Temperatures may be dropping outside, but Canada's housing market remains red-hot.

During the third quarter, demand for homeownership remained high throughout the country. But with housing inventories at near historical lows in virtually every market, competition intensified between buyers, putting pressure on prices and deteriorating affordability in the process.

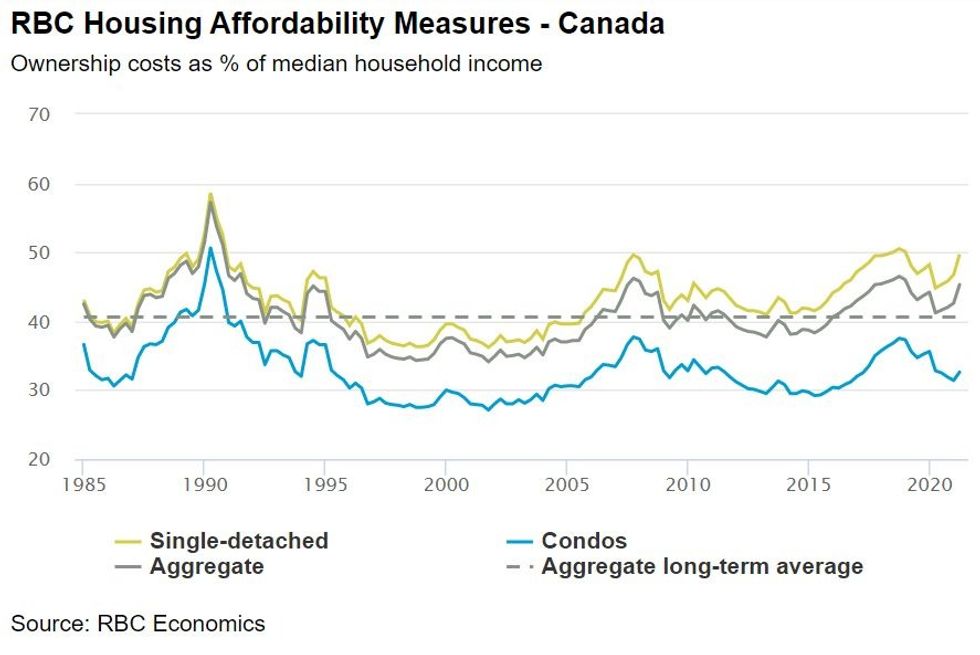

As a result, soaring prices and higher mortgage rates slammed housing affordability during Q3-2021, pushing RBC’s aggregate measure -- the ratio of ownership costs to household income -- up 2.0 percentage points to 47.5% -- its worst level in 31 years, according to RBC senior economist Robert Hogue. According to RBC, a rise represents a deterioration in affordability.

This jump comes on the heels of a huge 2.7 percentage increase in the second quarter of 2021, which completely reversed improvements from the start of the pandemic.

READ: 2022: Housing Sales to Ease, But Prices Expected to Rise Even Higher

RBC Q3-2021

RBC Q3-2021

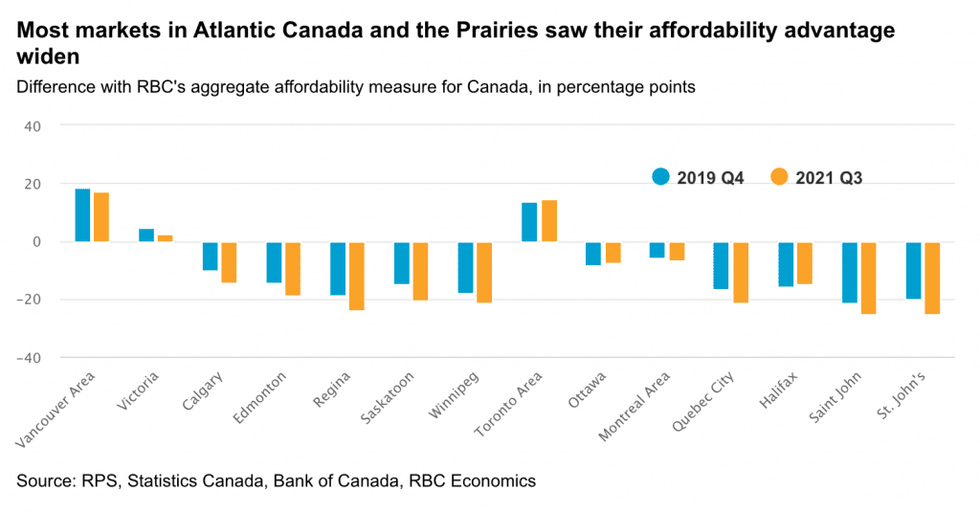

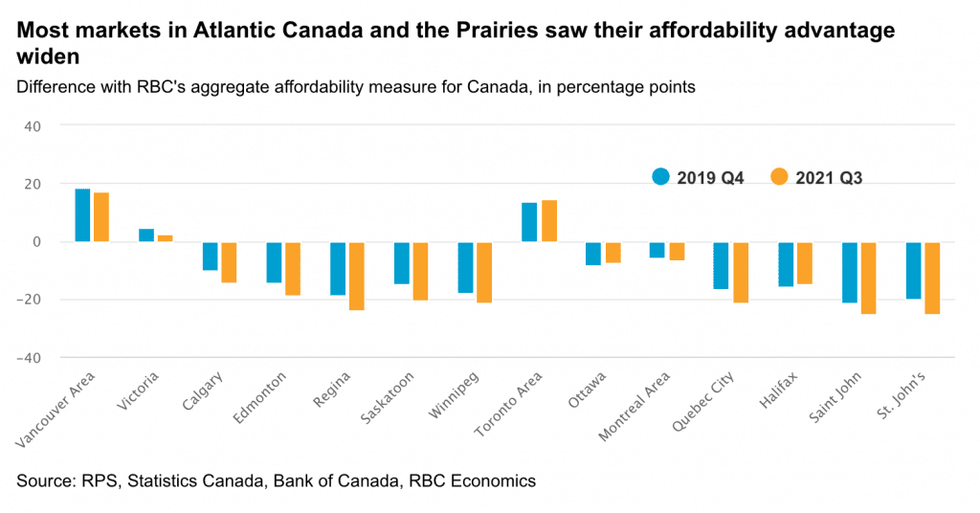

While housing affordability continues to erode, the bank says it's been an "uneven process" throughout the country, with some markets, particularly those already unaffordable like Toronto, experiencing greater erosion, while more affordable areas, like Atlantic Canada and the Prairies, worsening less and remaining well within historical norms.

As affordability throughout Canada deteriorates further, Hogue says some markets, specifically Toronto and throughout southern Ontario, have entered even less affordable positions in comparison to the rest of the country -- a trend the economist expects will drive some Ontario buyers toward more affordable regions of the country.

RBC Q3-2021

RBC Q3-2021

Meanwhile, as demand-supply conditions tightened, bidding wars became the new norm, even in markets that rarely see them, and intensifying in places more accustomed to them, Hogue said. But until both demand and supply return closer to balance, the economist says prices will only continue to rise higher.

Earlier on in the pandemic, homebuyers were benefiting from the declining interest rates that were offsetting the impact of rising property values. However, Hogue says that's no longer the case, as a small increase in the five-year fixed mortgage rate accounted for half the 2.0 percentage-point increase in the bank's aggregate measure in the third quarter.

And while the Bank of Canada has yet to raise interest rates, a slight rise in rates alone could drive up RBC's national affordability measure another 2.0 to 3.5 percentage points over the coming year. What's more, a further 5% increase in home prices would add an extra 2.0 percentage points. However, Hogue says income gains would be able to provide a partial offset.

READ: Omicron Will Only Stoke the Fire of Canada’s Already Red-Hot Real Estate Market

Unfortunately, the outlook for buyers is grim. Further deterioration in affordability could push many buyers out of the market -- or at least steer them away from the housing category. That being said, the bank says it expects buyers in Canada’s priciest markets, including in Vancouver, Toronto, Victoria and, to a lesser extent, Ottawa and Montreal, to be under the most pressure to reset their buying expectations.

"That would be the market’s self-correcting mechanism at work. So long as supply is slow in coming, much of rebalancing adjustments will fall on the demand side of the equation," said Hogue.

While affordability continues to be an issue, some markets still remain relatively more affordable. In fact, RBC’s aggregate measures remain well below their long-run averages -- and are likely to stay so in the year ahead -- in Calgary, Edmonton, Regina, Saskatoon, Winnipeg, Saint John, and St. John’s. The latter was the only market bucking the deteriorating trend in the third quarter.

RBC Q3-2021

RBC Q3-2021

That being said, RBC expects homeownership costs to continue to rise quickly in the period ahead -- similar to other industry predictions.

"Home prices re-accelerated amid strong demand and scarce inventories this fall. And borrowing costs are poised to get more expensive," said Hogue.

Given that fixed mortgage rates have already gone up since summer, RBC expects that the Bank of Canada will start to hike its overnight rate this coming spring, which would drive variable rates higher -- a repercussion that would be felt across the country.