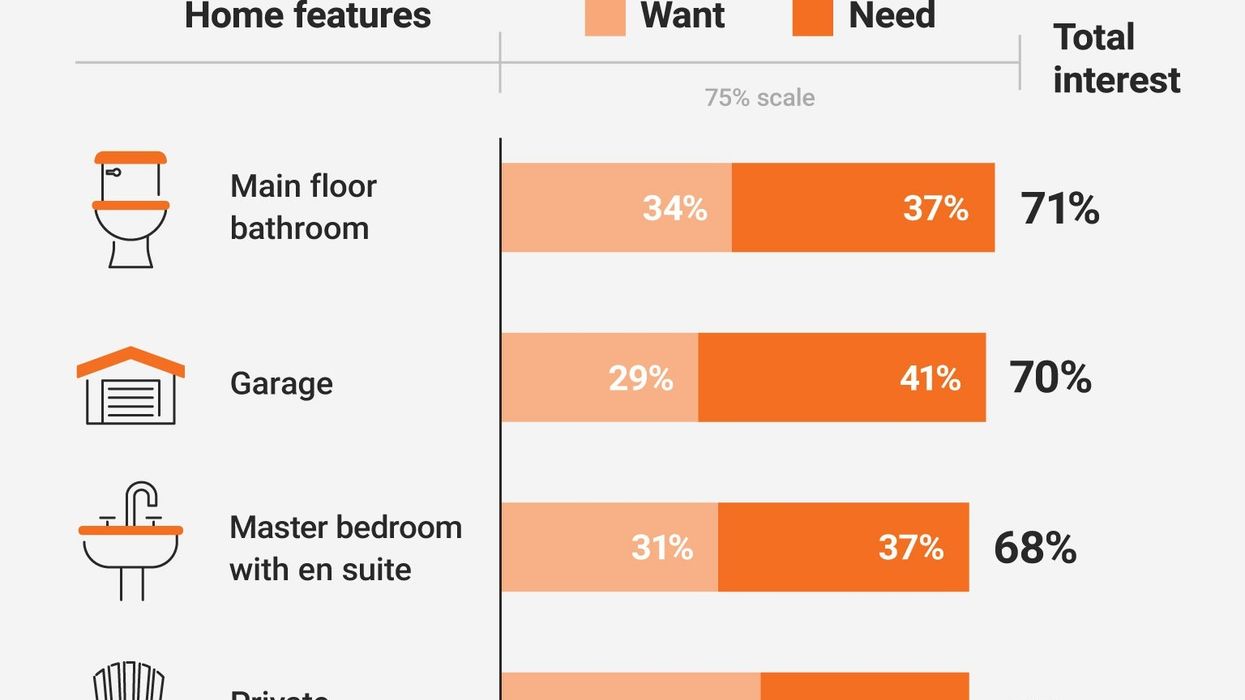

It’s a wild time now within the Toronto housing market — supply and demand is out of whack, prices are soaring out of reach, and competition is so fierce dreams are over before they even begin.

What’s more, the credit checks and new intake of a mortgage payment is more than enough to push prospective first-time home buyers into a frenzy.

Are you anxiously perched on the sidelines, nervous to jump into the biggest purchase of your life? We thought so. Cover your bases with these helpful tips:

1. Know your budget

Who knows how much you’re able to afford better than yourself? Forget those formulas that bankers use and do some number crunching. It will make you feel more confident in actually knowing how much you can really afford. Determine your budget based on your income, expenses, savings, debts, and assets. Don’t forget to factor in your lifestyle. Be honest with yourself. Acknowledging this might help with tweaking some everyday choices in order to afford that dream house.

But don’t get discouraged if your dream home requires some budget inflation. You might be better suited for a condo as being your starter home. Keep in mind that if you do overbuy on your very first home, it will be harder in the long run. It’s best to begin with smaller payments that you would make on a starter home. An upgrade is always a possibility down the road, and will probably have less stress attached.

2. Don’t forget about those extra costs

Excitement can get the best of us, and suddenly we forget about those extra fees. For example, closing costs can range from 1.5 per cent to 3.5 per cent of the total cost of the home. Not to mention other payment expectations like a home inspection fee, legal fees, property insurance and property tax, just to name a few. Make sure to always confirm those tiny (but important) details up front and centre.

These payments might not only include loan costs, but other costs like property taxes and homeowner's insurance. You may be required to buy private mortgage insurance (PMI) depending on the size of your down payment. Keep in mind that most lenders require PMI when a homebuyer makes a down payment of less than 20 per cent of the home's purchase price.

3. Get pre-approval for your mortgage

Thanks to that number crunching, you know exactly how much you can afford for a down payment. Getting pre-approved for your mortgage gives you an edge over other people who might be interested in the same property. Mortgage experiences often have a bad reputation of being stressful and non-transparent, and require a lot of rate haggling, which ultimately overwhelms that feeling of accomplishment and excitement with your first house.

These days, individuals have more options: banks, credit unions, mortgage brokers, or new digitally led mortgage experiences, like MogoMortgage. MogoMortgage pairs market-leading interest rates (without the haggling), with an online process supported by salaried mortgage specialists, and an interactive dashboard designed to encourage and reward members for paying down their mortgage.

4. Use your brains, not your heart

Check those emotions at the front door. Thinking logically and realistically is most important. Don’t let realtors pressure you into signing right on the spot. A property might pass you by, but the wrong choices typically come with consequences that might be difficult to recover from. A good rule of thumb is to refuse to step into any house that is listed above your budget.

5. Don’t look back

You know that saying, “don’t fix what ain’t broke”? Well same goes for after you’ve made your home purchase. Once you find it — stop looking! Focus on making that house a home. Bring some Feng Shui into the space, light up a great candle, have your first pizza dinner sans furniture, and start making those memories.