Canada added more new housing supply in 2025, driven largely by record rental construction and a growing share of missing middle housing — but new data suggests underlying vulnerabilities are building, particularly in major ownership markets like Toronto and Vancouver.

According to the Spring 2026 Housing Supply Report from the Canada Mortgage and Housing Corporation (CMHC), national housing starts rose 6% year-over-year in 2025, to 259,000 units. Activity exceeded the 10-year average in nearly every major market, with one notable exception: Toronto, where starts fell well below historical norms and reached the lowest per-capita level among Canada’s seven largest census metropolitan areas (CMAs).

While construction activity remained resilient overall, the report highlights growing concerns about the future pipeline of ownership-oriented housing, as condominium presales weakened sharply and unsold inventories climbed across several markets.

Rental And Missing Middle Construction Drive Supply

Rental development played the largest role in boosting housing supply in 2025. Across the country, the number of rental units under construction reached nearly twice the 10-year average, contributing to higher vacancy rates and slower rent growth.

Rental starts hit record highs in several major markets, including Calgary, Edmonton, Ottawa, Halifax, and Montréal. Toronto recorded its second-highest level of rental starts on record, while Vancouver — despite a slight decline — still saw rental construction remain elevated by historical standards.

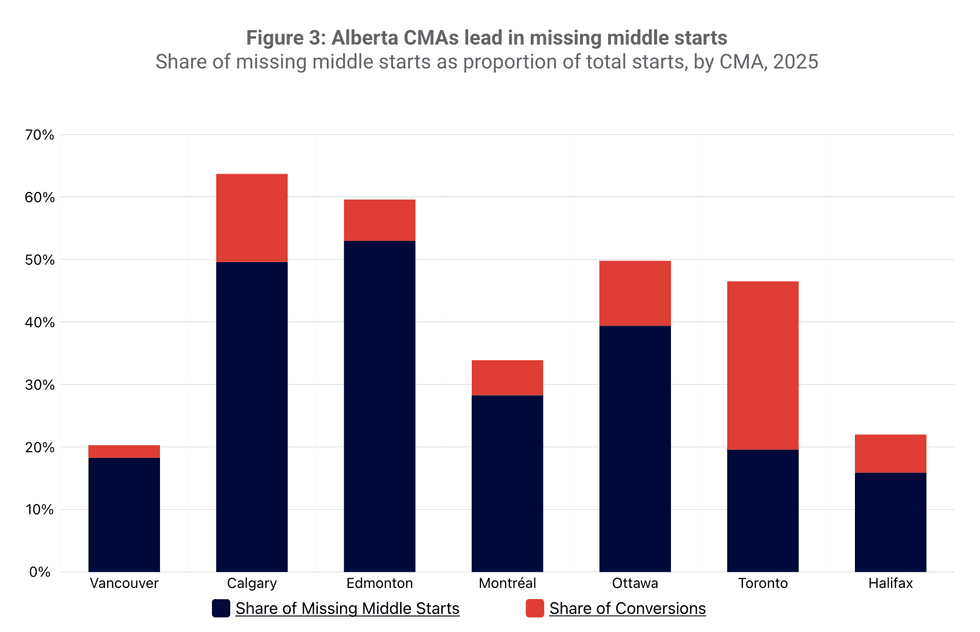

At the same time, construction of “missing middle” housing continued to expand. The category — which includes accessory suites, multiplexes, row houses, stacked townhouses, and low-rise apartments — accounted for roughly 10% more starts across Canada’s seven largest CMAs in 2025.

This form of housing has grown steadily in most major cities since 2018. Calgary and Edmonton led the trend in 2025, with about 60% of new housing starts falling into the missing middle category, largely made up of row houses and townhomes. Toronto followed at roughly 50%, with more than half of those units coming from conversions of existing buildings.

Spring 2026 Housing Supply Report/CMHC

Spring 2026 Housing Supply Report/CMHC

Missing middle housing is considered an important source of faster-to-build and relatively lower-cost housing in established neighbourhoods, while also providing alternatives for households priced out of single-detached homes but seeking more space than high-rise units typically offer.

Construction Timelines Improve, Completions Surge

Despite the large number of apartment projects underway across the country, construction timelines improved in several markets during 2025. Smaller project sizes, efficiency gains, slower construction cost growth, and easing labour constraints all contributed to faster delivery times.

Calgary, Ottawa, and Edmonton recorded the strongest improvements in construction timelines, with Calgary and Edmonton delivering the fastest apartment construction times overall.

At the same time, completions remained historically strong as projects launched in previous years reached the finish line. Vancouver recorded a new completion record — driven primarily by apartment projects — while Calgary and Edmonton also reached record levels, supported by strong ground-oriented housing completions.

Although completions softened slightly in Montreal, Ottawa, Toronto, and Halifax, levels remained historically elevated across those markets as well.

Spring 2026 Housing Supply Report/CMHC

Spring 2026 Housing Supply Report/CMHC

Condo Slowdown Raises Concerns For Future Supply

Despite the increase in new housing supply, the report identifies growing challenges that could constrain future development.

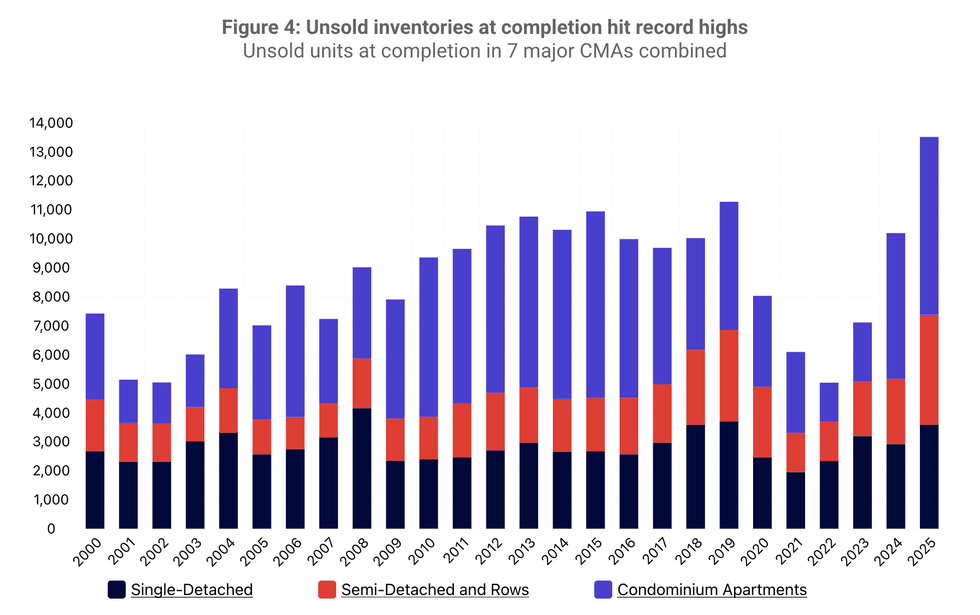

Condominium apartment starts declined sharply across the country as presales weakened and investors pulled back. Elevated construction costs also made it more difficult for developers to meet presale thresholds required for financing.

These conditions were accompanied by rising levels of unsold inventory at completion across most major markets, with the exception of Montreal. Vancouver recorded the highest level of unsold condominium inventory at completion, while Edmonton had the largest inventory of unsold ground-oriented homes. Toronto also saw notable increases in unsold condominium units and row houses.

When completed units remain unsold, financing conditions typically tighten, making it harder for developers to launch new projects. As a result, some developments are delayed or cancelled, slowing the pipeline of future housing supply.

Vancouver: Short-Term Relief Masks Longer-Term Risks

In the Vancouver region, housing conditions appeared to ease in 2025, but the report notes that the shift reflects timing rather than a fundamental balance between supply and demand.

A large wave of housing completions — following several years of strong construction activity — increased available supply and pushed rental vacancy rates higher, contributing to slower rent growth and weaker resale price gains.

At the same time, resale listings increased as some homeowners faced mortgage renewals at higher interest rates or adjusted their housing arrangements. Meanwhile, resale transactions dropped to their lowest level in two decades.

Despite these softer conditions, the longer-term supply pipeline has begun to shrink. Housing starts have now declined for two consecutive years, and project cancellations are expected to reduce the number of units delivered in the future, particularly in the condominium sector.

Developers in the region also faced rising construction costs and weaker revenue expectations, as slower rent growth and higher vacancy rates made new rental projects more difficult to finance.

Even so, missing middle construction increased in the region. Ground-oriented housing starts rose year-over-year, led by growth in semi-detached housing in Burnaby following local policy changes allowing laneway homes and secondary suites in those developments.

Toronto: Short-Term Surplus, Long-Term Supply Risk

In the Toronto region, the report highlights a divergence between current market conditions and longer-term supply trends.

In the short term, housing markets appear more relaxed. Higher rental vacancy rates, slowing rent growth, and declining home prices have emerged alongside increased supply. A high volume of housing completions and record levels of resale listings have expanded available inventory, while slower population growth and economic uncertainty have weakened demand.

However, the report notes that housing starts declined again in 2025, and have now fallen to their lowest level since 2009. For the first time, Toronto recorded fewer housing starts than Calgary, Montreal, and Vancouver.

Because new projects can take several years to move from planning to occupancy, the current slowdown in starts could translate into future supply shortages if demand rebounds. The cancellation of condominium projects is also expected to remove thousands of units from the future housing pipeline.

Differences between housing types also complicate the market outlook. Surpluses were larger among smaller condominium apartments, for instance, than among family-sized homes.

Developers increasingly shifted towards smaller projects in response to financing challenges and economic uncertainty. In 2025, projects containing three to five units outnumbered developments with more than 100 units for the first time on record.

Purpose-built rental construction also gained ground. Rental starts reached their second-highest level since 1990 and, in the City of Toronto, exceeded condominium apartment starts for the first time.

Supply Imbalances Expected To Ease Over Time

Looking ahead, the report projects that national housing starts will decline through 2026 to 2028 as developers contend with elevated costs, softer demand, and higher inventories.

However, the supply imbalances that emerged in 2025 are expected to ease as the market gradually absorbs newly completed housing.

Over time, as new homes enter the housing system and age, they tend to become relatively more affordable — a process the report identifies as an important mechanism through which new housing supply improves affordability across the broader housing market.