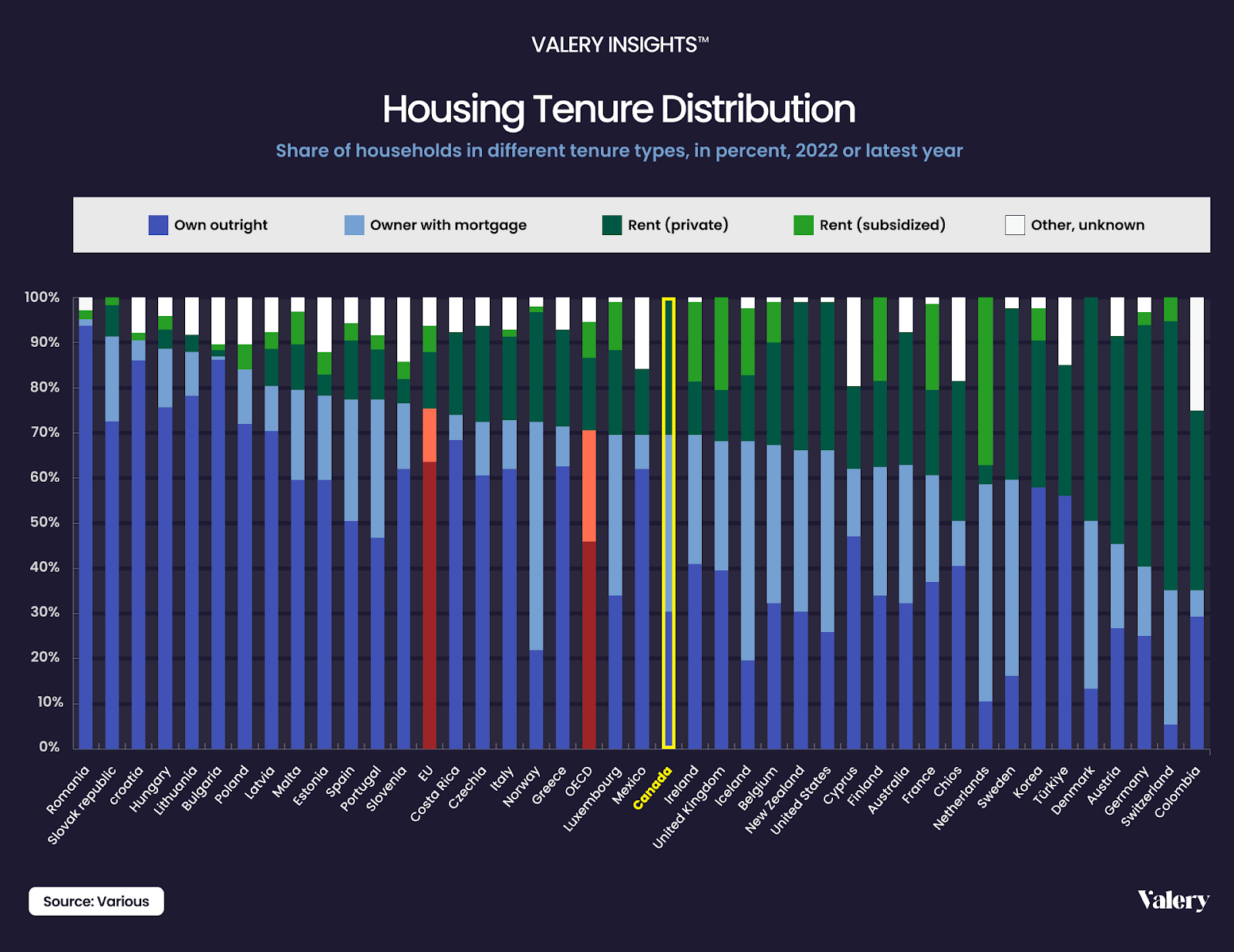

There is a quiet revolution unfolding at the heart of Canada’s housing system — not on the skyline, but on the balance sheet of its most influential insurer, Canada Mortgage and Housing Corporation (CMHC).

For decades, CMHC had been the invisible hand helping Canadians buy homes. It backed buyers, stabilized lenders, and injected liquidity into the market when confidence wavered. But as revealed in its 2024 annual report, that hand has shifted. Much like our European counterparts, who have seen decades of declining homeownership in favour of institutional rental housing development, CMHC has begun lifting a different pillar of the housing economy: rental development.

via valery.ca

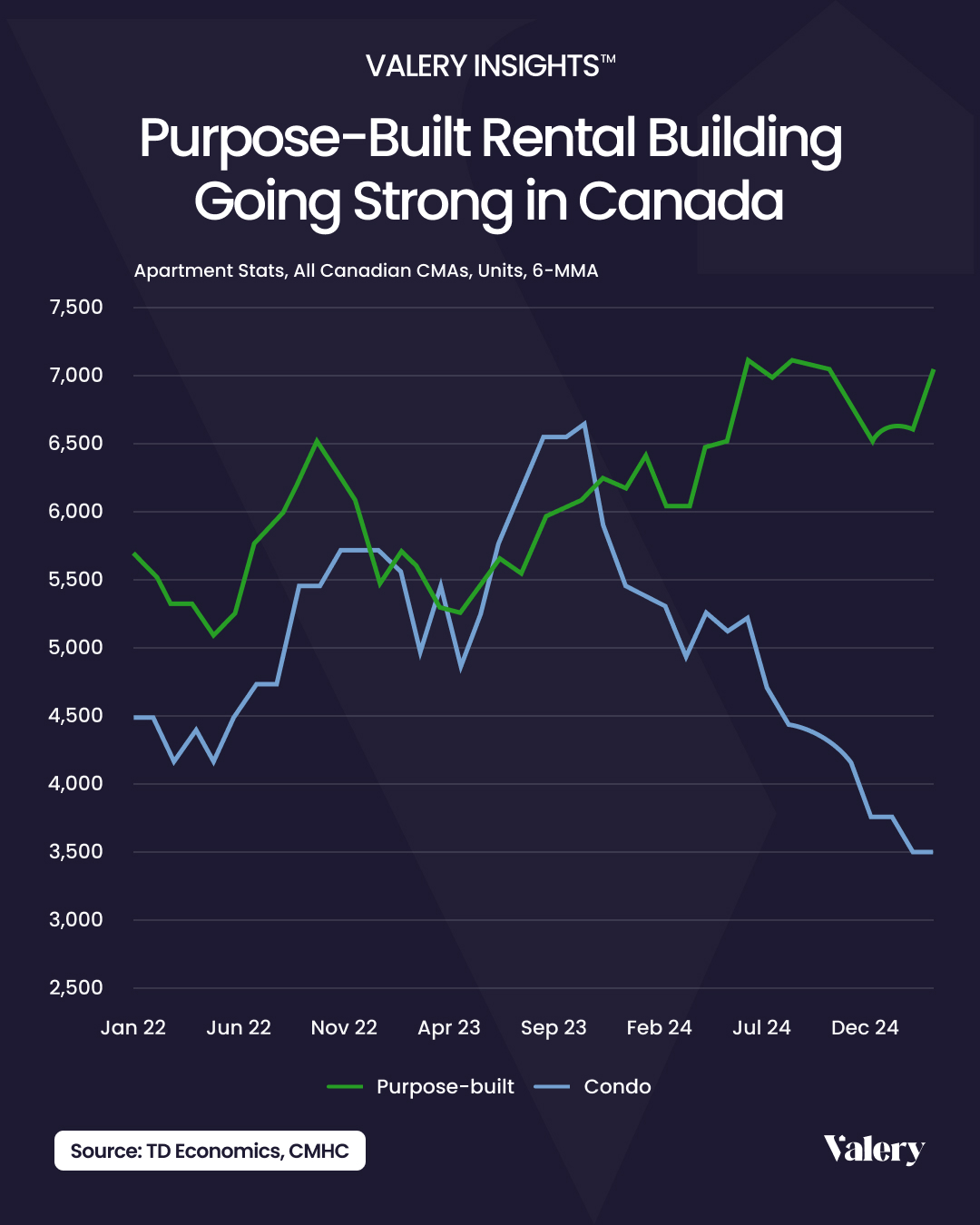

This wasn’t just a strategic adjustment. It has been a gradual structural transformation, one that redefined who CMHC served, where capital flowed, and how risk was distributed in the housing system. Perhaps we’ll be thanking CMHC decades from now, given that purpose-built rental has now backfilled a large portion of the condo supply pipeline, which has all but dropped off.

A lot of real estate industry experts talk about a “supply gap” we could see in Canada in 2028 when the condo pipeline dries up and there’s a shortage of new units. If we keep building rental at this pace, I don’t think that’s something we’ll need to worry about.

via valery.ca

The Numbers Are Impossible To Ignore

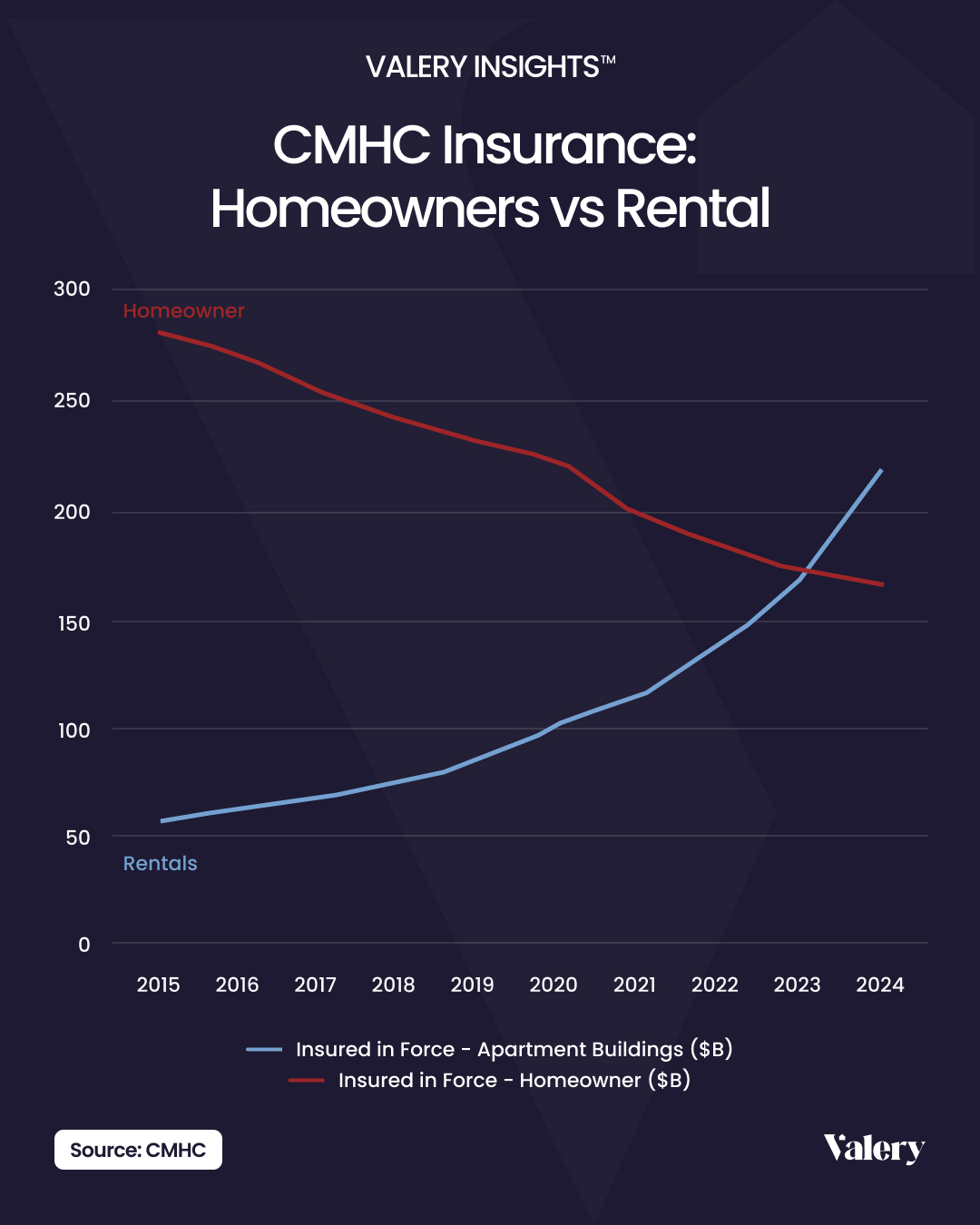

Let’s start with the most basic indicator of intent, i.e. insurance-in-force.

In 2024, CMHC held $213 billion in insurance on multi-unit apartment buildings, up from $168 billion the year prior. Meanwhile, insurance on single-family homeowners fell to $162 billion. The chart below shows the long-term trend.This inversion is no short of a watershed. For the first time in its history, CMHC’s book is led not by the dream of ownership, but by the machinery of rent.

via valery.ca

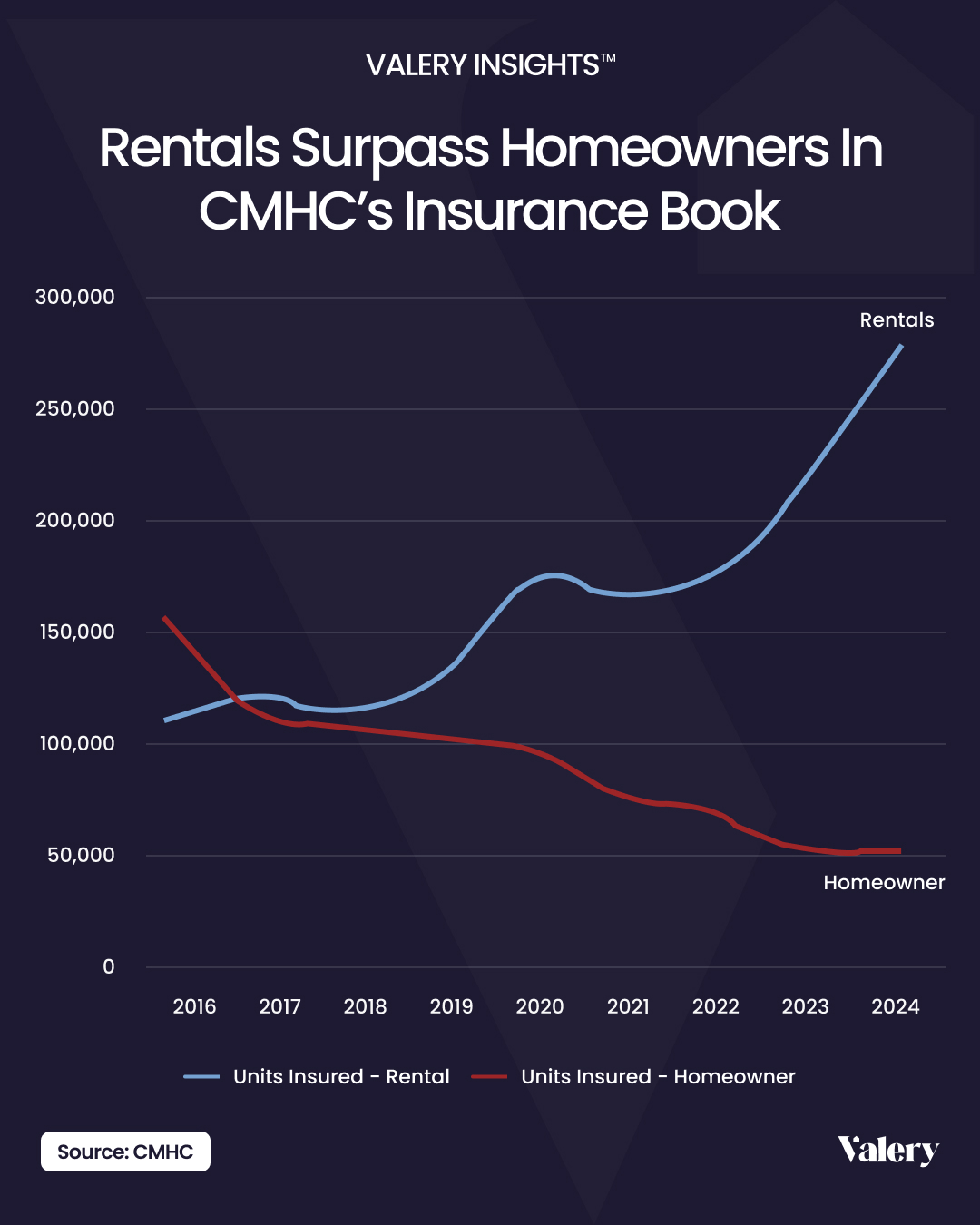

And it’s not just dollars, it’s doors.

CMHC insured 283,700 rental units last year. That’s a 28% spike, driven overwhelmingly by the fact that CMHC’s MLI Select program is one of the only ways a builder can afford to build today. Homeowner loans? Just 49,600 — a marginal 3% gain. The visual below shows how that divergence has played out over the past decade. What began as a narrow difference has now become a wide and accelerating gap, one that is increasing at an even greater pace since the introduction of MLI Select in 2022.

Within this divergence lies the story of where Canadian housing is heading, and who gets left behind.

via valery.ca

Premiums, Arrears, And The Rising Cost Of Risk

Follow the money and the picture sharpens further. CMHC collected $1.67 billion in premiums and fees from the multifamily segment alone, a 73% jump year over year. Rental underwriting is now the single largest driver of the agency’s insurance revenue.

But with volume comes volatility.

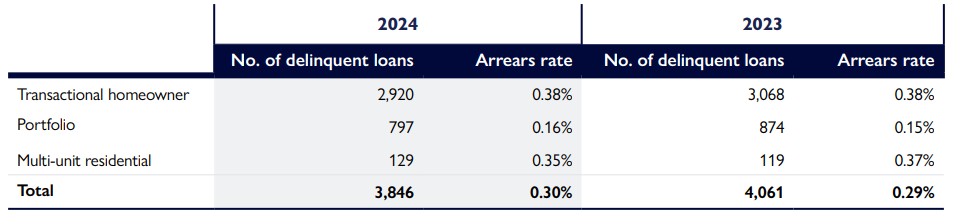

CMHC’s insurance-service expense ratio, a key metric of risk-adjusted cost, jumped to 12.6% in 2024. The agency attributes this rise “primarily to increasing multi-unit arrears volumes, particularly in Québec.” The number of delinquent multifamily loans ticked up to 129, an 8% increase in raw counts, even as the official arrears rate (0.35%) dipped slightly due to the expanding portfolio. The table below breaks down delinquency counts and arrears rates across CMHC’s portfolio for the years 2023 and 2024.

Delinquent Loan Trends by Segment, 2023–2024/CMHC

Bigger Balances, Tighter Buffers

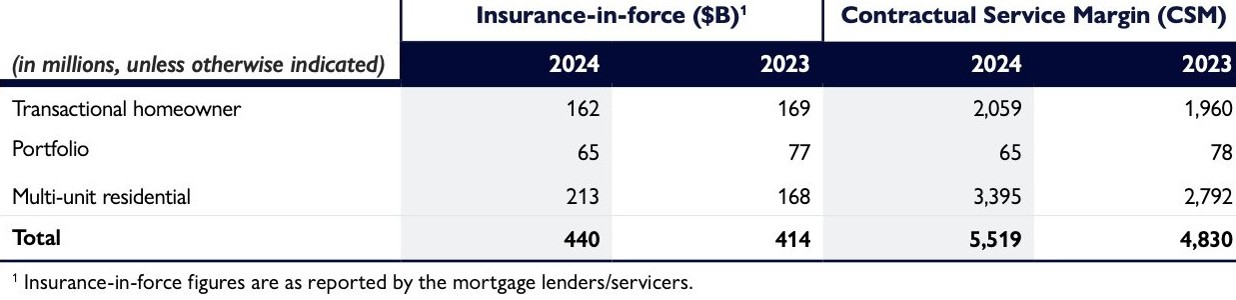

Liabilities tied to multifamily insurance swelled 34%, hitting nearly $5 billion. To hedge against this exposure, CMHC boosted its Contractual Service Margin (CSM), essentially a buffer of unearned profit, to $3.4 billion in the multi-unit book, as shown in the table below.

And yet, the biggest defensive move wasn’t on paper, it was on dividends.

In 2024, CMHC cut its payouts to the government, deliberately stockpiling capital in anticipation of OSFI’s new multi-unit capital framework set to launch in 2026. The agency is repositioning itself for a regime where multifamily underwriting will carry a heavier capital load. Translation: more skin in the game, less cash flowing out.

This is prudent governance. But it also underscores just how large, and potentially volatile, CMHC’s exposure to the rental market has become.

Year-over-Year Comparison of Insurance-in-Force and Contractual Service Margins/CMHC

Securitization Echoes The Strategy

Capital markets don’t lie. And in 2024, they followed CMHC’s lead, straight into the rental sector.

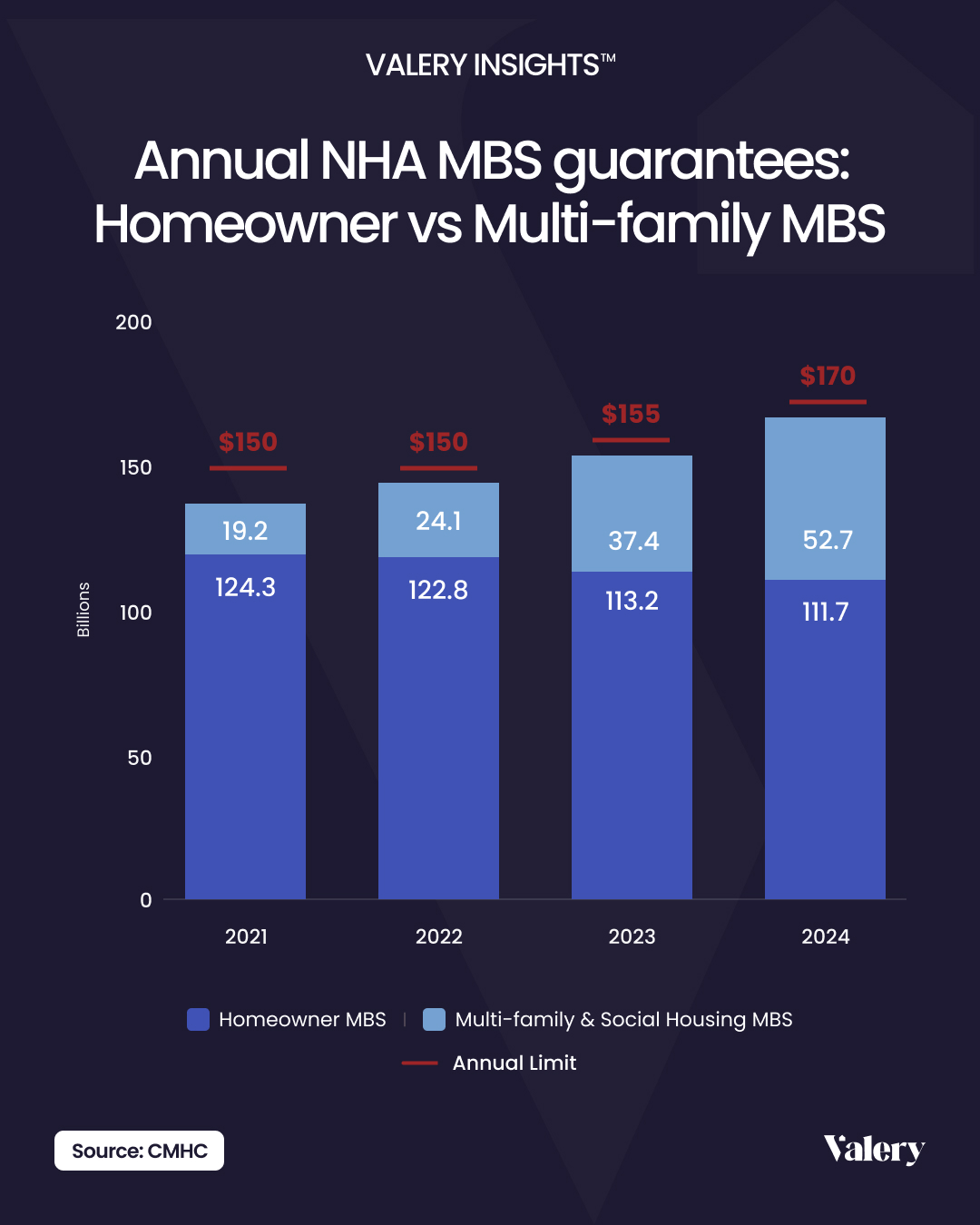

Multi-family NHA-MBS issuance soared to $52.7 billion, a 41% jump over the previous year. By contrast, homeowner-backed mortgage securities flatlined. The chart below shows how CMHC’s securitization strategy has evolved since 2021. Developers, and the financial institutions funding them, are increasingly leaning on CMHC-backed securitization to finance new rental construction at scale.

via valery.ca

Critically, a growing share of these mortgage pools are classified as “affordability-linked,” products tied to the MLI Select program, which rewards builders for delivering energy-efficient, accessible, and affordable units. In 2024, $38.8 billion of such affordability-linked securities were issued, up from $29 billion the year before.

It’s a smart design. But the volumes now involved give CMHC the power not just to incentivize, but to dictate the terms of rental development in Canada.

Capital Flow Is Policy Now

What we’re witnessing is a recalibration of Canada’s housing mandate.

Rental projects are faster to approve, denser to build, and more efficient to fund than their single-family counterparts. They also align neatly with climate targets, urban intensification goals, and CMHC’s affordability framework. For federal policymakers desperate to boost supply, CMHC’s multifamily underwriting engine is a gift.

But gifts come with tradeoffs.

Every dollar of insurance capacity extended to a rental project is a dollar less available to underwrite homeownership. Every policy tweak that makes rental lending easier inadvertently makes the ownership path longer, riskier, and less subsidized.

The result? A structurally rental-forward housing system, not by accident, but by architecture.

What Happens When The Tilt Becomes A Tumble?

There’s no doubt we need more rental housing. Nor is there any question that CMHC’s tools have become sharper, faster, and more targeted in delivering it.

But here’s the concern: in solving one crisis, are we sleepwalking into another?

The balance of Canada’s housing system has historically relied on a healthy interplay between rental and ownership. One fuels mobility. The other fuels stability. One offers flexibility. The other builds equity. When that balance frays, social mobility slows. Wealth gaps widen. The very foundation of a “middle-class dream” begins to erode.

CMHC is now underwriting the rental economy at a scale no one predicted. That brings enormous opportunity, but also enormous influence. And influence, unchecked, becomes fragility.

A Closing Word To Stakeholders

If you’re a builder, the signal from CMHC is clear: this is your moment. Capital is flowing. Insurance is available. CMHC has your back, provided you align with their affordability, energy, and accessibility mandates.

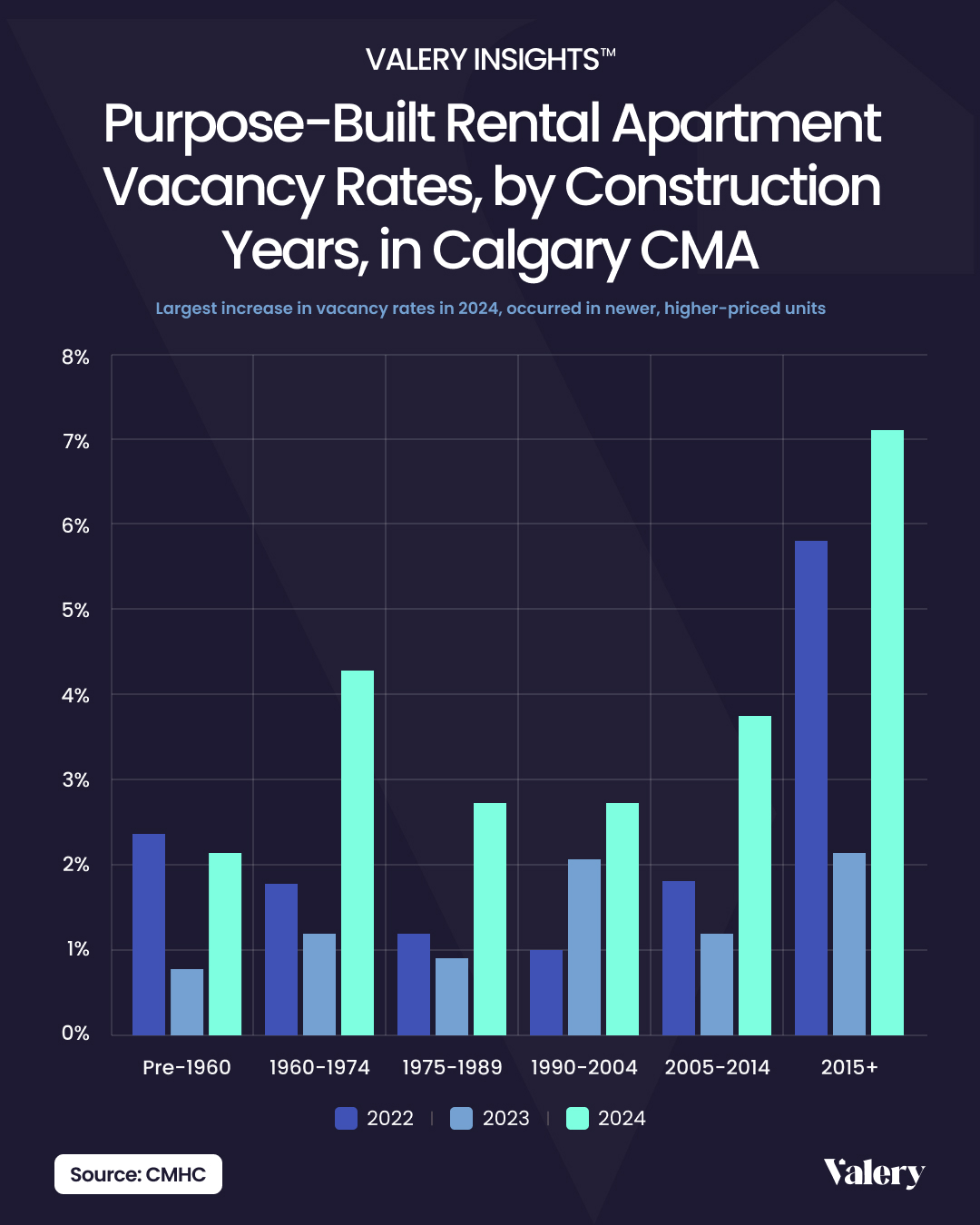

The bigger problem is an economic one. Builders must decide whether or not we’re at risk of overbuilding rental supply, given falling population growth, falling rents, and rising vacancy rates. I never thought I’d say the word “overbuilding” in Canadian real estate in my lifetime, but look no further than Calgary’s rental market, which was flooded with MLI Select builds underwritten at 2% vacancy in 2023, that were stabilizing into a 7% vacancy market (figure below). Edmonton seems to be on a similar path, with a record number of Toronto pre-construction investors buying CMHC MLI Select financed multiplexes.

via valery.ca

While multifamily delinquencies aren’t rising as a percentage, they are rising in volume and one can’t help but be concerned about the impact that a historic boom/bust Alberta cycle might have on their record rental supply pipeline.

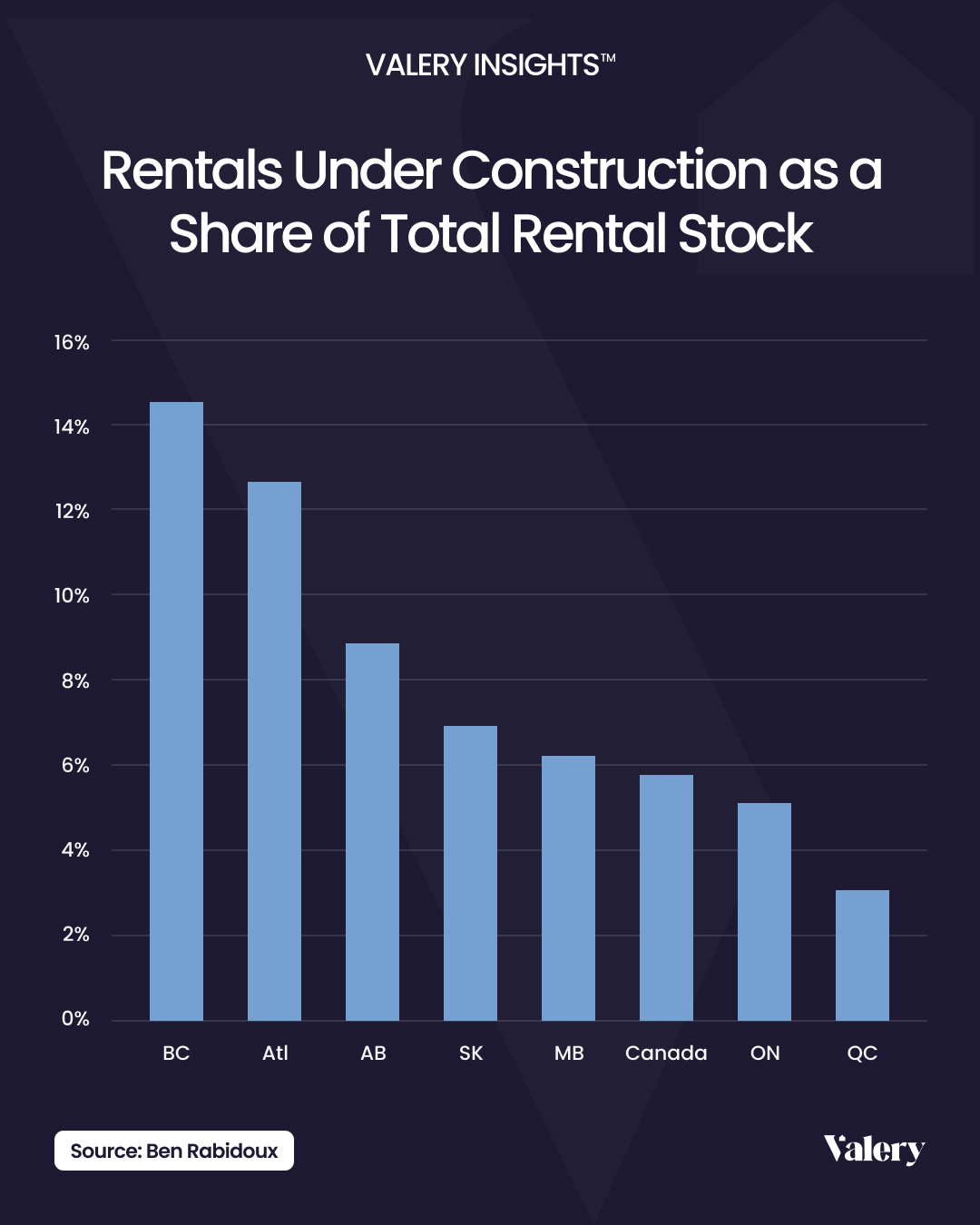

Compounding that, the sheer magnitude of rental under construction right now relative to existing supply is the highest we’ve seen in decades, with some markets more vulnerable than others (see: BC and Atlantic Canada). In the absence of growing rental demand via population growth, this supply flood could materialize in a direct upward hit to vacancy rates. Honestly, it would not surprise me to see vacancy rates two to three times from where we are right now. We’re currently in the 2% range and 6%+ would not be unheard of given the setup:

via valery.ca

If you’re an investor, follow the paper trail. Securitized rental paper, especially MLI Select pools, is where the liquidity is heading.

But if you’re a policymaker, a buyer, or a lender? You should be asking tougher questions.

- Who will champion first-time buyers in a system tilting toward institutional landlords?

- What guardrails exist to ensure rental-led risk doesn’t overwhelm (or overshoot) CMHC’s core mandate?

- And how do we restore balance before the pendulum swings too far?

Make no mistake, the future is rental-fied. The question is whether it will also be equitable, sustainable, and resilient.