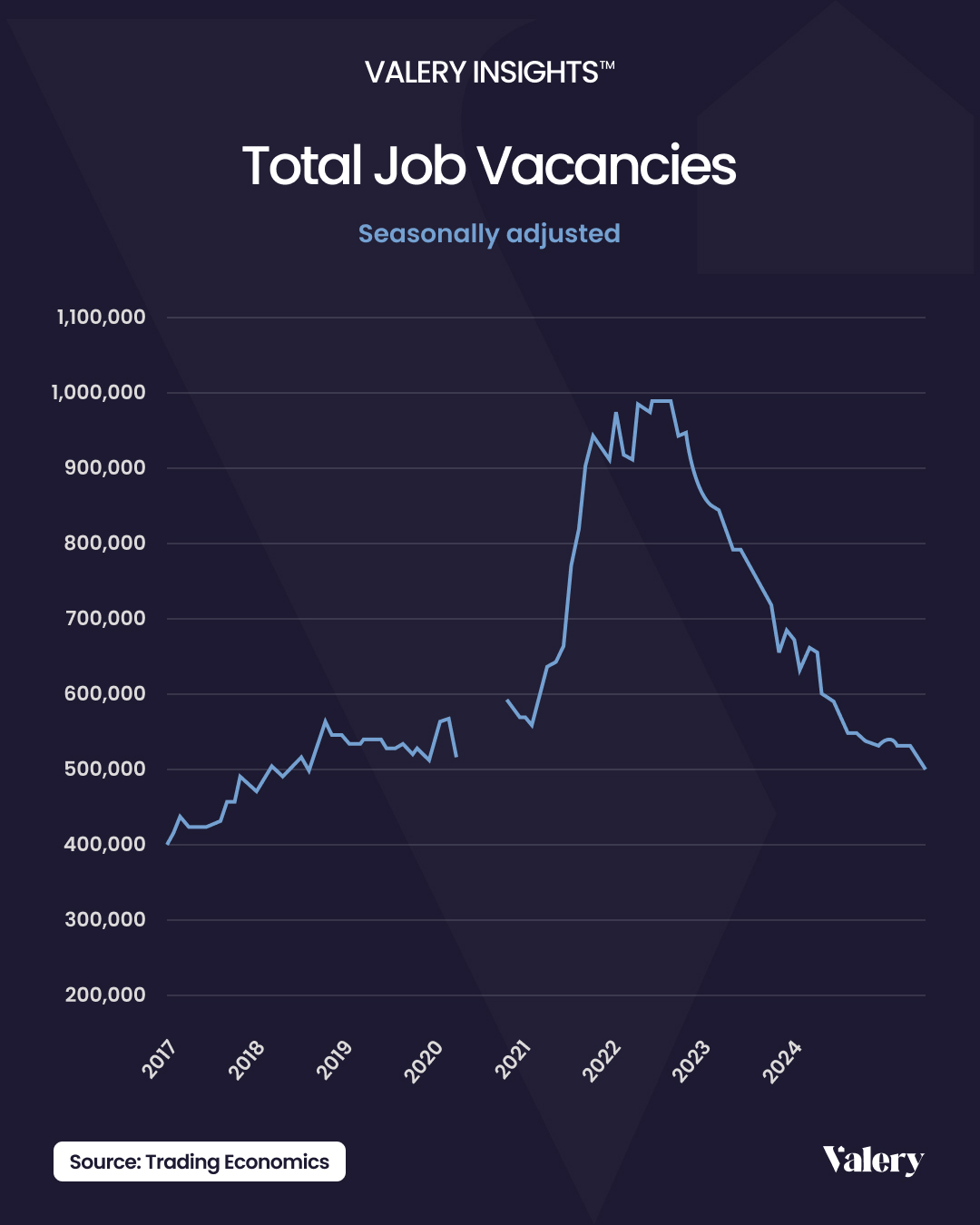

Household Incomes

The third pillar is equally fragile. Wage growth has been uneven. Job vacancies have fallen sharply since their highs in 2022, and unemployment has begun to rise. These trends suggest that household earnings are unlikely to grow quickly enough to offset high housing costs.

via valery.ca

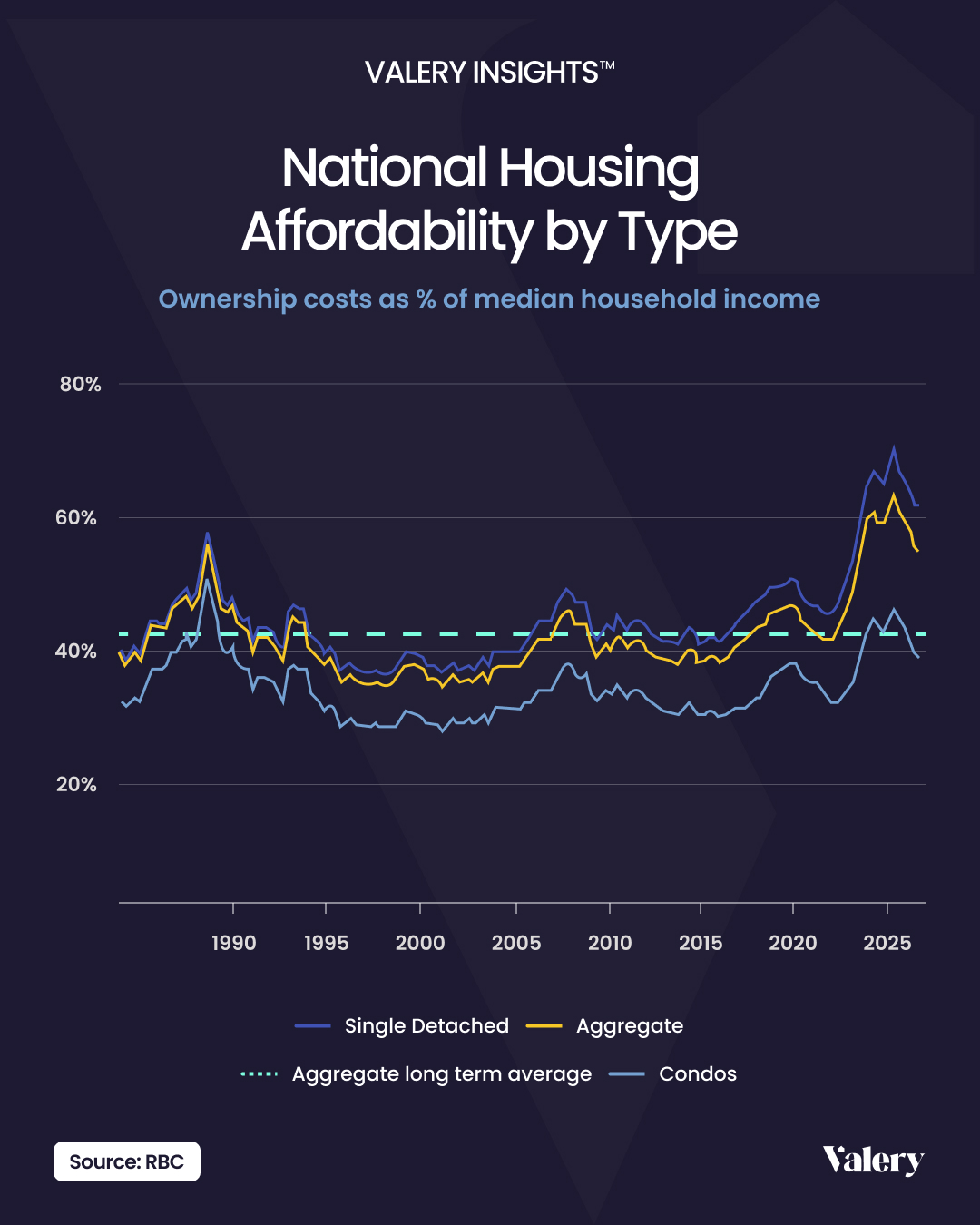

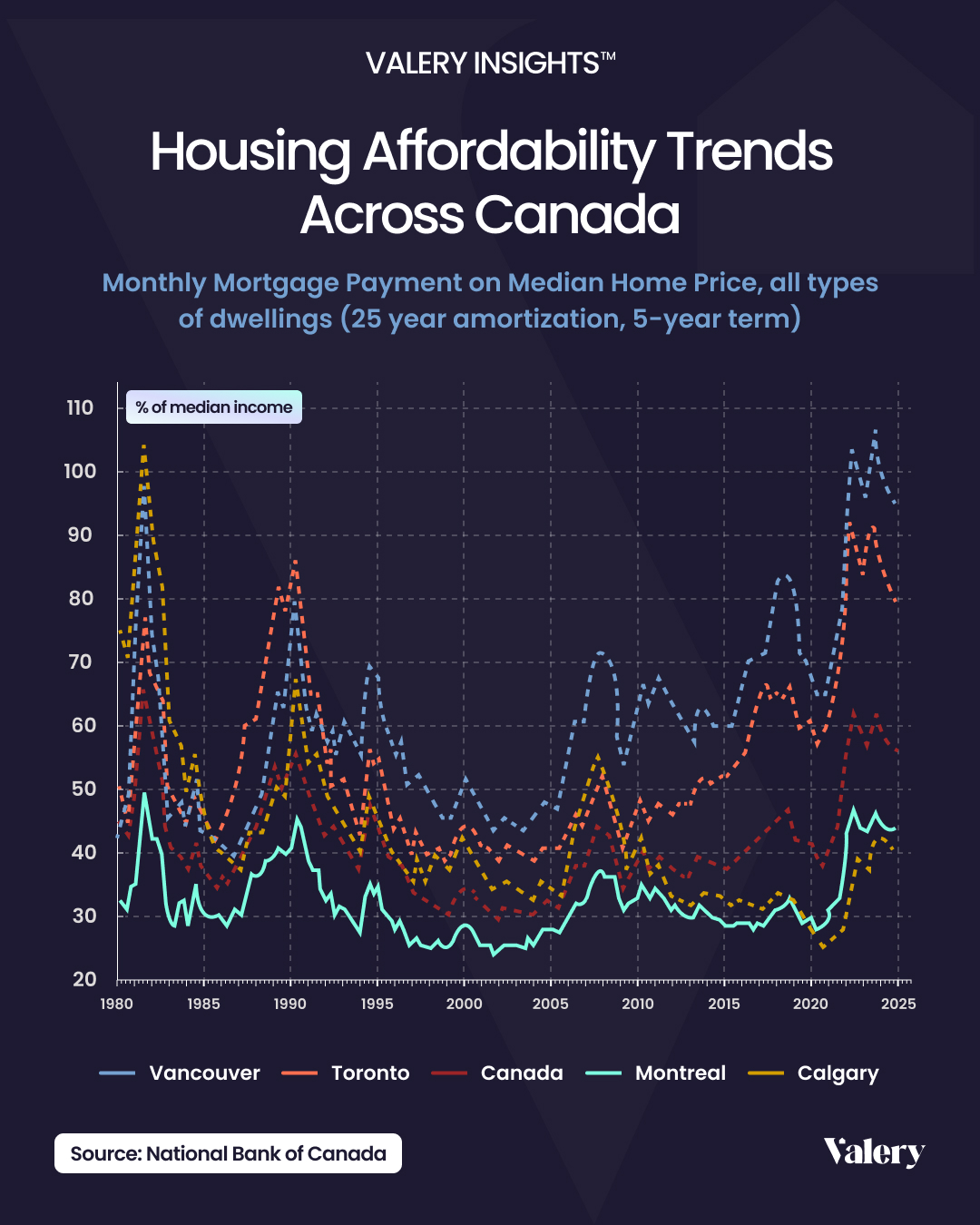

Lessons From Past Cycles

Canadian housing markets have long followed a familiar pattern. Periods of rapid price growth and interest rate hikes are often followed by a slow correction. Prices edge down, rates ease, and incomes eventually rise to meet the market.

The current cycle, however, remains incomplete. Even after recent price drops, ownership costs as a share of income remain far outside the range that defined previous periods of relative affordability. RBC’s data places this figure well above the 30-45 per cent band that supported healthy buyer activity in past decades.

via valery.ca

National Bank of Canada’s affordability monitor paints a similar picture. Costs remain elevated across housing types, reinforcing how much further the market must adjust before it becomes accessible to a broader range of Canadians.

via valery.ca

Why Prices Must Bear The Weight

With interest rates constrained and income growth unlikely to accelerate, house prices may be the only variable with room to adjust. This does not suggest a dramatic collapse. Instead, it points to a gradual, measured decline that realigns prices with the earning power of Canadian households.

Such a shift would bring clear benefits. More affordable housing would allow families to redirect spending toward other parts of the economy. It would also encourage higher transaction volumes in real estate, benefitting professionals who rely on an active market.

A Critical Moment For Canada’s Housing System

Homeownership has long been a cornerstone of the Canadian middle-class promise. Today, that promise feels increasingly fragile. RBC’s report acknowledges modest progress, but it also underscores how far the market must go before buyers can return with confidence.

Restoring balance will require movement across all three drivers of affordability. Until house prices, interest rates, and incomes align, the housing market will remain caught in a state of uncertainty.

This is more than an economic challenge. It is a test of Canada’s ability to build a housing system that serves the aspirations of its people.