It's no secret that buying real estate in Ontario is a daunting task. Should you save up to live in your dream neighbourhood that's close to top-rated schools or settle for something more affordable that requires a longer commute? Do you wait until prices go down or that family-friendly housing development goes up? The list of questions and decisions never ends.

And while there are dozens of scenarios that might steer you away from taking the home-owning plunge, at least future and current homeowners can find some solace knowing they can save some money on their home insurance -- which can be a costly expense for Canadian homeowners -- as insurance rates have dropped in Ontario.

According to the inaugural Home Insurance Price Index report from leading financial comparison site LowestRates.ca, there are many forces that are currently affecting home insurance prices, including climate change.

The report focuses on three of Canada’s largest home insurance markets: British Columbia, Alberta, and Ontario, accounting for nearly two-thirds of the country's population.

"The industry expects prices are only going to get more expensive as insurance companies deal with rising building costs, increased weather events, and more claims," says Justin Thouin, CEO of LowestRates.ca.

"However, not all insurers will raise their rates at the same level. While one company may be raising rates by 10%, another may raise rates only 1%. You need to be able to find the ones that are offering better rates in a rising rate environment."

READ: Real Estate Continues to Contribute to Employment Growth in Canada: StatsCan

According to the data, on average, homeowner’s house insurance premiums in BC climbed by 6% from Q3-2019 through Q3-2020, which LowestRates labels a "substantial" year-over-year increase driven by escalating real estate values and the increased frequency and severity of weather events.

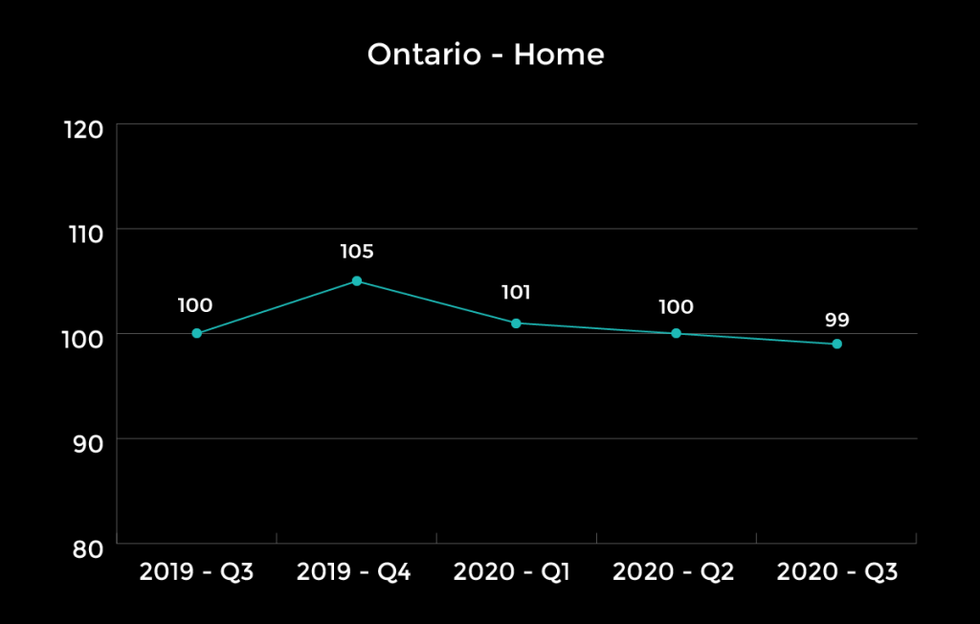

Over the same period, rates rose in Alberta by just 1%, while dropping in Ontario by 1%. In these two provinces, the impact of rising valuations and climate change was tempered by other factors.

In the report, LowestRates.ca says climate change has been a key driver of home insurance prices, with residential property premiums rising over the past year -- a trend that experts say is likely to continue.

"It’s likely that the increases we’ve seen across the provinces will begin to rise more aggressively as climate change gets worse and weather-related damages become more extreme," reads the report.

Elektra Hilton, the Director of Operations at DirectRate.ca, agrees that home insurance rates have -- and will continue to be -- impacted by severe weather events.

“Climate change has affected home insurance. For example, flash flooding and hail have been major events in recent years which resulted in significant costs to the industry. Home insurance rates will likely continue to be impacted by severe weather events,” explained Hilton.

According to the report, COVID-19 hasn't influenced the increase in home insurance premiums over the past several months.

LowestRates.ca COO Dave Dyer explains that any increases we’re seeing in home and condo insurance can be largely attributed to non-COVID factors -- such as climate change and inflation -- rather than the increase of Canadians working from home.

"Unless working from home poses additional risks to the structure or contents of the property, most Canadians don’t have to worry about seeing increases in their property insurance premiums anytime soon," said Dyer.

However, just because home insurance premiums haven’t increased yet, it doesn’t mean the higher volume of people working from home won’t cause premiums to increase in the future.

Regardless of how COVID-19 will impact insurance in the future, at the moment, consumers luckily aren’t seeing higher prices due to it -- not yet, anyway.

The news, however, is much worse for condo owners. In both BC and Alberta, the average cost of condo insurance increased by 16% in Q3-2020, with severe weather events serving as a key factor, as were rising costs for building materials and less competition in the condo insurance market. LowestRates.ca believes that this trend may eventually "creep" into other regions as well.

And while not as drastic, the situation is still dire in Ontario, where condo insurance premiums rose by 3% in 2020 -- however, market observers believe bigger increases are likely on the way.

The report points out that a massive amount of new condos have been built throughout Ontario in the past decade, with some cities, such as Toronto, having "rushed" to build condos to keep up with a rapidly increasing population.

"Condos being built so quickly increases the risk of lower workmanship, potentially resulting in building problems that may require an insurance claim later on. This could contribute to the trend of a rising number of claims," reads the report.

For now, with condo insurance rates up only 3% in Ontario year-over-year, LowestRates.ca says it has yet to see a major impact on consumers.

"But it’s certainly something that the insurance industry is aware of and we’ll continue to watch and report on if it leads to a surge in prices in Ontario," reads the report.